Exhibit 99.1

UCOMMUNE INTERNATIONAL LTD

Index to the unaudited condensed consolidated financial statements

F-1

UCOMMUNE

INTERNATIONAL LTD

CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in thousands, except share and per share data, or otherwise noted)

| As of December 31, | As of June 30, | |||||||||||

| 2023 | 2024 | |||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Note 2d) | |||||||||||

| ASSETS | ||||||||||||

| Current assets: | ||||||||||||

| Cash and cash equivalents | ||||||||||||

| Restricted cash, current | ||||||||||||

| Short-term investments | ||||||||||||

| Accounts receivable, net of allowance of RMB | ||||||||||||

| Prepaid expenses and other current assets, net | ||||||||||||

| Amounts due from related parties, current | ||||||||||||

| Total current assets | ||||||||||||

| Non-current assets | ||||||||||||

| Long-term investments | ||||||||||||

| Property and equipment, net | ||||||||||||

| Right-of-use assets, net | ||||||||||||

| Intangible assets, net | ||||||||||||

| Rental deposit | ||||||||||||

| Other assets, non-current | ||||||||||||

| Total non-current assets | ||||||||||||

| TOTAL ASSETS | ||||||||||||

F-2

UCOMMUNE

INTERNATIONAL LTD

CONDENSED CONSOLIDATED BALANCE SHEETS — (Continued)

(Amounts in thousands, except share and per share data, or otherwise noted)

| As of December 31, | As of June 30, | |||||||||||

| 2023 | 2024 | |||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Note 2d) | |||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||||||

| Current liabilities: | ||||||||||||

| Accounts payable | ||||||||||||

| Accrued expenses and other current liabilities | ||||||||||||

| Amounts due to related parties, current | ||||||||||||

| Deferred workspace membership fee | ||||||||||||

| Contract liabilities | ||||||||||||

| Income taxes payable | ||||||||||||

| Deferred subsidy income | ||||||||||||

| Lease liabilities, current | ||||||||||||

| Total current liabilities | ||||||||||||

F-3

UCOMMUNE

INTERNATIONAL LTD

CONDENSED CONSOLIDATED BALANCE SHEETS — (Continued)

(Amounts in thousands, except share and per share data, or otherwise noted)

| As of December 31, | As of June 30, | |||||||||||

| 2023 | 2024 | |||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Note 2d) | |||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||||||

| Non-current liabilities: | ||||||||||||

| Refundable deposits from members, non-current | ||||||||||||

| Lease liabilities, non-current | ||||||||||||

| Warrant liabilities | ||||||||||||

| Total non-current liabilities | ||||||||||||

| TOTAL LIABILITIES | ||||||||||||

| Commitments and contingencies (Note 16) | ||||||||||||

| SHAREHOLDERS’ EQUITY | ||||||||||||

| Class A ordinary shares ( | ||||||||||||

| Class B ordinary shares ( | ||||||||||||

| Additional paid-in capital | ||||||||||||

| Statutory reserves | ||||||||||||

| Accumulated deficit | ( | ) | ( | ) | ( | ) | ||||||

| Accumulated other comprehensive income | ||||||||||||

| Total Ucommune International Ltd shareholders’ equity | ||||||||||||

| Noncontrolling interests | ||||||||||||

| TOTAL EQUITY | ||||||||||||

| TOTAL LIABILITIES AND EQUITY | ||||||||||||

| (i) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

F-4

UCOMMUNE

INTERNATIONAL LTD

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Amounts in thousands, except share and per share data, or otherwise noted)

| For the Six Months Ended June 30, | ||||||||||||

| 2023 | 2024 | 2024 | ||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Unaudited) | (Note 2d) | ||||||||||

| Revenue: | ||||||||||||

| Total revenue | ||||||||||||

| Cost of revenue: | ||||||||||||

| ( | ) | ( | ) | ( | ) | |||||||

| ( | ) | ( | ) | ( | ) | |||||||

| Other services | ( | ) | ( | ) | ( | ) | ||||||

| Total cost of revenue | ( | ) | ( | ) | ( | ) | ||||||

| Operating expenses: | ||||||||||||

| Impairment loss on long-lived assets and long-term prepaid expenses | ( | ) | ( | ) | ( | ) | ||||||

| Sales and marketing expenses | ( | ) | ( | ) | ( | ) | ||||||

| General and administrative expenses | ( | ) | ( | ) | ( | ) | ||||||

| Change in fair value of warrant liability | ||||||||||||

| Change in fair value of put option liability | ||||||||||||

| Loss from operations | ( | ) | ( | ) | ( | ) | ||||||

| Interest (expense)/income, net | ( | ) | ||||||||||

| Subsidy income | ||||||||||||

| Impairment on long-term investments | ( | ) | ( | ) | ( | ) | ||||||

F-5

UCOMMUNE

INTERNATIONAL LTD

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS — (Continued)

(Amounts in thousands, except share and per share data, or otherwise noted)

| For the Six Months Ended June 30, | ||||||||||||

| 2023 | 2024 | 2024 | ||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Unaudited) | (Note 2d) | ||||||||||

| Gain/(loss) on disposal of subsidiaries | ( | ) | ( | ) | ||||||||

| Other expense, net | ( | ) | ( | ) | ( | ) | ||||||

| Loss before income taxes and loss from equity method investments | ( | ) | ( | ) | ( | ) | ||||||

| Provision for income taxes | ( | ) | ( | ) | ( | ) | ||||||

| Loss from equity method investment | ( | ) | ( | ) | ( | ) | ||||||

| Net loss | ( | ) | ( | ) | ( | ) | ||||||

| Less: Net loss attributable to noncontrolling interests | ( | ) | ( | ) | ( | ) | ||||||

| Net loss attributable to Ucommune International Ltd | ( | ) | ( | ) | ( | ) | ||||||

| Net loss per share attributable to ordinary shareholders of Ucommune International Ltd(i) | ||||||||||||

| ( | ) | ( | ) | ( | ) | |||||||

| Weighted average shares used in calculating net loss per share(i) | ||||||||||||

| (i) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

F-6

UCOMMUNE

INTERNATIONAL LTD

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(Amounts in thousands, except share and per share data, or otherwise noted)

| For the Six Months Ended June 30, | ||||||||||||

| 2023 | 2024 | 2024 | ||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Unaudited) | (Note 2d) | ||||||||||

| Net loss | ( | ) | ( | ) | ( | ) | ||||||

| Other comprehensive (loss)/income, net of tax | ||||||||||||

| Foreign currency translation adjustments | ( | ) | ||||||||||

| Total Comprehensive loss | ( | ) | ( | ) | ( | ) | ||||||

| Less: Comprehensive loss attributable to noncontrolling interest | ( | ) | ( | ) | ( | ) | ||||||

| Comprehensive loss attributable to Ucommune International Ltd’s shareholders | ( | ) | ( | ) | ( | ) | ||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

F-7

UCOMMUNE

INTERNATIONAL LTD

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

(Amounts in thousands, except share and per share data, or otherwise noted)

| Ordinary Shares | Additional paid-in | Statutory | Accumulated | Accumulated other comprehensive | Total Ucommune International Ltd shareholders’ | Noncontrolling | Total | |||||||||||||||||||||||||||||

| Shares(i) | Amount | capital | Reserve | deficit | loss | equity | interests | equity | ||||||||||||||||||||||||||||

| Balance as of December 31, 2022 in RMB | ( | ) | ||||||||||||||||||||||||||||||||||

| Adoption of ASC 326 | — | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Net loss | — | ( | ) | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | ( | ) | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||

| Provision for statutory reserve | — | ( | ) | |||||||||||||||||||||||||||||||||

| Shares issued for conversion of convertible debt | ||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | |||||||||||||||||||||||||||||||||||

| Disposal of subsidiaries | — | ( | ) | ( | ) | |||||||||||||||||||||||||||||||

| Balance as of June 30, 2023 in RMB (unaudited) | ( | ) | ||||||||||||||||||||||||||||||||||

| Balance as of December 31, 2023 in RMB | ( | ) | ||||||||||||||||||||||||||||||||||

| Net loss | — | ( | ) | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||

| Foreign currency translation adjustment | — | ( | ) | |||||||||||||||||||||||||||||||||

| Capital contribution from shareholder | ||||||||||||||||||||||||||||||||||||

| Exercise of Warrant | ||||||||||||||||||||||||||||||||||||

| Stock-based compensation | ||||||||||||||||||||||||||||||||||||

| Capital contribution from noncontrolling shareholders | — | |||||||||||||||||||||||||||||||||||

