February 2, 2024

VIA EDGAR

United States Securities and Exchange Commission

Division of Corporation Finance

Office of Industrial Applications and Services

100 F Street, N.E.

Washington, D.C. 20549

Attention: Ken Schuler, Craig Arakawa, Jeanne Baker and Terence O’Brien

|

Re:

|

Tronox Holdings plc

Form 10-K for the year ended December 31, 2022

Filed on February 22, 2023

File No. 001-35573

|

Dear Mr. Schuler, Mr. Arakawa, Ms. Baker and Mr. O’Brien,

On behalf of Tronox Holdings plc (“Tronox,” the “Company,” “we,” “us” and, with correlative meaning, “our”), the

following responses are provided to the comments submitted to Tronox by the staff of the Securities and Exchange Commission (the “Staff”) in a letter dated December 22, 2023 (the “Letter”) relating to Tronox’s Annual Report on Form 10-K for the year ended December 31, 2022 (the “2022 Form 10‑K”),

in compliance with the extension period granted by the Staff in a telephone conference on December 26, 2023. Terms not defined herein shall have the meaning set forth in the 2022 Form 10-K. We have restated below in italics the comments from the

Letter and have supplied our response to the comment immediately thereafter.

The Company proposes to comply with these comments for the first time in its Annual Report on Form 10-K for the fiscal year ended December 31, 2023 (the “2023 Form 10‑K”). The Company respectfully submits that, given the proximity to the filing of the 2023 Form 10-K, this

approach would be more appropriate to best aid investor understanding and reduce the risk of investor confusion with multiple filings, as the Staff reviews and evaluates the proposed illustrative disclosures contained herein. The Company does not believe this approach would be prejudicial to investors, as the Company believes that all material information relating to these properties is already contained in the 2022 Form 10-K and previously

filed technical report summaries (“TRSs”), taken as a whole, and any

additional information provided with respect to prior periods will be available to investors in the 2023 Form 10-K.

|

Tronox Holdings plc

263 Tresser Blvd., Suite 1100

Stamford, CT 06901 USA

T +1 203 705 3800

www.tronox.com

|

|

Securities and Exchange Commission

Division of Corporation Finance

Page 2

|

To that end, the Company has endeavored to provide the Staff with proposed preliminary disclosure in the appendices hereto reflecting certain information and data of the Company as of and for the fiscal year ended

December 31, 2023, which information and data are not yet final as of the date hereof and are thus set forth herein as placeholders for illustrative purposes. Appendix A provides the

proposed structure for the summary property disclosure and individual property disclosure for the 2023 Form 10-K. In addition, as further discussed herein, the Company respectfully advises the Staff that there have been no material changes in the

mineral reserves or mineral resources for the properties described in each of the TRSs incorporated by reference as Exhibit 96.1, 96.2, 96.3 and 96.4 to the 2022 Form 10-K since December 31, 2021, the effective date of each such TRS. The Company has therefore provided the Staff with certain supplemental information as of and for the fiscal year ended on such effective date, which it proposes to include in

amendments to the respective TRSs that will be filed as exhibits to the 2023 Form 10-K in response to the Staff’s comments. Appendices B, C, D and E (collectively with Appendix A, the “Appendices”) provide such supplemental disclosure for such TRS amendments to be filed

as Exhibits 96.1, 96.2, 96.3 and 96.4 to the 2023 Form 10-K, respectively.

Form 10-K

Mining Operations, page 27

1. The summary disclosures should encompass all your properties, including both material and non-material properties, and should appear in advance of and

incremental to, the individual property disclosures. The requirements for individual property disclosures are more extensive and detailed in comparison and are applicable for material properties, as determined pursuant to Item 1301 of Regulation

S-K. For example, the summary disclosures should describe the locations of each operating, development, and exploration property to comply with Item 1303(b)(2)(ii)(A); while the individual property disclosures should

include comparable details along with a map for each property, showing its particular location, that is accurate to within one mile, using an easily recognizable coordinate system, to comply with Item 1304(b)(1)(i). Please revise your filing to include and differentiate between the summary and individual property disclosures to comply with the aforementioned guidance.

