May 8, 2023

VIA EDGAR

U.S. Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549

Attention: |

Mr. Christopher Wall |

|

|

Ms. Sonia Bednarowski Ms. Kate Tillan Ms. Bonnie Baynes |

|

|

|

|

|

Re: |

CleanSpark, Inc. |

|

|

Form 10-K for the Fiscal Year Ended September 30, 2022 |

|

|

Filed December 15, 2022 |

|

|

Form 10-Q for the Quarterly Period Ended December 31, 2022 |

|

|

Filed February 9, 2023 |

|

|

File No. 001-39187 |

Dear Mr. Wall and Ms. Bednarowski:

This letter is being furnished on behalf of CleanSpark, Inc. (the “Company,” “we” or “us”) in response to the comment received from the staff of the Division of Corporation Finance Office of Crypto Assets (the “Staff”) of the U.S. Securities and Exchange Commission (the “Commission”) by letter dated March 31, 2023, regarding the Company’s Form 10-K for the Fiscal Year Ended September 30, 2022 (the “10-K”) (File No. 000-39187) filed on December 15, 2022 and the Company’s Form 10-Q for the Quarterly Period Ended December 31, 2022 (File No. 001-39187) filed on February 9, 2023.

The text of the Staff’s comment has been included in bold and italics for your convenience, and we have numbered the paragraph below to correspond to the number in the Staff’s letter. For your convenience, we have also set forth the Company’s response immediately below the numbered comment.

10-K for the Fiscal Year Ended September 30, 2022 General

Response:

The Company acknowledges the Staff’s comment and confirms that a table showing a comprehensive breakeven analysis that compares the average cost to earn or mine one bitcoin with the average revenue earned per bitcoin in the period will be included in future filings, including the Company’s upcoming Quarterly Report on Form 10-Q for the period ended March 31, 2023 expected to be filed on or about May 10, 2023 (the “Second Quarter

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

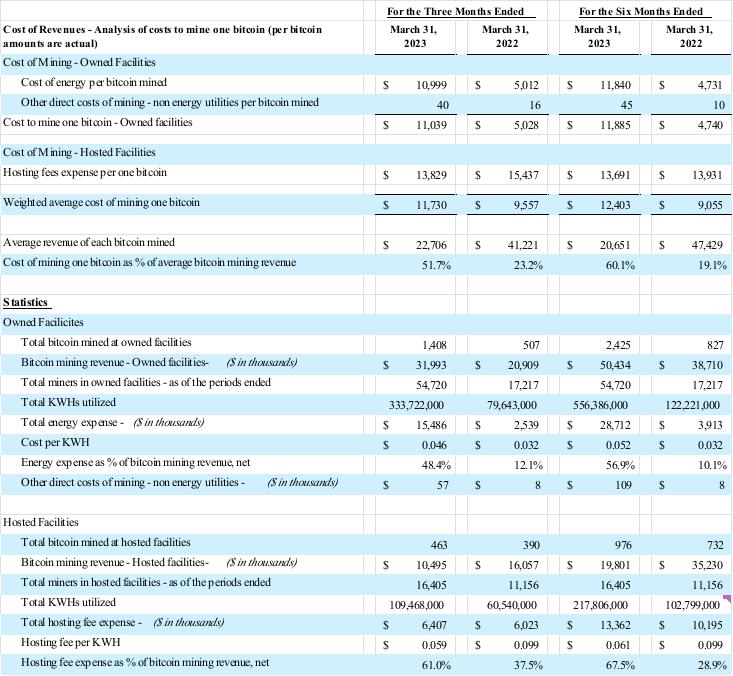

10-Q”). The format of the table that we intend to include in the Second Quarter 10-Q is included below and will include both a 3-month and year-to-date comparable periods.

As depicted above in the table, the Company calculates the “Cost of Mining” based on the Cost of Revenues line item in the Consolidated Statements of Operations and Comprehensive Income (Loss), which includes energy costs as well as hosting fee expenses. The Company considers these costs as directly associated with the mining costs. We also are including statistics in this table, which we believe enhance investors’ understanding of our fleet and the key metrics that drive our energy usage.