| Disposal of subsidiaries | — | ( | ) | ( | ) | |||||||||||||||||||||||||||||||

| Balance as of June 30, 2024 in RMB (unaudited) | ( | ) | ||||||||||||||||||||||||||||||||||

| Balance as of June 30, 2024 in USD (unaudited) | ( | ) | ||||||||||||||||||||||||||||||||||

| (i) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

F-8

UCOMMUNE

INTERNATIONAL LTD

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in thousands, except share and per share data, or otherwise noted)

| For the Six Months Ended June 30, | ||||||||||||

| 2023 | 2024 | 2024 | ||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Unaudited) | (Note 2d) | ||||||||||

| Net cash provided by/(used in) operating activities | ( | ) | ( | ) | ||||||||

| Cash flows from investing activities | ||||||||||||

| Purchase of short-term investments | ( | ) | ( | ) | ( | ) | ||||||

| Redemption of short-term investments | ||||||||||||

| Purchase of property and equipment | ( | ) | ( | ) | ( | ) | ||||||

| Proceeds from disposal of property and equipment | ||||||||||||

| Cash deduction due to disposal of subsidiaries | ( | ) | ( | ) | ( | ) | ||||||

| Net used in investing activities | ( | ) | ( | ) | ( | ) | ||||||

| Cash flows from financing activities | ||||||||||||

| Capital contribution from shareholders | ||||||||||||

| Capital contribution from noncontrolling shareholders | ||||||||||||

| Loan received from related parties | ||||||||||||

| Loan repaid to related parties | ( | ) | ||||||||||

| Loan received from third parties | ||||||||||||

| Loan repaid to third parties | ( | ) | ( | ) | ( | ) | ||||||

| Cash received from exercise of warrant | ||||||||||||

| Net cash (used in)/provided by financing activities | ( | ) | ||||||||||

| Effects of exchange rate changes | ( | ) | ||||||||||

| Net increase in cash, cash equivalents and restricted cash | ||||||||||||

| Cash, cash equivalents and restricted cash – beginning of the period | ||||||||||||

| Cash, cash equivalents and restricted cash – end of the period | ||||||||||||

| Supplemental disclosure of cash flow information: | ||||||||||||

| Interest paid | ||||||||||||

| Income taxes paid | ||||||||||||

| Supplemental disclosure of noncash information: | ||||||||||||

| Payable for purchase of property and equipment | ||||||||||||

| Right-of-use assets obtained in exchange for new operating lease liabilities | ||||||||||||

| ROU assets disposed as reduction of operating lease liabilities due to lease termination | ||||||||||||

| Conversion of convertible bond’s principle | ||||||||||||

| Disposal of properties and prepaid expenses and other current assets in exchange for long-term investments | ||||||||||||

| Settlement of accrued expenses and other current liabilities with other non-current assets | ||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

F-9

UCOMMUNE

INTERNATIONAL LTD

NOTES TO UNAUDITED CONDENSED CONSOLIDATED STATEMENTS

FOR THE SIX MONTHS ENDED JUNE 30, 2023 and 2024

(Amounts in thousands, except share and per share data, or otherwise noted)

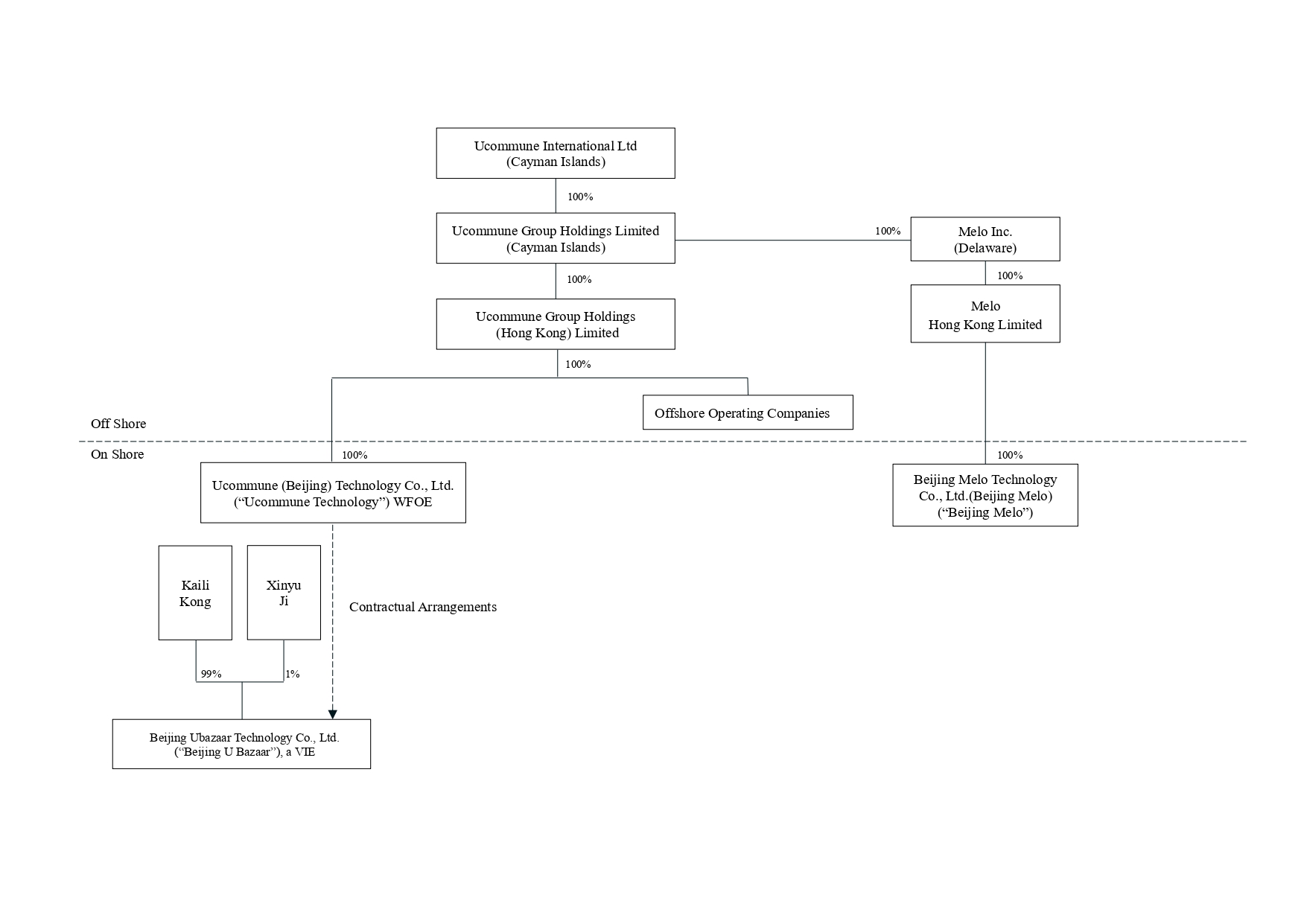

| 1. | ORGANIZATIONS AND PRINCIPAL ACTIVITIES |

Ucommune Group Holdings Limited (“Ucommune Group”) was founded in 2018 and was incorporated in the Cayman Islands. On June 29, 2020, Orisun Acquistion Corp. (“Orisun”), a special purpose acquisition company (“SPAC”), entered into a share exchange agreement (the “Share Exchange Agreement”) with Ucommune Group. Pursuant to the Share Exchange Agreement, Ucommune International Ltd (“the Company”), which is a subsidiary wholly owned by Orisun, acquired all of the issued and outstanding ordinary shares of Ucommune Group from the shareholders of Ucommune Group by newly issuing ordinary shares of Orisun to the shareholders of Ucommune Group (“SPAC Transaction”). The SPAC Transaction was consummated on November 17, 2020. Ucommune Group’s shareholders remains the controlling financial interests of Ucommune Group after the SPAC Transaction, which was accounted for as a reverse recapitalization. In connection with the closing of the SPAC Transaction, Orisun had been ceased and Ucommune International Ltd continued as the surviving company.