Response:

The Company respectfully acknowledges the Staff’s interpretation of Items 1303 and 1304 of Regulation S-K and

will include in Part I, Item 2 “Properties” of the 2023 Form 10-K finalized summary and individual property disclosure that is substantially in the form of the illustrative disclosure set forth in Appendix A.

The Company respectfully submits to the Staff in an effort to place in context the following responses that it had considered these matters in preparing the 2022 Form 10-K and,

based on its initial interpretation of Item 601(b)(96) and subpart 1300 of Regulation S-K, the Company provided the information required by such Item and subpart in the 2022 Form 10‑K and TRSs, considered

together, with the exception of certain information that it did not believe to be material to investors given that the Company is a vertically integrated manufacturer of TiO2 pigment. With respect to the material properties, for example,

certain portions of the information required under Item 1304 of Regulation S-K, such as the requisite descriptions of the properties, including maps accurate to within one mile, existing infrastructure, the

Company’s ownership interest in the property and the history of the property, were provided only in the respective TRSs for each such property. Nonetheless, the Company recognizes that subpart 1300 of Regulation S-K applies to vertically

integrated companies with mining operations, and the Company will therefore include the additional information set forth in Appendix A in the 2023 Form 10-K.

|

Securities and Exchange Commission

Division of Corporation Finance

Page 3

|

The Company further advises the Staff that it has assessed the materiality of its mining operations as required by Item 1301 of Regulation S-K, using the principles set forth in Release No. 34-84509

(Oct. 31, 2018). Based on this analysis, the Company has determined that the following of its mining operations are material: Cooljarloo, Atlas-Campaspe, Namakwa Sands and KZN Sands. The Company has also determined that the following of its mining

operations are not material: Dongara, Port Durnford, Wonnerup, Ginkgo-Crayfish Dredge and Kara/Cylinder.

Mineral Sands – South Africa and Australia, page 30

2. Please revise your filing to report each individual property’s production by product such as heavy metals, ilmenite, rutile, leucoxene, and zircon, as required

by Item 1303(b)(2)(i) of Regulation S-K.

Response:

The Company respectfully informs the Staff that, based on its interpretation of Item 1303(b)(2)(i) of Regulation S‑K, which requires to “aggregate annual production for the properties,” the

Company provided its aggregate mineral production for each of the three years ended December 31, 2022 on pages 30 and 31 the 2022 Form 10-K.1 Nonetheless, the Company respectfully acknowledges the

Staff’s comment and provides the illustrative disclosure showing the Company’s aggregate annual production by property as set forth in Appendix A on page A-2. The Company will comply with this comment by including finalized disclosure in

Part I, Item 2 “Properties” of the 2023 Form 10-K.

Heavy Metal Reserves, page 32

3. Please include the commodity price used, metallurgical recovery, and the cutoff grade with your resource and reserve disclosures as required by Item 1303(b)(3)

of Regulation S-K.

1 This interpretation is consistent with the Release No. 34-84509 (Oct. 31, 2018), which states that “in a change from the proposed rules, which required the disclosure of the total production from

each of the registrant’s top 20 properties by asset value for the three most recently completed fiscal years, the final rules require that the overview must include annual production on an aggregated basis for the registrant’s mining properties

during each of the three most recently completed fiscal years” (footnotes omitted).

|

Securities and Exchange Commission

Division of Corporation Finance

Page 4

|

Response:

The Company respectfully acknowledges the Staff’s comment and provides the illustrative disclosure setting forth the commodity price used, saleable product yield (recovery) and the cutoff grade with our reserves and

resources disclosures, as set forth in Appendix A on pages A-3 and A-4. The Company will include finalized disclosure in the 2023 Form 10-K. The Company respectfully informs the Staff that Tronox uses the term “saleable product yield (recovery)” to refer to the conversion of contained, in-situ mineral to saleable products, which is equivalent to the term “metallurgical or processing recoveries” used in subpart 1300 of

Regulation S-K.

4. Please state whether your qualified persons (QP’s) are employees of your company and provide the additional information required by Item 1302(b)(5) of

Regulation S-K.