Comment 3: In future filings, please disclose the percentage of your energy usage that uses clean and renewable energy resources as well as the locations in which you use these resources. In addition, please identify the types of “clean and renewable” energy sources you use and explain how you plan to increase your usage.

Response:

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

The Company acknowledges the Staff’s comment and will disclose the requested information in each future filing that is required to include information required by Item 101 (Business) of Regulation S-K, including the 2023 10-K. The Company notes that such information is not required to be included in the Second Quarter 10-Q or any other quarterly reports on Form 10-Q.

The Company derives energy from the electrical grid, and as a result the Company’s energy mix will vary from period to period based on a variety of factors including weather, temperature, demand, and how the grid operator ultimately procures and utilizes energy resources.

In March 2023, the Company published its first ESG and Corporate Responsibility Report (the “ESG Report”), which is available on the Company’s website. The ESG Report stated that, for the fiscal year ending 2022, based upon data published by the Company’s power providers, the Company’s energy mix was comprised of approximately 94.02% clean energy, 5.70% carbon-based energy, and 0.28% undisclosed energy sources. Clean energy includes hydroelectric, solar, nuclear and wind. Additionally, the Company participates in renewable energy programs, such as Georgia’s Simple Solar (or Flex RECs program), in order to increase access to clean energy sources.

The Company does not currently have location-based data on energy sources. We have engaged a third party, Cleartrace, to generate additional data on energy consumption, which the Company expects will be reported in the Company’s Annual Report on Form 10-K for the fiscal year ended September 30, 2023 (the “2023 10-K”).

Furthermore, the Company is currently engaged with NASDAQ as an ESG advisor to identify additional long-term target goals for clean energy in the coming years. Additionally, as we identify sites for expansion, the availability of clean and low-carbon energy is one important factor (of many) in evaluating such sites and the associated power providers.

Comment 7: In future filings, please disclose the range, mean and average age of your miners, the average downtime attributed to scheduled maintenance and non-scheduled maintenance as well as the average, mean and range of the energy efficiency of your miners.

Response:

The Company acknowledges the Staff’s comment and will provide in its future filings, including in Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations of the Second Quarter 10-Q, the following disclosure, as appropriately updated in such filing, in response to this request (even though such disclosure is responsive to Item 101 (Business) of Regulation S-K, which is not required in quarterly reports on Form 10-Q).

The Company owns approximately 71,300 miners as of March 31, 2023, which range in age from 1-34 months and have an average age of 12 months. The Company does not have scheduled downtime for its miners, however, it periodically performs unscheduled maintenance on its miners, but such downtime has not historically been significant. When performing unscheduled maintenance,

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

the Company will typically replace the miner with a substitute miner to limit overall downtime. The miners owned as of March 31, 2023 have a range of energy efficiency (watts per terahash – “w/th”) of 21.5 to 38 w/th with an average energy efficiency of 31.0 w/th.

Comment 9: In future filings, please disclose your custody procedures and arrangements by identifying all third-party custodians and the material terms of the agreements, including:

Response:

The Company acknowledges the Staff’s comment and will disclose the requested information in each future filing that is required to include information required by Item 101 (Business) of Regulation S-K, including the 2023 10-K. The Company notes that such information is not required to be included in the Second Quarter 10-Q or any other quarterly reports on Form 10-Q.

Specifically, the Company will disclose information consistent with the following:

The Company holds most of its bitcoin in hot wallets, which are maintained by Coinbase, as it frequently uses its bitcoin balances as a source of liquidity. To the extent the future value of the bitcoin produced exceeds the Company’s needs for operational and other liquidity needs, the Company expects it will store larger bitcoin balances in cold storage, for which the Company has a custody agreement with Coinbase.

For security reasons, Coinbase does not disclose the geographic location of its cold storage wallets to its customers.

The Company currently monetizes its bitcoin balances often, and the CFO or his delegate reconciles expected bitcoin balances to the Coinbase hot wallet on a daily basis. Additionally, cold wallets are reconciled monthly and are considered “on-chain.” In other words, the cold wallets have a unique blockchain address and activity is tracked through the blockchain by the Company if there are any reconciling issues.