Ucommune International Ltd, its consolidated subsidiaries, variable interest entities (“VIEs”) and VIEs’ subsidiaries (collectively referred to as the “Group”) is primarily engaged in providing long-term leasing, on-demand and short-term leasing solutions to freelancers, start-up entrepreneurs, small medium enterprises and corporations by delivering well-furnished and fully-serviced space on a flexible basis in the People’s Republic of China (“PRC”). The individuals and enterprises registered on U bazaar, a mobile app of the Group are referred to as members.

| a. | The VIE arrangements |

The Company operates substantially all of its business through its VIEs including Ucommune Venture and Beijing U Bazaar. On May 20, 2019, WFOE entered into a series of contractual arrangements with Ucommune Venture, Beijing U Bazaar, and the respective equity interest holders. The series of contractual agreements include exclusive business cooperation agreement, exclusive call option agreement, equity pledge agreement, powers of attorney and spousal consent letters.

The Group believes that these contractual arrangements enable the Company to (1) have power to direct the activities that most significantly affects the economic performance of the VIEs, and (2) receive the economic benefits of the VIEs that could be significant to the VIEs. Accordingly, the Company is considered the primary beneficiary of the VIEs and is able to consolidate the VIEs and VIEs’ subsidiaries.

The

Group’s business has been directly operated by the VIEs and their subsidiaries. As of December 31, 2023, and June 30, 2024,

the VIEs and their subsidiaries accounted for an aggregate of

| As of December 31, | As of June 30, | |||||||||||

| 2023 | 2024 | |||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Note 2d) | |||||||||||

| Cash and cash equivalents | ||||||||||||

| Other current assets | ||||||||||||

| Total current assets | ||||||||||||

| Property and equipment, net | ||||||||||||

| Right-of-use assets, net | ||||||||||||

| Other non-current assets | ||||||||||||

| Total non-current assets | ||||||||||||

| TOTAL ASSETS | ||||||||||||

| Accounts payable | ||||||||||||

| Lease liabilities, current | ||||||||||||

| Other current liabilities | ||||||||||||

| Total current liabilities | ||||||||||||

| Lease liabilities, non-current | ||||||||||||

| Other non-current liabilities | ||||||||||||

| Total non-current liabilities | ||||||||||||

| Total liabilities | ||||||||||||

F-10

| For the Six Months Ended June 30, | ||||||||||||

| 2023 | 2024 | 2024 | ||||||||||

| RMB | RMB | USD | ||||||||||

| (Unaudited) | (Unaudited) | (Note 2d) | ||||||||||

| Net revenues | ||||||||||||

| Net loss | ( | ) | ( | ) | ( | ) | ||||||

| Net cash provided by/(used in) operating activities | ( | ) | ( | ) | ||||||||

| Net cash (used in)/provided by investing activities | ( | ) | ||||||||||

| Net cash (used in)/provided by financing activities | ( | ) | ||||||||||

There are no consolidated VIEs’ assets that are collateral for the VIEs’ obligations. No creditors (or beneficial interest holders) of the VIEs have recourse to the general credit of the Company or any of its consolidated subsidiaries. No terms in any arrangements, considering both explicit arrangements and implicit variable interests, require the Company or its subsidiaries to provide financial support to the VIEs. However, if the VIEs ever need financial support, the Company or its subsidiaries may, at its option and subject to statutory limits and restrictions, provide financial support to the VIE through loans to the shareholders of the VIEs or entrustment loans to the VIEs.

| b. | Recent development |

Substantially all of the Group’s revenues and workforce are concentrated in China. COVID-19 has resulted in a material and negative effect on the economy and rental market in China and caused loss of the Group’s business, closure and disposal of unprofitable spaces in operation during the year 2023 and in the first half of 2024, which in turn resulted in a decrease in revenue of workspace membership services. The Group’s financial position, results of operations and cash flows could be adversely affected to the extent that the outbreak harms the Chinese economy in general.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

| a. | Basis of presentation and use of estimates |

The accompanying condensed consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (U.S. GAAP) and pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (the “SEC”) which include the Company, its subsidiaries, its VIEs and VIEs’ subsidiaries. These accounting principles require management to make certain estimates and assumptions that affect the amounts in the accompanying financial statements. Actual results may differ from those estimates. The Group bases its estimates on past experience and various other factors believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not readily apparent from other sources.

F-11

Significant accounting estimates reflected in the Group’s financial statements include, but are not limited to, valuation allowance for deferred tax assets, incremental borrowing rate, allowance for credit losses, impairment of right-of-use (“ROU”) assets, other long-lived assets and long-term investments, and valuation of the Group’s warrant liabilities. Actual results may differ materially from those estimates.

| b. | Going Concern |

The accompanying condensed consolidated financial statements have been prepared assuming that the Group will continue as a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The realization of assets and the satisfaction of liabilities in the normal course of business is dependent on, among other things, the Group’s ability to generate sufficient cash flows from operations, and the Group’s ability to arrange adequate financing arrangements.

The

Group has incurred recurring operating losses since its inception, including net losses of RMB

Historically, the Group has relied principally on both operational sources of cash and non-operational sources of financing to fund its operations and business development. The Group’s ability to continue as a going concern is dependent on management’s ability to successfully execute its business plan which includes continued business transition from asset-heavy model to asset-light model in order to improve the profitability, continued exploration of new business opportunities that have synergies with the Company’s core business, controlling operating costs and optimizing operational efficiency to improve the Group’s cash flow from operations. The Group also plans to raise additional capital, including among others, obtaining debt and equity financing, to support its future operation.

The Group continues to explore opportunities to grow its business. However, it has not yet achieved a business scale that is able to generate a sufficient level of revenues to achieve net profit and positive cash flows from operating activities, and the Group expects the operating losses and negative cash flows from operations will continue for the foreseeable future. If it is unable to grow the business to achieve economies of scale in the future, it will become even more difficult for the Group to sustain a sufficient source of cash to cover its operating costs. There can be no assurance, however, that the Group will be able to obtain additional financing on terms acceptable to the Group, in a timely manner, or at all. In the event that financing sources are not available, or that the Group is unsuccessful in increasing its gross profit margin, push collection of long term receivables and reducing operating losses, the Group may be unable to implement its current plans for expansion, repay debt obligations or respond to competitive pressures, any of which would have a material adverse effect on the Group’s business, financial condition and results of operations and would materially adversely affect its ability to continue as a going concern.

The Group’s condensed consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and liquidation of liabilities in the normal course of business. The condensed consolidated financial statements do not include any adjustments that might result from the outcome of such uncertainties.

| c. | Impairment of ROU assets and other long-lived assets |

The Group reviews its ROU assets and other long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may no longer be recoverable. Factors the Group considers to be important which could trigger an impairment review primarily includes (a) Significant underperformance relative to projected operating results; (b) Significant changes in the overall business strategy; (c) Significant adverse changes in legal or business environment and (d) Significant competition, unfavorable industry trend, or economic outlook. When these events occur, the Group measures impairment by comparing the carrying value of the ROU assets and property and equipment to the estimated undiscounted future cash flows expected to result from the use of the assets and their eventual disposal. If the sum of the expected undiscounted cash flow is less than the carrying amount of the assets, the Group would recognize an impairment loss based on excess of carrying value over the fair value of the assets. The Company measured the fair value of impaired space by using discounted cash flow model. The estimates used in projected future cash flows include rental charges and occupancy rate. The gross yield rate is used as the discount rate.

F-12

The Group reviews its other non-current assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may no longer be recoverable. Factors the Group considers to be important which could trigger an impairment review primarily includes (a) Significant adverse changes in legal or business environment and (b) significant competition, unfavorable industry trend, or economic outlook. When these events occur, the Group measures impairment by comparing the carrying value of the non-current assets to the estimated collection of receivables.

The

Group recorded and RMB

| d. | Convenience translation |

The Group’s business is primarily conducted in China and substantially all of the revenues are denominated in Renminbi (“RMB”). However, periodic reports made to shareholders will include current period amounts translated into US dollars using the exchange rate as of balance sheet date, for the convenience of the readers. No representation is made that the RMB amounts could have been, or could be, converted, realized or settled into USD at that rate on June 30, 2024, or at any other rate.

| e. | Allowance for credit losses |

On

January 1, 2023, the Group adopted ASC 326, Credit Losses (“ASC 326”) which replaced previously issued guidance regarding

the impairment of financial instruments with an expected loss methodology that will result in more timely recognition of credit losses.

