|

|

|

|

|

(State or Other Jurisdiction

of Incorporation)

|

(Commission File Number)

|

(IRS Employer

Identification No.)

|

|

|

|

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

|

Title of each class

|

Trading

Symbol(s)

|

Name of each exchange on which registered

|

||

|

|

|

The

|

||

|

interest in a share of 7.50% Series A Fixed-Rate Non-Cumulative Perpetual Preferred Stock) |

|

The

|

|

Exhibit

Number

|

Description

|

|

|

99.1

|

Guidance statement, dated October 10, 2024. | |

|

104

|

Cover Page Interactive Data File (embedded within the Inline XBRL document).

|

|

|

|

MAINSTREET BANCSHARES, INC

|

|

|

|

|

|

|

|

Date: October 10, 2024

|

|

By:

|

/s/ Thomas J. Chmelik

|

|

|

|

|

Name: Thomas J. Chmelik

|

|

|

|

|

Title: Chief Financial Officer

|

Exhibit 99.1

MainStreet Bancshares Issues Guidance for Third Quarter 2024 Earnings

FAIRFAX, Va., October 10, 2024 – MainStreet Bancshares, Inc. (Nasdaq: MNSB & MNSBP), the holding company for MainStreet Bank, today issued guidance for its upcoming third quarter earnings. The Company estimates a loss of four cents per common share for the third quarter.

During the third quarter, the Company charged-off $1.9 million to successfully offload $21.8 million in nonperforming loans. The loans originated between March 2020 and April 2021, and bore the full brunt of pandemic-related construction delays, higher costs, supply chain delays and rapidly increasing interest rates.

In addition, the Company reversed $983,000 of accrued interest income, and paid $593,519 in nonrecurring liquidation expenses. The Company made a provision of $1 million to support loan growth and ensure the Allowance for Credit Losses is directionally consistent.

“We’ve been thorough in identifying problem loans and where possible, have found creative means to work with borrowers to preserve their ownership,” said Tom Floyd, Chief Lending Officer of MainStreet Bank. “However, in a few cases the borrowers’ options dwindled and the best course of action was liquidation.”

Changes to nonperforming loans are summarized in the table below.

|

Nonperforming loan activity between Q2 and Q3 |

||

|

Beginning balance 6/30/2024: |

$20,690,967 |

|

|

Additions: |

31,352,865 |

|

|

Dispositions: |

-21,802,695 |

|

|

Charge-offs: |

-1,906,503 |

|

|

Normal paydowns: |

-70,678 |

|

|

Ending balance 9/30/2024: |

$28,263,956 |

|

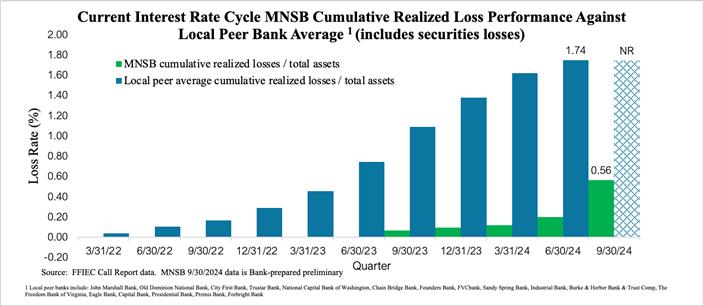

Despite the activity recognized during the third quarter, the Company’s cumulative loss history over the course of the entire interest rate cycle is less than one-third of its local peer average cumulative losses, as shown in the table below.

The Company maintained a superior net interest margin throughout the current interest rate cycle, led by strong loan yields. The Company’s core net interest margin is expanding, estimated to be 3.25% for the quarter. The Generally Accepted Accounting Principles net interest margin is estimated to be 3.05% for the quarter and is estimated to be 3.19% year-to-date.

“The Bank continues to originate good loans and grow deposits,” said Abdul Hersiburane, President of MainStreet Bank. “The FOMC has started down the path of easing interest rates, which will take the pressure off our variable rate borrowers and open the Washington, D.C. condo market to a new field of buyers.”

Third Quarter 2024 Earnings Release and Virtual Meeting

The Company anticipates releasing earnings before the market opens on Monday, October 28, and hosting a conference call at 2 p.m. EST to discuss the company's third quarter and year-to-date results.

ABOUT MAINSTREET BANK: MainStreet operates six branches in Herndon, Fairfax, McLean, Leesburg, Clarendon, and Washington, D.C. MainStreet Bank has 55,000 free ATMs and a fully integrated online and mobile banking solution. The Bank is not restricted by a conventional branching system, as it can offer business customers the ability to Put Our Bank in Your Office®. With robust and easy-to-use online business banking technology, MainStreet has "put our bank" in thousands of businesses in the metropolitan area.

MainStreet Bank has a robust line of business and professional lending products, including government contracting lines of credit, commercial lines and term loans, residential and commercial construction, and commercial real estate. MainStreet is an SBA Preferred Lender. From sophisticated cash management to enhanced mobile banking and instant-issue Debit Cards, MainStreet Bank is always looking for ways to improve our customer's experience.

MainStreet Bank was the first community bank in the Washington, D.C., metropolitan area to offer a full online business banking solution. MainStreet Bank was also the first bank headquartered in the Commonwealth of Virginia to offer CDARS – a solution that provides multi-million-dollar FDIC insurance. Further information on the Bank can be obtained by visiting its website at mstreetbank.com.

Banking-as-a-Service

In recent months, the weaknesses of other embedded banking solutions have been exposed—to the detriment of banks, their fintech clients and their end-customers. The Avenu team digested all the lessons that could be learned from these weaknesses and implemented enhancements to provide a scalable and compliance-rich solution. Version 1 of the Avenu Software as a Service solution was completed on September 18, 2024.

Avenu

Avenu is the first and only embedded banking solution that connects our partners and their apps directly and seamlessly to our purpose-built Avenu core solution. We are not a sponsor bank without our own technology, and we are not a middleware software company without our own bank. We are Avenu, a leading financial technology company owned by an established community bank in the heart of Washington, D.C.

Avenu’s clients are fintechs, social media, application developers, money movers, and entrepreneurs. They all have one thing in common: They are innovating how money moves to solve real-world issues and help communities thrive. We are focused on servicing our community and creating long-term business relationships.

This release contains forward-looking statements, including our expectations with respect to future events that are subject to various risks and uncertainties. The statements contained in this release that are not historical facts are forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. Words such as "may," "will," "could," "should," "expect," "plan," "project," "intend," "anticipate," "believe," "estimate," "predict," "potential," "pursuant," "target," "continue," and similar expressions are intended to identify such forward-looking statements. Factors that could cause actual results to differ materially from management's projections, forecasts, estimates and expectations include: fluctuation in market rates of interest and loan and deposit pricing, adverse changes in the overall national economy as well as adverse economic conditions in our specific market areas, , maintenance and development of well-established and valued client relationships and referral source relationships, and acquisition or loss of key production personnel. We caution readers that the list of factors above is not exclusive. The forward-looking statements are made as of the date of this release, and we may not undertake steps to update the forward-looking statements to reflect the impact of any circumstances or events that arise after the date the forward-looking statements are made. In addition, our past results of operations are not necessarily indicative of future performance.