Our custody agreement with Coinbase provides that Coinbase Custody will obtain and maintain, at its sole expense, insurance coverage in such types and amounts as are commercially reasonable for the Custodial Services provided under the custody agreement. We do not carry additional insurance coverage on our bitcoin holdings. Further, we are not aware of any insurance providers having inspection rights associated with the crypto assets held in storage.

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

Lines of Business, page 5

Response:

The Company acknowledges the Staff’s comments and advises the Staff that it has no specific material strategic acquisitions that are probable at this time, although we regularly review and explore potential targets. Specifically, the Company regularly enters into non-binding LOIs and performs due diligence on various acquisition targets as part of the Company’s strategy to expand its bitcoin mining operations. The Company currently has an executed, non-binding LOI with a potential target and is in the process of conducting due diligence on that target. While the Company has not yet conducted a significant analysis on that target, the Company does not believe it would be significant if the transaction were to proceed to closing.

At this time, there is no intention to engage in the mining or staking of any other crypto assets. The Company further respectfully submits that it will include the following disclosure in its Second Quarter 10-Q, and will continue to include such disclosure in future filings and update the disclosure as needed to reflect the Company’s latest activities and strategy, and will comply with its obligations (including with respect of financial information and pro forma financial information) in respect of material acquisitions that are completed or, to the extent applicable, are probable:

We regularly evaluate opportunities to expand our business, including through potential acquisitions of businesses or assets. We will evaluate a variety of sources of capital in connection with financing any future possible acquisitions, including the incurrence of debt, sales of stock or bitcoin, or using cash on hand. We may also use the Company’s stock as transaction consideration, as we have done in the past.

Response:

The Company confirms it has a Custody Agreement with Coinbase. The Company also has a Custody Agreement with Genesis Custody Limited, which acts as its backup cold wallet option. However, the Company only has 0.01777 bitcoin with Genesis Custody Limited, which was the result of a test transfer. No further amounts were transferred to this account since the test was completed in mid-2022.

Distribution, Marketing and Strategic Relationships, page 7

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

Response:

Under the the agreement between the Company and Coinmint, Coinmint houses and provides power to CleanSpark’s mining servers located at Coinmint’s site. Additionally, Coinmint provides basic repair and IT services for CleanSpark’s machines. Those servers then connect directly to CleanSpark’s mining pool operated by Foundry. The Company participates in a single mining pool operated by Foundry (“Foundry USA Pool”) and contributes all 6.7 EH/s of current processing power to this pool.

The Foundry USA Pool in which CleanSpark participates does not provide services to any other cryptocurrencies, but other Foundry pools may provide services for other cryptocurrencies. Prior to May 2023, Foundry did not charge the Company any fees for pool services. However, the Company was given notice in April 2023 that Foundry would begin implementing fees for its services, at a rate of 0.19% of total bitcoin earned. Once the Company reaches 10 EH/s of computing power for a quarter, the fee will decrease to 0.15% of total bitcoin earned. This new fee structure was implemented on May 2, 2023.

Cybersecurity, page 10

Response:

The Company acknowledges the Staff’s comment and will provide the requested information, as set forth below, in each future filing, as appropriately updated, that is required to include information required by Item 101 (Business) of Regulation S-K, including the 2023 10-K. The Company notes that such information is not required to be included in the Second Quarter 10-Q or any other quarterly reports on Form 10-Q.

We have property insurance coverage for our bitcoin miners under a multi-tiered insurance program with 18 different underwriters for a total of $100,000,000 in limits. This insurance coverage covers all the Company’s bitcoin miners and includes Earthquake/Flood insurance with a $5,000,000 limit and Storm/Wind/Hail coverage with a limit of 3% Value at Risk of Time of Loss. We also maintain equipment breakdown coverage, with a property damage limit of $100,000,000. We do not maintain Business Interruption Coverage, which is currently not being provided by underwriters to any bitcoin mining companies. The policies also exclude coverage of our bitcoin holdings and cybersecurity coverage. We engage our insurance broker annually to solicit underwriters to provide proposals to renew our current coverage or update our policies to meet our needs, prior to the policies’ expiration on November 1st of each year.

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

Note 2. Summary of Significant Accounting Policies

Revenue Recognition, page F-11

Response:

The Company acknowledges the Staff’s comment and has included a thorough explanation of the payout methodology as part of its response to comment number 8 in this correspondence.