The Group used a modified retrospective approach and did not restate the comparable prior periods, which resulted in RMB

Upon adoption of ASC 326, the Group maintains an allowance for credit losses in accordance with ASC 326 and records the allowance for credit losses as an offset to assets such as accounts receivable, prepayments and other current assets and due from related parties which are not under common control, etc., and the estimated credit losses charged to the allowance is classified as “General and administrative expenses” in the consolidated statements of operations. The Group assesses collectability by reviewing receivables on a collective basis where similar characteristics exist, primarily based on size, nature and on an individual basis when we identify specific customers with known disputes or collectability issues. In determining the amount of the allowance for credit losses, the Group considers historical collectability based on past due status, the age of the receivable balances, credit quality of the Group’s customer or vendor based on ongoing credit evaluations, current economic conditions, reasonable and supportable forecasts of future economic conditions, and other factors that may affect the Group’s ability to collect from customers. Bad debts are written off as incurred. The Group generally does not require collateral from its customers.

| f. | Long-term investments |

The Group’s long-term investments include equity securities without readily determinable fair values and equity method investments.

F-13

Equity securities without readily determinable fair values

For equity securities without readily determinable fair value, the Group elected to use the measurement alternative to measure those investments at cost, minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for identical or similar investments of the same issuer. The adoption did not have a material impact on the Group’s consolidated financial position or results of operations, in accordance with ASC Topic 321, Investments—Equity Securities.

The Group reviews its equity securities without readily determinable fair value for impairment at each reporting period. If a qualitative assessment indicates that the investment is impaired, the Group estimates the investment’s fair value in accordance with the principles of ASC Topic 820—Fair Value Measurement (“ASC 820”). If the fair value is less than the investment’s carrying value, the Group would recognize an impairment loss in the consolidated statements of operations.

Equity method investments

Investee

companies over which the Group has the ability to exercise significant influence, but does not have a controlling interest through investment

in common shares or in-substance common shares, are accounted for using the equity method. Significant influence is generally considered

exist when the Group has an ownership interest in the voting stock of the investee between

Under the equity method, the Group initially records its investment at cost and subsequently recognizes the Group’s proportionate share of each equity investee’s net income or loss after the date of investment into accumulated deficit and accordingly adjusts the carrying amount of the investment. The Group reviews its equity method investments for impairment whenever an event or circumstance indicates that any other-than-temporary impairment (“OTTI”) has occurred. The Group considers available quantitative and qualitative evidence in evaluating potential impairment of its equity method investment.

An impairment charge is recorded when the carrying amount of the investment exceeds its fair value and this condition is determined to be other-than-temporary.

Nonmonetary transactions

The Group engages in nonmonetary exchanges of equity interest of certain long-term investments. The transaction price of the nonmonetary consideration is based on the fair values of the assets involved. The cost of equity interest acquired in exchange is initially measured at the fair value of the assets the Group surrendered to obtain them.

| g. | Convertible bond and detachable warrants |

The Group issued convertible bond with detachable warrants in January 2022. The Group has evaluated that the convertible bond with detachable warrants is a bundle of freestanding financial instruments and should be separately accounted. With respect to the convertible bond, the Group has evaluated whether the conversion feature of the bond is considered an embedded derivative instrument subject to bifurcation in accordance with ASC 815 —Accounting for Derivative Instruments and Hedging Activities (“ASC 815”). Based on the Group’s evaluation, the conversion feature is not considered to be bifurcated because the conversion feature is either clearly and closely related to the Convertible Bond or meet the scope exception under ASC 815-10-15. The Group has determined that there was no beneficial conversion feature attributable to the convertible bond, as the adoption of ASU 2020-06 since January 1, 2022.

The Group has evaluated the embedded put option in accordance with ASC815 has had determined the put option meet the definition of a derivative and need to be bifurcated and measured under the fair value as the convertible bond was issued at a substantial discount and is contingently exercisable. The Group classifies put option in its condensed consolidated balance sheets as a liability which is revalued at each balance sheet date subsequent to the initial issuance.

F-14

The Group has evaluated the detachable warrants in accordance with ASC 815 has had determined the detachable warrants meet the definition of a derivative and need to be measured under the fair value. The Group classifies warrants in its condensed consolidated balance sheets as a liability which is revalued at each balance sheet date subsequent to the initial issuance.

| h. | Lease |

The Group made an accounting policy election for all lease related asset classes, to account for the lease and non-lease components as a single lease component. The Group has also made an accounting policy election to exempt leases with an initial term of 12 months or less from being recognized on the balance sheet. Short-term leases are not significant in comparison to the Group’s overall lease portfolio. Payments related to those leases continue to be recognized in the consolidated statement of operations on a straight-line basis over the lease term.

From the Perspective of Lessee

The Group leases properties for its co-working space and other locations. At the commencement of each lease, management determines its classification as an operating or finance lease. For leases that qualify as operating leases, the Group recognizes the associated lease expense on a straight-line basis over the term of the lease beginning on the date of initial possession, which is generally when the Group enters the leased premises and begins to make improvements in preparation for its intended use.

At the commencement date of a lease, the Group recognizes a lease liability for future fixed lease payments and a ROU asset representing the right to use the underlying asset during the lease term.

The future fixed lease payments are discounted using the incremental borrowing rate as the rate implicit in the lease is not readily determinable. The incremental borrowing rate is estimated on a portfolio basis and incorporating lease term, currency risk, credit risk and an adjustment for collateral.

The Group uses the discount rate as of the commencement date of the lease, incorporating the entire lease term. Current maturities and long-term portions of operating lease liabilities are classified as lease liabilities, current and lease liabilities, non-current, respectively, in the consolidated balance sheets.

The ROU asset is measured at the amount of the lease liabilities with adjustments, if applicable, for lease prepayments made prior to or at lease commencement, initial direct costs incurred and lease incentives. Variable lease expenses include rent contingent payments based on percentages of revenue as defined in the lease. It is not included in lease expenses before it incurs or becomes probable.

From the Perspective of Lessor

The Group recognizes workspace membership revenue under ASC 842, and all the lease contracts are operating leases. The Group provides various leasing solutions for its members and generates revenues from monthly rent in the form of membership services fees or office desk rental fee. The workspace memberships enable members to access to office space, use of a shared internet connection, access to certain facilities (kitchen, common areas, etc.), as well as fee-based for the use of conference room. The price of each membership varies, based on the basis of the particular characteristics of the office space occupied by the member, the geographic location of the workspace, and the amount of desk space in the contract. The members do not have options to purchase underlying assets at termination. Renewal of memberships are on a negotiation basis before termination. The majority of the Group’s lease contracts are fixed lease payment contracts. The Group’s variable lease payments consist of certain contracts indexed to future sales revenues of the lessees. Variable membership fees are recognized when incurred. Workspace membership revenue consists primarily of fees from members and is recognized ratably, on a monthly basis, over the lease term, as access to office space is provided. The Group applied practical expedients to choose not to separate lease and non-lease components for all lease related asset classes. The consolidated component is accounted for under ASC842. The lease term for most of the membership services is less than one year. The leases do not have renewal options and penalty is imposed if the lessees early terminate the leases. Workspace membership fees are generally collected in advance each quarter. Members are generally required to provide the Group with a deposit which is normally one-month service fee. Pursuant to the term of membership agreement, the amount of deposit may be applied against the member’s unpaid balance.

F-15

The residual value of the Group’s lease assets represents the fair value of the leased assets at the end of the lease terms. The Group relies on industry data, historical experience, independent appraisals and the experience of the management team to value lease residuals.

| For the six months ended June 30, | ||||||||

| 2023 | 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Operating lease income from fixed payments | ||||||||

| Variable operating lease income | ||||||||

| Total | ||||||||

| RMB | ||||

| (Unaudited) | ||||

| For the six months period ending December 31, | ||||

| 2024 | ||||

| For the year ending December 31, | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| 2028 | ||||

| Thereafter | ||||

| Total | ||||

| i. | Revenue recognition |

Revenue is recognized when control of promised goods or services is transferred to the Group’s customers in an amount of consideration to which the Group expects to be entitled to in exchange for those goods or services. The Group follows the five steps approach for revenue recognition under Topic 606: (i) identify the contract(s) with a customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, (iv) allocate the transaction price to the performance obligations in the contract, and (v) recognize revenue when (or as) the Group satisfies a performance obligation.