Response:

The Company acknowledges the Staff’s comment and will remove references to confirmation and receipt as required steps, as they are not required for revenue recognition nor do they affect the calculation of the Company’s revenue. Additionally, the Company respectfully submits that it is fully constraining all variable consideration as required by ASC 606-10-32-12a because the amount of consideration is highly susceptible to factors outside of the Company’s control as defined by the Company’s customer’s payout methodology. ASC 606-10-32-11 requires that variable consideration not be included in the transaction price unless it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved. The transaction consideration in the Company’s agreement with the mining pool operator is all variable since the amount of consideration is dependent on the daily computing power provided by the Company (i.e.,

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

hashrate). The Company then receives the expected pay-per-share base amount and a proportionate amount of the transaction fee rewards (as defined in the Foundry USA Pool’s payout methodology described below), based on what the pool mathematically should earn based on the Company’s contributed hashrate as compared to the bitcoin networks algorithmic difficulty. The variable amount is not resolved and determined until the daily earnings are calculated by the pool operator from midnight-to-midnight UTC time in accordance with the payout formula. Considering that contract inception occurs in tandem with daily earnings (i.e., when the computing power is provided to the mining pool), there is no practical manner to include any amount of variable consideration in the transaction price until the variable component is resolved and the consideration has been received.

The payout methodology for the Company’s agreement with Foundry Digital LLC is “Full-Pay-Per-Share” (“FPPS”) for which the Company is awarded daily earnings in the form of bitcoin (see Exhibit A entitled “What is Foundry USA Pool’s payout methodology”). As described in Exhibit A and summarized below, the daily earnings are based on the computing power (user hashrate) that the Company contributes to the mining pool, as a percentage of the global hashrate, as represented by network difficulty which is adjusted by the algorithm every 2,016 blocks (approximately every 14 days), over the daily earnings period. Daily Earnings are calculated from midnight-to-midnight UTC time, and the sub-account balance is credited one hour later at 1 AM UTC time. The Company utilizes Greenwich Mean Time (GMT), which is also the midnight of Coordinated Universal Time or Universal Time Coordinated (UTC), since this is consistent with the Company’s customer contract, in calculating its daily earnings from midnight-to-midnight UTC time

The italicized section below is excerpted from Exhibit A

Total Daily Earnings consists of two parts:

The “Pay-Per-Share Base Amount” pays a flat amount of bitcoin for each share submitted to the pool. It calculates the expected value of hashrate based on the current network difficulty according to this formula:

“Tx Fee Reward” part of the daily reward starts with calculating the “FPPS Rate”. FPPS rate is always above 100% and represents the multiplier for the PPS Base Amount in order to derive the Full-Pay-Per-Share earnings. FPPS Rate is calculated using the sum of all block transaction fees and the sum of all block subsidies, in a given day (calculated midnight-to-midnight UTC).

There are no other terms beyond this formula that cause variability.

As indicated in the payout formula, the Company shares in the expected pay-per-share base amount (“fixed bitcoin rewards”) based on contributed hashrate as compared to the bitcoin networks algorithmic difficulty. The Company’s bitcoins earned through FPPS is determined at the end of the 24 hour “midnight-to-midnight" period once the Company’s

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

computational hashrate contributed over such period has ended. The Company’s proportionate amount of the global network’s transaction fee rewards earned are calculated at the end of each transactional day, in the same manner as the fixed bitcoin rewards. It is important to note that under the pool agreement, the Company is not subject to the pool’s performance, rather, the Company is guaranteed fixed bitcoin rewards and transaction fee rewards based on the hashrate the Company contributes as a percentage of the total global hashrate, as represented by network difficulty.

For purposes of revenue recognition, calculating the transaction fee rewards earned on a real-time basis is not a cost-effective or practical practice. The transaction fee rewards fluctuate for each unique block mined by network participants throughout the daily measurement period, with an average of 144 unique blocks mined over such period, and during which time the Company’s real-time computing power can fluctuate. As a result, it is more practical to measure the Company’s total rewards at the close of each daily measurement period.

The Company has a single performance obligation to its customers to provide computing power services (i.e., hashrate) to the mining pool operator customer. The performance obligation of computing power services is fulfilled over time daily between midnight-to-midnight UTC time, as opposed to a point in time, since the Company provides computing power within the meaning of paragraphs 606-10-25-27 through 25-29. The Company has full control of the mining equipment utilized in providing hashrate to the mining pool and if the Company determines it will increase or decrease the processing power of its machines and/or fleet (i.e., for repairs or when power costs are excessive) this will impact the computing power provided during the “Daily Earnings” period as calculated from midnight-to-midnight UTC time. However, at the end of each day, a full computation can be determined based on the FPPS calculation and the precise calculation of the quantity of bitcoin is determinable.

The Company’s performance is complete in transferring the hashrate service (that is, an asset) to the customer and the customer obtains control of that asset within the meaning of ASC 606-10-25-23 through the service provided. As such, the Company records its share of the bitcoins receivable by the mining pool operator upon the close of the reporting date at midnight UTC.

In exchange for providing computing power, the Company is entitled to a pro-rata share of the fixed bitcoin awards earned over the measurement period, plus a pro-rata fractional share of the global transaction fee rewards for the respective measurement period, less net digital asset fees due to the mining pool operator over the measurement period. The Company’s bitcoin award is based on the proportion of computing power the Company contributed to the mining pool operator as compared to the bitcoin networks algorithmic difficulty. The proportionate share of the transaction fee rewards earned are based on the Company’s computing power as compared to the total computing power contributed to the global network. There are no deferred revenues or other liability obligations recorded by the Company since there are no payments in advance of the performance.

Please see the response to question 9 for an expansive discussion as to how the Company addresses valuation.

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

Response:

Based on the facts and circumstances of the Company’s relationships with the mining pool operators, the Company has concluded that all criteria per ASC 606-10-25-1 are met at the point the Company provides computing power to the mining pool, thus the point of “contract inception.”

Our responses to each aspect of ASC 606-10-25-1 are as follows:

An entity shall account for a contract with a customer that is within the scope of this Topic only when all of the following criteria are met:

The Company currently has a written contract with its mining pool operator (Foundry) and both parties have fulfilled their respective obligations since the contract has been in place (refer to Exhibit A to the Company’s prior response letter for the contract with Foundry).

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

The services required by the customer and consideration payable are specified by the terms of the contract between the customer (the mining pool operator) and the service provider (the Company) per the written contract.

Payment terms for the computing power to the customer (i.e., services) are defined in the contract and accompanying payout formula.

The Company has confirmed commercial substance as evidenced through the terms and conditions of the written contract. The contract is terminable at any time by either party and the Company’s enforceable right to compensation only begins when the Company starts providing computing power to the mining pool operator.

Collectability of contract consideration is probable as the customer has the ability and intention to pay that amount of consideration when it is due as evidenced by the Company historically receiving full consideration daily after the customer obtained control of the Company’s computing power services.

Based on the facts and circumstances of the Company’s relationships with its mining pool operator as discussed above, the Company concluded that the contract arises at the point that the Company provides computing power to the mining pool, which is “contract inception” (which occurs daily at midnight UTC). While the Company has no obligation to perform and can exit the mining pool at any time, when it does provide computing power, the Company has a right to consideration from the mining pool operator for the computing power that it has provided.

The mining pool operator’s payment obligation arises upon the provision of computing power. As a result, the pool operator is obligated to pay for the computing power it receives from the Company in bitcoin (i.e., a noncash consideration), which the pool operator may or may not receive as a direct result of the collective efforts of the mining pool participants. It is the Company’s analysis that the bitcoin valued upon receipt is not materially different than the formula stated in the initial contract and fair value of the bitcoin award received is determined using the closing price of the related bitcoin on the date earned (i.e., contract inception) consistent with 606-10-32-21.