The primary sources of the Group’s revenues are as follows:

| (i) | Workspace membership revenue |

As set out in Note 2 “Lease, from the perspective of lessor”, workspace membership revenue is recognized under ASC 842.

| (ii) | Marketing and branding services revenue |

The Group provides integrated branding services primarily including the tailor-made digital marketing strategy design and placement on different media platforms based on the customer’s needs in respective industries, including the internet, automobile, finance, electronics and consumer goods as the single performance obligation and revenue is recognized over time during the contract period under input method according to the actual placement. The Group also provides online targeted marketing services to provide marketing strategy design and placement on famous advertising platform for the promotion of the customer as the single performance obligation and recognize revenue over time during the contract period under output method according to the agreed settlement statement. The Group is the primary obligator and bearing the service risk of the marketing and branding services, and the Group has the right and ability to direct which media channel to place the advertisement to the customer on the Group’s behalf and has discretion in establishing the price for the service. So, the Group is identified as a principal.

F-16

| (iii) | Other services revenue |

Other services revenue primarily consists of 1) interior design and construction revenue, 2) co-working space management fees, 3) SaaS services, IOT solutions and technical support revenue and 4) charges to members for ancillary services including printing and copying, etc. The Group identified the services as one single performance obligation.

1) Interior design and construction revenue

The Group provides interior design service to customer for agreed location as the single performance obligation and recognizes interior design revenue over time upon the achievement of milestones, which represents the design stages agreed in the contract. The Group provides construction service as the single performance obligation and recognizes revenue using a cost-based input method that recognizes revenue as work is performed based on the relationship between actual costs incurred compared to the total estimated cost of the contract, to determine the Group’s progress towards contract completion and to calculate the corresponding amount of revenue to recognize. The Group has the right and ability to direct which sub-contractors or third-party designers to provide construction or design work for the customers, and the Group is the primary obligator and bearing the service risk of the interior design and construction services. So, the Group is identified as a principal.

2) Co-working space management fees

Co-working space management fees is derived from managing branded co-working space locations for leased property owners as the single performance obligation. The fee generally consists of a monthly base amount plus revenue sharing. The Group primarily charge landlords management fees for branding, consulting and operating services. The Group provide services within the contract term and recognizes revenue over time under output method when service is completed.

3) SaaS services, IOT solutions and technical support revenue

The Group recognizes revenue at a point in time for the SaaS services and IOT solutions revenue as the single performance obligation when service is completed, or devices are delivered to customers. The Group provides technical support services as the single performance obligation and recognizes revenue over time under output method because the customer simultaneously receives and consumes the benefits as the Group performs throughout a fixed term.

4) Ancillary services revenue

The Group recognizes revenue at a point in time when respective ancillary services including printing and copying services are rendered to members.

Contract liabilities primarily

result from the timing difference between the Group’s satisfaction of performance obligation and the customers’ payment. Substantial

all marketing and branding revenue, and other services revenue is recognized over time during the six months ended June 30, 2023 and 2024.

Balance of contract liabilities were RMB

F-17

| j. | Warrant liability |

In connection with the issuances of ordinary shares, the Group may issue options or warrants to purchase ordinary shares. In certain circumstances, these options or warrants may be classified as liabilities, rather than as equity.

Warrants classified as equity are initially recorded at fair value and subsequent changes in fair value are not recognized as long as the warrants continue to be classified as equity. Warrants classified as liabilities are initially recorded at fair value with gains and losses arising from changes in fair value recognized in the consolidated statements of operations during the period in which such instruments are outstanding.

| k. | Recent accounting pronouncements not yet adopted |

In November 2023, the FASB issued ASU No. 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures (“ASU 2023-07”), which requires an enhanced disclosure of significant segment expenses on an annual and interim basis. This guidance will be effective for the annual periods beginning after December 15, 2023, and for interim periods beginning January 1, 2025. Early adoption is permitted. Upon adoption, the guidance should be applied retrospectively to all prior periods presented in the financial statements. The Group is in the process of evaluation the impact of adopting this new guidance on its consolidated financial statements.

In December 2023, the FASB issued ASU No. 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures (“ASU 2023-09”), which improves the transparency of income tax disclosures by requiring consistent categories and greater disaggregation of information in the effective tax rate reconciliation and income taxes paid disaggregated by jurisdiction. It also includes certain other amendments to improve the effectiveness of income tax disclosures. This guidance will be effective for the annual periods beginning the year ending December 31, 2025. For entities other than public business entities, the amendments are effective for annual periods beginning after December 15, 2025. Early adoption is permitted. The Group is in the process of evaluation the impact of adopting this new guidance on its consolidated financial statements.

| 3. | RISKS AND CONCENTRATION |

Foreign currency risk

The

RMB is not a freely convertible currency. The State Administration for Foreign Exchange, under the authority of the Peoples Bank of China,

controls the conversion of RMB into other currencies. The value of the RMB is subject to changes in central government policies, international

economic and political developments affecting supply and demand in the China Foreign Exchange Trading System market. The Group’s

cash and cash equivalents denominated in RMB amounted to RMB

Concentration risks

Financial

instruments that potentially expose the Group to significant concentration of credit risk primarily consist of cash and cash equivalents

and short-term investments. As of December 31, 2023 and June 30, 2024, substantially all of the Group’s cash and cash equivalents

and short-term investments were deposited in financial institutions located in the PRC. There are two customers individually represent

There is one and three customers

individually represent greater than 10% of total accounts receivable as of June 30, 2023 and 2024, respectively. Their aggregated percentage

to total accounts receivable is

There is one and one supplier that individually represent greater than 10% of the total cost of revenue (excluding impairment loss) for the six months ended June 30, 2023 and 2024.

F-18

| 4. | ACCOUNTS RECEIVABLE, NET |

As of 2023 | As of June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| Account receivable | ||||||||

| Less: Allowance for credit losses | ( | ) | ( | ) | ||||

| Total | ||||||||

December 31, 2023 | June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| Balance at beginning of period | ||||||||

| Adoption of ASC 326 | ||||||||

| Amounts charged to/(reversed of) expenses | ( | ) | ||||||

| Amounts written off | ( | ) | ( | ) | ||||

| Disposal of a subsidiary | ( | ) | ||||||

| Balance at end of period | ||||||||

As

of December 31, 2023 and June 30, 2024, all accounts receivable was due from third party customers. Provision for credit losses for the

year ended December 31, 2023 was RMB

| 5. | PREPAID EXPENSES AND OTHER CURRENT ASSETS, NET |

| As of December 31, 2023 | As of June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| Advances to suppliers(i) | ||||||||

| Prepaid VAT | ||||||||

| Rental deposit, current | ||||||||

| Staff advances | ||||||||

| Prepaid consulting expenses | ||||||||

| Short-term construction deposits | ||||||||

| Prepaid short-term rent | ||||||||

| Interest receivable | ||||||||

| Receivables from third-party payment platform | ||||||||

| Receivables from Hunan Longxi | ||||||||

| Others(ii) | ||||||||

| Total | ||||||||

| Less: Allowance for credit losses | ( | ) | ( | ) | ||||

| Total | ||||||||

Notes:

| (i) |

| (ii) |

F-19

| December 31, 2023 | June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| Balance at beginning of period | ||||||||

| Adoption of ASC 326 | ||||||||

| Amounts charged to/(reversed of) expenses | ( | ) | ||||||

| Amounts written off | ( | ) | ( | ) | ||||

| Disposal of a subsidiary | ( | ) | ||||||

| Balance at end of period | ||||||||

Provision

for credit losses for prepayment and other current assets for the year ended December 31, 2023 was RMB

| 6. | PROPERTY AND EQUIPMENT, NET |

As of 2023 | As of June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| Leasehold improvement | ||||||||

| Buildings | ||||||||

| Furniture | ||||||||

| Office equipment | ||||||||

| Vehicles | ||||||||

| Total cost of property and equipment | ||||||||

| Less: Accumulated depreciation | ( | ) | ( | ) | ||||

| Impairment loss | ( | ) | ( | ) | ||||

| Total | ||||||||

F-20

Depreciation expenses for

the six months ended June 30, 2023 and 2024 were RMB

Impairment loss for the six months ended June 30, 2023 and 2024 were and , respectively.

Gain on disposal for the six

months ended June 30, 2023 was RMB

As of June 30, 2024, the Group had no significant outstanding capital commitments.

| 7. | LONG-TERM INVESTMENTS |

| As of December 31, | As of June 30, | |||||||

| 2023 | 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| Equity method investments: | ||||||||

| Shanghai Youmei Information Consulting Co., Ltd. (Youmei)(a) | ||||||||

| Qingdao Rongzemingzhi Network Technology Co., Ltd. (Rongzemingzhi)(b) | ||||||||

| Other equity method investments(c) | ||||||||

| Less: impairment loss on equity method investments | ( | ) | ( | ) | ||||

| Equity securities without readily determinable fair values investments: | ||||||||

| Hangzhou Renjunxing Technology Co., Ltd (Renjunxing)(d) | ||||||||

| Green fire Decoration Engineering (Beijing) Co., Ltd. (Green Fire)(e) | ||||||||

| Other equity securities without readily determinable fair values investments(f) | ||||||||

| Less: impairment loss on equity securities without readily determinable fair values investments | ( | ) | ( | ) | ||||

| Total | ||||||||

Notes:

| (a) |

| (b) |

| (c) |

F-21

| (d) |

| (e) |

| (f) |

| 8. | LEASE |

From the Perspective of Lessee

The Group leases real estate

for terms between

The Group sub-leased the leased premises to provide various lease solutions. All of the Group’s leases are operating leases under ASC 842.

As of 2023 | As of June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| ROU assets | ||||||||

| Operating lease liabilities – current | ( | ) | ( | ) | ||||

| Operating lease liabilities – non-current | ( | ) | ( | ) | ||||

| Weighted average remaining lease terms | ||||||||

| Weighted average incremental borrowing rate | % | % | ||||||

| For the six months ended June 30, 2023 | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Operating lease expenses for variable payments | ||||||||

| Operating lease expenses for fixed payments | ||||||||

| Short-term lease expenses | ||||||||

| Total | ||||||||

| For the six months ended June 30, 2023 | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Cash paid for amounts included in the measurement of lease liabilities: | ||||||||

| Operating cash flows for operating leases | ||||||||

F-22

| For the six months ended June 30, 2023 | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Operating lease liabilities arising from obtaining ROU assets | — | |||||||

| ROU assets disposed as reduction of operating lease liabilities due to lease termination | — | |||||||

| RMB | ||||

| (Unaudited) | ||||

| For the period ending December 31, | ||||

| 2024 | ||||

| For the year ending December 31, | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| 2028 | ||||

| Thereafter | ||||

| Total lease payments | ||||

| Less: imputed interest | ( | ) | ||

| Total lease liabilities | ||||

| 9. | ACCRUED EXPENSES AND OTHER CURRENT LIABILITIES |

As of 2023 | As of June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| Penalty payable(i) | ||||||||

| Refundable deposits from members, current | ||||||||

| Payable for investments and acquisitions | ||||||||

| Payable to former shareholders of acquirees | ||||||||

| Accrued payroll | ||||||||

| VAT payable | ||||||||

| Other taxes payable | ||||||||

| Interests payable | ||||||||

| Others | ||||||||

| Third-party loans(ii) | ||||||||

| Amounts reimbursable to employees | ||||||||

| Total | ||||||||

Notes:

| (i) |

| (ii) |

F-23

| 10. | COST OF REVENUE (EXCLUDING IMPAIRMENT LOSS) |

| For the six months ended June 30, 2023 | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Lease expenses | ||||||||

| Employee compensation and benefits | ||||||||

| Depreciation and amortization | ||||||||

| Advertising costs | ||||||||

| Construction and design costs | ||||||||

| Other operating costs(i) | ||||||||

| Total | ||||||||

Notes:

| (i) |

| 11. | INCOME TAXES |

Cayman Islands& BVI

The Company and Ucommune Group are tax-exempted companies incorporated in the Cayman Islands. A subsidiary, Ucommune International Limited, is incorporated in BVI. The foregoing companies are not subject to income tax.

United States (“U.S.”)

Melo and Ucommune N.Y. Corp.

are incorporated in the U.S. and are subject to the U.S. federal income taxes. According to U.S. tax reform, a flat corporate income tax

rate of

Hong Kong

Ucommune HK was established

in Hong Kong and is subject to a two-tiered income tax rate for taxable income earned in Hong Kong effectively since April 1,

2018. The first

Singapore

Ucommune Singapore Pte. Ltd.

and Ucommune Technology Pte. Ltd. were established in Singapore and are subject to Singapore corporate income taxes at the rate of

F-24

PRC

Effective from January 1,

2008, a new Enterprise Income Tax Law, or (“the New EIT Law”), combined the previous income tax laws for foreign invested

and domestic invested enterprises in the PRC by the adoption of a unified tax rate of

On May 25, 2022, the State

Finance and Taxation Department issued the Notice on Preferential Policies for Enterprise Income Tax in Hengqin Guangdong-Macao Deep Cooperation

Zone (hereinafter referred to as “Hengqin Shenhe District” or “Hengqin”) (Caishui [2022] No.19). And on February

17, 2023, Hengqin Guangdong-Macao Deep Cooperation Zone Taxation Bureau, State Administration of Taxation issued Announcement on Issues

Relating to the Substantial Operation of Eligible Industrial Enterprises in the Hengqin Guangdong-Macao Deep Co-operation Zone ([2023]

No. 1). These policies continue the policy of collecting enterprise income tax at a reduced preferential tax rate of

According to Caishui [2019]

No.13, announcement of the Ministry of Finance and the State Taxation Administration Caishui [2021] No.12, and announcement of the Ministry

of Finance and the State Taxation Administration [2023] No.12, small and low-profit enterprises shall meet three conditions for enjoying

preferential tax conditions, including (i) annual taxable income of no more than RMB

According to announcement

of the State Taxation Administration [2021] No.8, which became effective on January 1, 2021 and until to December 31, 2022, small, low-profit

enterprises whose annual taxable income is no more than RMB

According to announcement

of the Ministry of Finance and the State Taxation Administration [2022] No.13, which became effective on January 1, 2022 and until to

December 31, 2024, small, low profit enterprises whose annual taxable income exceed RMB

In accordance with announcement

of the Ministry of Finance and the State Taxation Administration [2023] No. 6, which was effective from January 1, 2023 to December 31,

2024, preferential tax rate became

According to announcement

of the Ministry of Finance and the State Taxation Administration [2023] No.12, which became effective on August 2, 2023 and until to December

31, 2027, small, low profit enterprises is subject to the preferential income tax rate of

| For the six months ended June 30, 2023 | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Current tax expense | ||||||||

| Deferred tax benefit | ( | ) | ||||||

| Total | ||||||||

F-25

| As of December 31, 2023 | As of June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | ||||||||

| Deferred tax assets: | ||||||||

| Allowance for credit losses | ||||||||

| Impairment loss on long-lived assets and long-term prepaid expenses | ||||||||

| Impairment loss on long-term investments | ||||||||

| Accrued Liabilities | ||||||||

| Deductible temporary difference related to advertising expenses | ||||||||

| Deferred subsidy income | ||||||||

| Net operating loss carrying forwards | ||||||||

| Total deferred tax assets | ||||||||

| Less: valuation allowance | ( | ) | ( | ) | ||||

| Deferred tax assets, net | ||||||||

| RMB | ||||

| Net change of valuation allowance of Deferred tax assets | ||||

| Balance at December 31, 2022 | ||||

| Additions-change to tax expense | ||||

| NOL Reductions/expirations | ( | ) | ||

| Balance at December 31, 2023 | ||||

| Additions-change to tax expense | ||||

| NOL Reductions/expirations | ( | ) | ||

| Balance at June 30, 2024 (Unaudited) | ||||

F-26

The aggregate NOLs as of

June 30, 2024 was RMB

The Group does not file combined

or consolidated tax returns, therefore, losses from individual subsidiaries of the Group may not be used to offset other subsidiaries’

earnings within the Group. Valuation allowance is considered on each individual subsidiary basis. Valuation allowance of RMB

The impact of an uncertain

income tax position on the income tax return is recognized at the largest amount that is more-likely-than-not to be sustained upon audit

by the relevant tax authority. An uncertain income tax position will not be recognized if it has less than a

The Group has concluded that there are no significant uncertain tax positions requiring recognition in financial statements for the year ended December 31, 2023 and six months ended June 30, 2024. The Group did not incur any significant interest and penalties related to potential underpaid income tax expenses and also does not anticipate any significant increases or decreases in unrecognized tax benefits in the next 12 months. The Group has no material unrecognized tax benefits which would favorably affect the effective income tax rate in future years.