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

As previously clarified in our response to question #8, daily earnings are calculated by Foundry from midnight-to-midnight UTC time, and the Company’s sub-account balance is credited one hour later at 1 AM UTC time with the bitcoin earned. While the Company recognizes the potential for material fluctuations in the fair value of bitcoin over a 24-hour period, because there is only a one-hour difference between date earned at midnight UTC and the received amount at 1 AM UTC time, there is a low risk of material fluctuations due to the limited time difference, hence why it is not viewed as material. As a result, the Company has determined that a reconciliation of the disclosure of bitcoin fair value on the date "earned" with the prior disclosure of bitcoin fair value on the date "received" of will not be meaningful to investors. For clarification, for purposes of revenue recognition, the Company uses the value at midnight UTC, not the time of receipt. The Company will eliminate the use of the word “received” in its disclosures, going forward.

As previously clarified in our response to question #8, the Company’s performance is complete in transferring the hashrate service (i.e., an asset) to the customer as this is when customer obtains control of that asset in accordance with ASC 606-10-25-23. More specifically, the Company has concluded at contract inception that this single performance obligation is satisfied over time in accordance with ASC 606-10-25-27a as the customer simultaneously receives and consumes the benefits provided by the Company’s hashrate services. During this time period, the customer utilizes the Company’s computing power to generate bitcoins (i.e., a digital currency asset) thus meeting ASC 606-10-25-25b, which is using one asset (i.e., our hashrate services) to enhance the value of other assets (i.e., bitcoin). The Company will clarify when “control is transferred” in future filings.

As discussed in response #8, the Company utilizes Greenwich Mean Time (GMT), which is also the midnight of Coordinated Universal Time or Universal Time Coordinated (UTC), since this is consistent with our customer contract in calculating its daily earnings from midnight-to-midnight UTC time.

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

Response:

The Company acknowledges the Staff’s comments and will make these disclosures of qualitative and quantitative information consistent with ASC 606-10-50 as applicable in future filings of Form 10-Ks. Consistent with the disclosure objectives of ASC 606-10-50-1 for an entity to disclose sufficient information to enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. A draft of such disclosure is as follows:

Revenue from Contracts with Customers

The Company recognizes revenue in accordance with ASC Topic 606 – Revenue from Contracts with Customers (ASC 606). The core principle of the revenue standard is that a company should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. The following five steps are applied to achieve that core principle:

Step 1: The Company enters into a contract with a bitcoin mining pool operator (i.e., the customer) to provide computing power to the mining pools. The contracts are terminable at any time by either party and the Company’s enforceable right to compensation only begins when the Company starts providing computing power to the mining pool operator (which occurs daily at midnight UTC). In exchange for providing computing power, the Company is entitled to a pro-rata share of the fixed bitcoin awards earned over the measurement period, plus a pro-rata fractional share of the global transaction fee rewards for the respective measurement period, less net digital asset fees due to the mining pool operator over the measurement period. The Company’s pro-rata share is based on the proportion of computing power the Company contributed to the mining pool operator as compared to the bitcoin network’s algorithmic difficulty. The proportionate share of the transaction fee rewards earned are based on the Company’s computing power as compared to the total computing power contributed to the global network. Applying the criteria per ASC 606-10-25-1, the contract arises at the point that the Company provides computing power to the mining pool operator, which is also contract inception, because customer consumption is in tandem with daily earnings of delivery of the computing power.

Step 2: In order to identify the performance obligations in a contract with a customer, a company must assess the promised goods or services in the contract and identify each promised good or service that is distinct. A performance

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

obligation meets ASC 606’s definition of a “distinct” good or service (or bundle of goods or services) if both of the following criteria are met:

Based on these criteria, the Company has a single performance obligation in providing computing power services (i.e., hashrate) to the mining pool operator (i.e., customer). The performance obligation of computing power services is fulfilled daily over-time, as opposed to a point in time, because the Company provides the hashrate throughout the day and the customer simultaneously obtains control of it and uses the asset to produce bitcoin. The Company has full control of the mining equipment utilized in the mining pool, and if the Company determines it will increase or decrease the processing power of its machines and/or fleet (i.e., for repairs or when power costs are excessive) the computing power provided to the customer will be reduced.

Step 3: The transaction consideration the Company earns is non-cash digital consideration in the form of bitcoin, which the Company measures at fair value on the date earned and is the same at contract inception per Step 1. According to the customer contract, daily earnings are calculated from midnight-to-midnight UTC time, and the sub-account balance is credited one hour later at 1 AM UTC time. The Company utilizes Greenwich Mean Time (GMT), which is also the midnight of Universal Time Coordinated (UTC), since this is consistent with our customer contract in calculating our daily earnings from midnight-to-midnight UTC time.