According to the PRC Tax

Administration and Collection Law, the tax authority may require the taxpayer or the withholding agent to make delinquent tax payment

within three years if the underpayment of taxes is resulted from the tax authority’s act or error. No late payment surcharge

will be assessed under such circumstances. The statute of limitation will be three years if the underpayment of taxes is due to the

computational errors made by the taxpayer or the withholding agent. Late payment surcharge will be assessed in such case. The statute

of limitation will be extended to five years under special circumstances which are not clearly defined (but an underpayment of tax

liability exceeding RMB

Therefore, the Group is subject to examination by the PRC tax authorities based on the above.

| For the six months ended June 30, 2023 | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Loss before provision for income taxes and loss from equity method investment | ( | ) | ( | ) | ||||

| Income tax expense computed at an applicable tax rate of | ( | ) | ( | ) | ||||

| Non-deductible expenses related to share-based compensation | ||||||||

| Non-taxable gain related to disposal gain on subsidiaries | ||||||||

| Effect of other non-deductible items | ||||||||

| Effect of preferential tax rate | ( | ) | ||||||

| Effect of income tax rate difference in other jurisdictions | ( | ) | ( | ) | ||||

| Prior year true up | ( | ) | ||||||

| Change in valuation allowance | ||||||||

| Total | ||||||||

F-27

New EIT Law includes a provision

specifying that legal entities organized outside of the PRC will be considered residents for Chinese Income tax purposes if the place

of effective management or control is within the PRC. The implementation rules to the New EIT Law provide that non-resident legal

entities will be considered PRC residents if substantial and overall management and control over the manufacturing and business operations,

personnel, accounting, properties, etc. occurs within the PRC. Despite the present uncertainties resulting from the limited PRC tax

guidance on the issue, the Group does not believe that the legal entities organized outside of the PRC within the Group should be treated

as residents for EIT law purposes. If the PRC tax authorities subsequently determine that the Company and its subsidiaries registered

outside the PRC should be deemed a resident enterprise, the Company and its subsidiaries registered outside the PRC will be subject to

the PRC income tax at a rate of

| 12. | CONVERTIBLE BOND AND DETACHABLE WARRANTS |

The following paragraphs are presented on a retroactive basis to reflect the Company’s share consolidation on April 21, 2022 and November 29, 2023.

On January 26, 2022, the

Company entered into and closed a private placement pursuant to a securities purchase agreement (the “Securities Purchase Agreement”)

with JAK Opportunities LLC (the “Purchaser”) for the offering of a $

On March 1, 2022, the Company

and the Purchaser entered amendment agreements to the Securities Purchase Agreement, Bond, and JAK Warrants to set a floor price of $

On August 29, 2022, the Company

and the Purchaser entered amendment agreements to the Securities Purchase Agreement, Bond, and JAK Warrants to change the floor price

to $

On October 25, 2022, the

Company and the Purchaser entered amendment agreements to the Securities Purchase Agreement, Bond, and JAK Warrants to change the floor

price to $

On January 24, 2023, the

Company and the Purchaser entered amendment agreements to the Securities Purchase Agreement, Bond, and JAK Warrants to change the floor

price to $

F-28

On June 7, 2023, the Company

and the Purchaser entered amendment agreements to the Securities Purchase Agreement, Bond, and JAK Warrants to change the floor price

to $

On January 30, 2024, the

Company and the Purchaser entered amendment agreement to the Warrants to amend and restate the Termination Date for purposes of the Series

B Warrant to December 31, 2024 for the Ordinary Shares issuable upon exercise of the Series B Warrant that are registered under the registration

statement on Form F-3 of Ucommune International Ltd (File No. 333-257664) (the “F-3 Registration Statement”), and to 12 months

following the effectiveness of a registration statement to be filed under the Securities Act registering the remaining unregistered Ordinary

Shares issuable upon exercise of the Series B Warrant for such remaining Ordinary Shares. With respect to the Ordinary Shares issuable

upon exercise of each of the Warrants that are registered under the F-3 Registration Statement, the Floor Price shall be amended and restated

to $

From October 2022 to July

2023, the Company issued

On March 12, 2024, the Purchaser

exercised

As of June 30, 2024, there

are outstanding JAK Warrants to purchase an aggregate of

No fractional shares will be issued upon exercise of the new warrant. No new warrants will be exercisable for cash unless the Company has an effective and current registration statement covering the shares of common stock issuable upon exercise of the new warrants and a current prospectus relating to such shares of common stock.

The JAK Warrants are classified

as a liability. The Company uses the binomial lattice model to value JAK Warrants and the fair value allocated to the JAK Warrants at

the date of issuance was RMB

| 13. | SHARE-BASED COMPENSATION |

The following paragraphs are presented on a retroactive basis to reflect the Company’s share consolidation on April 21, 2022 and November 29, 2023.

| a. | Incentive Plan |

| 2019 Plan |

On September 19, 2019, September

1, 2020 and October 13, 2020, Ucommune Group granted

For type 1,

F-29

For type 2,

For type 3,

For type 4,

On September 1,2020,

The vesting schedule of the award options for certain employees and non-employees has been changed from “

2020 Plan

In connection with the SPAC

Transaction, the Company adopted the 2020 Plan on November 17, 2020 (the “Replacement Date”), which is also the effective

date of the SAPC Transaction to assume and replace the 2019 Plan. The Company rolled over options granted under the 2019 Plan with nearly

the same terms. One option granted under the 2019 Plan was assumed and replaced by

| For the years ended December 31, | For the six months ended June 30, | |||||||

| 2023 | 2024 | |||||||

| RMB | RMB | |||||||

| Risk-free interest rate | % | % | ||||||

| Volatility | % | % | ||||||

| Dividend yield | ||||||||

| Life of options (in years) | ||||||||

| Fair value of underlying ordinary shares* | ||||||||

| * |

F-30

| (1) | Risk-free interest rate |

Risk-free interest rate was estimated based on the US Treasury Bond yield as at the valuation date with a maturity period close to the expected term of the options.

| (2) | Volatility |

The volatility of the underlying ordinary shares during the lives of the options was estimated based on the historical weighted volatility of the ordinary shares of comparable listed companies including the Company itself over a period comparable to the expected term of the options.

| (3) | Dividend yield |

The dividend yield was estimated by the Group based on its expected dividend policy over the expected term of the options.

| (4) | Life of options |

Life of options is extracted from option agreements.

Prior to the consummation of the SPAC Transaction, the estimated fair value of the ordinary shares underlying the options as of the valuation date was determined based on a contemporaneous valuation. When estimating the fair value of the ordinary shares on the valuation dates, management has considered a number of factors, including the result of a third party appraisal of the Company, while taking into account standard valuation methods and the achievement of certain events. The fair value of the ordinary shares in connection with the option grants on the valuation date was determined with the assistance of an independent third-party appraiser. The fair values of the underlying ordinary shares on each date of the grant after November 17, 2020, were the closing prices of the Company’s ordinary shares traded in the stock exchange.

| Number of options | Weighted average exercise price USD | Weighted average grant date fair value RMB | Weighted average remaining contractual term (years) | Aggregate intrinsic value | ||||||||||||||||

| Options outstanding at December 31, 2022 | ||||||||||||||||||||

| Granted | ||||||||||||||||||||

| Exercised | ( | ) | ||||||||||||||||||

| Forfeited | ( | ) | ||||||||||||||||||

| Options outstanding at December 31, 2023 | ||||||||||||||||||||

| Granted | ||||||||||||||||||||

| Exercised | ( | ) | ||||||||||||||||||

| Forfeited | ( | ) | ||||||||||||||||||

| Options outstanding at June 30, 2024 | ||||||||||||||||||||

| Options vested and expected to vest as of June 30, 2024 | ||||||||||||||||||||

| Options exercisable as of June 30, 2024 | ||||||||||||||||||||

| * | The number of options, exercise price and grant date fair value are presented on a retroactive basis to reflect the Company’s share consolidation on November 29, 2023, to effect a share consolidation of |

F-31

The aggregate intrinsic value

was calculated as the difference between the exercise price of the underlying awards and the closing stock price of $

For

the years | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Weighted average grant date fair value of option per share | ||||||||

| Aggregate grant date fair value of options* | ||||||||

| * |

As of June 30, 2024, there was no unrecognized compensation cost related to unvested share options.

| For the six months ended June 30, | ||||||||

| 2023 | 2024 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Cost of revenue | ( | ) | ||||||

| Selling and marketing | ||||||||

| General and administrative | ||||||||

| Total share-based compensation expense | ||||||||

| b. | Earn-out compensation from SPAC Transaction |

In connection with SPAC Transaction,

The Company accounted for the Earnout Shares as share-based compensation under ASC 718. The Company determined the fair value of the earn-out shares using binomial model, which includes significant unobservable inputs that are classified as level 3 in the fair value hierarchy.

No share-based compensation expense of earn-out shares was recorded during the year ended December 31, 2023 and six months ended June 30, 2024.

F-32

| 14. | NET LOSS PER SHARE |

| For the six months ended June 30, 2023 | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Numerator: | ||||||||

| Net loss attributable to Ucommune International Ltd’s shareholders | ( | ) | ( | ) | ||||

| Denominator: | ||||||||

| ( | ) | ( | ) | |||||

| * |

| ** |

For the six months ended

June 30, 2023 and 2024, the Group has and ordinary shares issuable upon the conversion of convertible bonds,

| 15. | RELATED PARTIES BALANCES AND TRANSACTIONS |

The Group had the following related parities:

| a. | Executive Officers and companies controlled by executive officers |

| b. | Equity method investees |

| c. | Companies controlled by the same controlling shareholders. |

| d. | The

|

| e. | The wholly owned subsidiary of d. |

| I. | Balances: |

F-33

| Relationship | Notes | As of December 31, 2023 | As of June 30, 2024 | |||||||||

| RMB | RMB | |||||||||||

| (Unaudited) | ||||||||||||

| Amounts due from related parties: | ||||||||||||

| Guangdong Advertising Co., Ltd. | (d) | (i) | ||||||||||

| Guangdong Marketing Advertising Group | (e) | (i) | ||||||||||

| Youxiang Group | (c) | (ii) | ||||||||||

| Others | (iii) | |||||||||||

| Relationship | Notes | As of December 31, 2023 | As of June 30, 2024 | |||||||||

| RMB | RMB | |||||||||||

| (Unaudited) | ||||||||||||

| Amounts due to related parties: | ||||||||||||

| Youxiang Group | (c) | (iv) | ||||||||||

| Guangdong Advertising Co., Ltd. | (d) | (v) | ||||||||||

| Others | (vi) | |||||||||||

Notes:

| (i) |

| (ii) |

| (iii) |

| (iv) |

| (v) |

| (vi) |

| II. | Transactions: |

Lease expenses

| Six months Ended June 30, 2023 | Six months Ended June 30, 2024 | |||||||||||

| Relationship | Notes | RMB | RMB | |||||||||

| (Unaudited) | (Unaudited) | |||||||||||

| Youxiang Group | (c) | (i) | — | |||||||||

| Guangdong Advertising Co., Ltd. | (d) | (i) | ||||||||||

F-34

Revenues

| Six months Ended June 30, 2023 | Six months Ended June 30, 2024 | |||||||||||

| Relationship | Notes | RMB | RMB | |||||||||

| (Unaudited) | (Unaudited) | |||||||||||

| Youxiang Group | (c) | (ii) | ||||||||||

| Guangdong Advertising Co., Ltd. | (d) | (iii) | ||||||||||

Property management expense

| Six months Ended June 30, 2023 | Six months Ended June 30, 2024 | |||||||||||

| Relationship | Notes | RMB | RMB | |||||||||

| (Unaudited) | (Unaudited) | |||||||||||

| Youxiang Group | (c) | (iv) | ||||||||||

Purchase of advertisement distribution resources

| Six months Ended June 30, 2023 | Six months Ended June 30, 2024 | |||||||||||

| Relationship | Notes | RMB | RMB | |||||||||

| (Unaudited) | (Unaudited) | |||||||||||

| Guangdong Advertising Co., Ltd. | (d) | (v) | ||||||||||

| Guangdong Advertising Marketing Group | (e) | (v) | ||||||||||

Notes:

| (i) |

| (ii) |

| (iii) |

| (iv) |

| (v) |

| 16. | COMMITMENTS AND CONTINGENCIES |

Capital commitment

As of June 30, 2024, the Group had no significant outstanding capital commitments.

Contingencies

In December 2019, Beijing

Huasheng Venture Real Estate Development Co., Ltd (“Beijing Huasheng”) entered into a lease agreement with Ucommune Venture.

Pursuant to the lease agreement, the Company agreed to lease the property of Beijing Huasheng in Beijing for a term of

F-35

On October 19, 2023, Beijing

Huasheng, together with Beijing Aikang Medical Investment Holding Group Co., Ltd. and Shanghai Tibai Medical Technology Co., Ltd. initialed

another arbitration before Beijing Arbitration Commission, requesting the Company to compensate for the loss of their investments in the

amount of US$

Except as described above, the Group is not a party to any material legal or administrative proceedings. From time to time, the Group is involved in various other legal and regulatory proceedings arising in the normal course of business. While the Group cannot predict the occurrence or outcome of these proceedings with certainty, it does not believe that an adverse result in any pending legal or regulatory proceeding, individually or in the aggregate, would be material to the Group’s consolidated financial condition or cash flows.

| 17. | SEGMENT INFORMATION |

Operating segments are defined as components of an enterprise engaging in business activities for which separate financial information is available that is regularly evaluated by the Group’s chief operating decision makers (“CODM”) in deciding how to allocate resources and assess performance.

The Group’s CODM has

been identified as the CEO. For the six months ended June 30, 2023 and 2024, there are

The Group primarily operates

in the PRC and substantially all of the Group’s long-lived assets are located in the PRC. The Group’s CODM evaluates

performance based on each operating segment’s revenue and costs of revenue (excluding impairment loss).

| For the six months ended June 30, 2023 | For the six months ended June 30, 2024 | |||||||

| RMB | RMB | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Revenue: | ||||||||

| Workspace membership | ||||||||

| Marketing and branding services | ||||||||

| Other services | ||||||||

| Total revenue | ||||||||

| Cost of revenue (excluding impairment loss) | ||||||||

| Workspace membership | ( | ) | ( | ) | ||||

| Marketing and branding services | ( | ) | ( | ) | ||||

| Other services | ( | ) | ( | ) | ||||

| Total cost of revenue (excluding impairment loss) | ( | ) | ( | ) | ||||

The Group’s CODM does not review the financial position by operating segment, thus total assets by operating segment is not presented.

| 18. | SUBSEQUENT EVENTS |

On September 20, 2024, Ucommune (Beijing) Technology Co., Ltd. (“Ucommune Technology”), a wholly foreign-owned enterprise of the Company, issued a notice (“Notice of Termination”) to terminate the Ucommune Venture VIE Agreements (as defined below) to Ucommune (Beijing) Venture Investment Co., Ltd. (“Ucommune Venture”), a variable interest entity of the Company, and the existing shareholders of Ucommune Venture. As a result, the series of contractual arrangements entered into by and among Ucommune Technology, Ucommune Venture and/or its shareholders (the “Ucommune Venture VIE Agreements”), including exclusive business cooperation agreement, equity pledge agreement, exclusive option agreement, shareholders’ voting rights proxy agreement and spousal consent letter, will be terminated in accordance with the terms therein following 30 calendar days after the delivery date of the Notice of Termination, by which time Ucommune Venture and its subsidiaries will be deconsolidated and their financial results will no longer be included in the Company’s consolidated financial statements. The Company has also carried out a series of restructuring transactions where the Company’s workspace membership business for mid- to large-sized enterprise members and marketing and branding business will continue to be operated by the Company, with the financial results being included in the Company’s consolidated financial statements; and certain non-core businesses of the Company will be disposed of in connection with the Notice of Termination.

The Company has evaluated the impact of events that have occurred subsequent to June 30, 2024, through the issuance date of the consolidated financial statements, other than the subsequent event described above, the Company did not identify any subsequent events that would have required adjustment or disclosure on the consolidated financial statements.

F-36

Exhibit 99.2

Conventions Which Apply to this Discussion

Except where the context otherwise requires and for purposes of the discussion in this Exhibit 99.2, or this discussion, only:

| ● | “Beijing Melo” refers to Beijing Melo Technology Co., Ltd.; |

| ● | “Beijing U Bazaar” refers to Beijing Ubazaar Technology Co., Ltd.; |

| ● | “Business Combination” refers to (1) reincorporation of Orisun Acquisition Corp in the Cayman Islands by merging with and into Ucommune; and (2) merger of Everstone International Ltd, a Cayman Islands exempted company, with and into Ucommune Group Holdings Limited, or Ucommune Group Holdings, resulting in Ucommune Group Holdings being a wholly owned subsidiary of the Parent; |