The transaction consideration the Company earns is all variable since it is dependent on the daily computing power provided by the Company. The Company’s bitcoins earned through the contractual payout formula is not known until the Company’s computational hashrate contributed over the daily measurement period is fulfilled over time daily between midnight-to-midnight UTC time. The Company’s proportionate amount of the global network transaction fee rewards earned are calculated at the end of each transactional day. There are no other forms of variable considerations, such as discounts, rebates, refunds, credits, price concessions, incentives, performance bonuses, penalties, or other similar items.

The Company fully constrains all variable consideration as a result of ASC 606-10-32-12a because the amount of consideration is highly susceptible to factors outside of our control as defined by the Company’s customer’s payout methodology. The variable consideration is constrained until the Company can reasonably estimate the amount of mining rewards by the end of a given transactional day based on the actual amount of computing power provided to the mining pool operators. By then, the Company considers it is highly probable that a significant reversal in the amount of revenues will not occur and includes such variable consideration in the transaction price.

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

Step 4: The transaction price is allocated to the single performance obligation upon verification for the provision of computing power to the mining pool operator. There is a single performance obligation (i.e., computing power or hashrate) for the contract; and therefore, all consideration from the mining pool operator is allocated to this single performance obligation.

Step 5: The Company’s performance is complete in transferring the hashrate service over-time to the customer and the customer obtains control of that asset. As such, the Company records its share of the bitcoins earned from the customer within an hour of the close of the reporting date at midnight UTC per the payout formula of the customer contract.

In exchange for providing computing power, the Company is entitled to a pro-rata share of the fixed bitcoin awards earned over the measurement period, plus a pro-rata fractional share of the global transaction fee rewards for the respective measurement period, less net digital asset fees due to the mining pool operator over the measurement period, as applicable. The transaction consideration the Company receives is non-cash consideration, in the form of bitcoin. The Company measures the bitcoin, which the Company measures at fair value on the date earned using the closing price of bitcoin on the date earned (midnight UTC).

Bitcoin, page F-17

Response:

The Company acknowledges the Staff’s comment and respectfully submits that as disclosed in our initial response that the “impairment analysis on bitcoin, performed quarterly, compares the carrying amount of each bitcoin to the lowest daily closing bitcoin price during such quarter.” The fair value of bitcoin pricing is derived daily from NASDAQ.com and the Company compares the quoted price from NASDAQ.com to other sources to ensure there is no material variance in quoted pricing. The Company selected

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

NASDAQ.com due to its consistent daily activity, whereas other sources were not as reliable on a daily basis. The Company utilizes quotes from NASDAQ.com to impair its bitcoin balances on a daily basis, using bitcoin price as of midnight Greenwich Mean Time (GMT).

However, the Company has subsequently determined that its method of calculating impairment of its bitcoin assets (which are combined into a single unit of accounting for purposes of testing impairment since they are operated as a single asset), on a daily basis using a daily closing price at a standard cutoff time, was not in compliance with the ASC 350-30-35-19 requirement to recognize impairment whenever carrying value exceeds fair value. Effectively, the Company determined that ASC 350-30-35-19 calls for the intraday low price of Bitcoin to be utilized in calculating impairment of the Company’s bitcoin held as that metric is the most accurate indicator of whether it is more likely than not that the asset is impaired. Accordingly, the Company did an analysis and concluded that the impact to the consolidated results of operations and consolidated balance sheet as of and for the fiscal years ended September 30, 2022, September 30, 2021 and the three-month period ended December 31, 2022 are immaterial. As indicated in the Company’s previous response to comment 22, the Company utilizes the sales of bitcoin to assist in funding operations and investing activities and accordingly typically holds minimal quantities of bitcoin at each period end (42 days’ and 19 days’ worth of bitcoin mining as of September 30, 2022 and December 31, 2022, respectively).

The Company further acknowledges the Staff’s comment “explain how you consider a qualitative assessment given the existence of a quoted price on apparently active markets,” and respectfully submits the Company does not perform a qualitative assessment for impairments of bitcoin as allowed under ASC 350-30-35-18A and therefore goes directly to the quantitative analysis for each reporting period. The Company will enhance disclosures in future filings regarding the application allowed in ASC 350-30-35-18A.

Response:

The Company acknowledges the Staff’s comment and respectfully submits that the Company utilizes the Coinbase exchange to sell its bitcoin. In connection with ASC

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

820-10-35-5a, the Company considers Coinbase as the principal market. The Company utilizes Nasdaq.com for all of its other bitcoin transactions (revenue and impairment). The Company recognizes the inconsistency and in accordance with ASC 820, will adjust its measurement base for recognizing revenue and measuring impairment for all subsequent periods, beginning with the quarter ended March 31, 2023 to the same principal market quotes, from Coinbase. As a result of the above, the Company performed an analysis and concluded the impact/variance between the daily closing price and the intra-day low between Nasdaq.com and Coinbase are not significant and for similar reasons as described in the Company’s response in question #11, should not require adjustment to previously filed financial statements.

Response:

The Company acknowledges the Staff’s comment and respectfully submits that in future filings the Company will enhance disclosure to explain its accounting policy for classifying bitcoin as a current asset. In the Company’s upcoming Second Quarter 10-Q, the disclosure below will be included in Note 2 – Significant Accounting Policies.

Bitcoin are included in current assets in the consolidated balance sheets due to the Company’s ability to sell it in a highly liquid marketplace and its intent to liquidate its Bitcoin to support operations when needed.

Form 10-Q for the Quarterly Period Ended December 31, 2022

Non-GAAP Measures, page 11

Response:

The Company acknowledges the Staff’s comment and respectfully submits that it will revise its non-GAAP presentation in its future filings to exclude the adjustments for other impairment expense (related to bitcoin) and realized gains and loss on sale of bitcoin.

Consolidated Statements of Cash Flows, page F-8

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

Response:

The Company acknowledges the Staff’s comment and respectfully submits that, after evaluating guidance in ASC 230-Statement of Cash Flows, that the sales of the bitcoin are not specifically identified as cash inflow transactions that qualify as investing activities. Accordingly, cash inflows from operating activities include all items not described or included as an investing or financing cash inflow. Further, consideration of this classification is that the bitcoin generated is reported as revenues and the current average holding period of bitcoin is less than one (1) month. Consistent with ASC 230-10-20 Glossary, the proceeds from the sale of bitcoin are the result of the Company producing and delivering computing power services to its customer and thus represent operating activities. These are cash flows from transactions that enter into the determination of the Company’s net income (loss).

Note 2. Summary of Significant Accounting Policies

Bitcoin, page F-15

Response:

The Company acknowledges the Staff’s comment and respectfully submits that in future filings that roll-forward of bitcoin will remove the proceeds from Sale of bitcoin and Realized loss (gain) on sale of bitcoin and replace them with the carrying value of the bitcoin sold.

Response:

The Company acknowledges the Staff’s comment and respectfully submits that the disclosure on page F-15 of the Company’s Quarterly Report on Form 10-Q for the Quarterly Period Ended December 31, 2022 was incorrect and that Realized loss (gain) on sale of bitcoin is included in Total Costs and Expenses on the consolidated Statements of

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2

Operations and Comprehensive Income (Loss) as disclosed on page F-3. The disclosure will be presented in a manner consistent with the disclosure on page F-3 in all future filings.

///

///

///

We appreciate the Staff’s time and attention and we hope that the foregoing has been responsive to the Staff’s comments. If you have any further questions or need any additional information, please feel free to contact the undersigned at 702-989-7692 ext. 700 or Mark D. Wood of our counsel Katten Muchin Rosenman LLP at 312-902-5493 or mark.wood@katten.com at your convenience.

Sincerely, |

|

|

|

/s/ Gary A. Vecchiarelli |

|

Gary A. Vecchiarelli |

|

Chief Financial Officer |

|

|

|

|

|

|

|

cc: Mark D. Wood

Katten Muchin Rosenman LLP

DOCPROPERTY "CUS_DocIDChunk0" 157102389v2