The Company confirms that each of the QPs who prepared the TRSs incorporated by reference as Exhibits 96.1, 96.2, 96.3 and 96.4 to the 2022 Form 10-K is an employee of an

indirect wholly owned subsidiary of the Company. This information will be included in Part I, Item 2 “Properties” of the 2023 Form 10-K, as indicated in Appendix A on page A-1.

Tronox Mineral Sands – 2022 Resources, page 34

5. Please clearly state your mineral resources are exclusive of reserves as required by Item 1303(b)(3) of Regulation S-K.

Response:

The Company confirms that its mineral resources are exclusive of reserves. This information will be included in Part I, Item 2 “Properties” of the 2023 Form 10-K, as indicated in Appendix A beginning on page

A-4.

6. Please modify your filing and provide a more detailed reconciliation of your resources/reserves as reported this year to last year, as required by Item 1303(e)

of Regulation S‑K.

Response:

The Company respectfully acknowledges the Staff’s comment and respectfully submits that the last columns of the tables on page 33 and 34 of the 2022 Form 10-K indicate the changes in our reserves/resources compared to

2021. As indicated in these tables there has been no material variation in the Company’s reported reserves and resources, and the changes reported are predominantly due to depletion, as indicated in the footnotes to these tables. For these reasons,

the Company believes that form of presentation satisfies the requirements of Item 1304(e). Nonetheless, the Company acknowledges the Staff’s interpretation of Item 1304, and provides an illustrative more detailed reconciliation of resources and

reserves from 2023 to 2022 as set forth in Appendix A for all of our mining operations beginning on page A-3 and for each of our material mining operations beginning on pages A-7, A-13, A-16 and A-19. The Company will comply with this comment in Part

I, Item 2 “Properties” of the 2023 Form 10-K.

|

Securities and Exchange Commission

Division of Corporation Finance

Page 5

|

7. Please modify your filing here and elsewhere to state the book value of your material properties as required by Item 1304(b)(2)(iii) of Regulation S-K.

Response:

The Company acknowledges the Staff’s comment and provides the illustrative disclosure regarding the book values of each our material properties and mining operations, inclusive of

plant, property and equipment, as set forth in Appendix A on pages A-5, A-10, A-15 and A-18. The Company will comply with this comment in the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4

Property Description, page E-1

Property Description, page E-1

8. Please modify your exhibits and locate your property within one-mile using an easily recognizable coordinate system as required by

Item 601(b)(96)(iii)(B)(3)(i) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment. Please refer to the maps on page 2 of each of Exhibit 96.1, 96.2, 96.3 and 96.4 of the 2022 Form 10-K, which the

Company respectfully submits to the Staff are in compliance with requirements to locate each property within one-mile using an easily recognizable coordinate system pursuant to Item 601(b)(96)(iii)(B)(3)(i) of Regulation S-K. In response to the

Staff’s comment, the Company additionally provides the coordinates of each property as shown in Appendix A on pages A-6, A-10, A-15 and A-18. The Company will amend the TRSs to include this information, and will file such amendments as Exhibits to

the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4

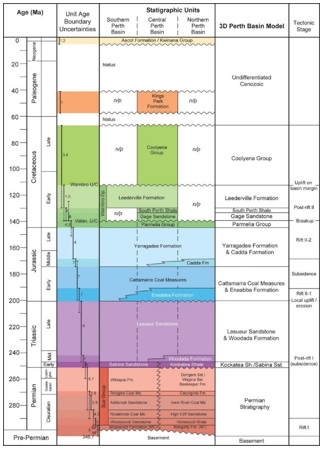

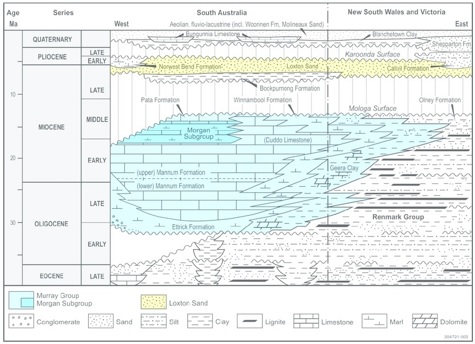

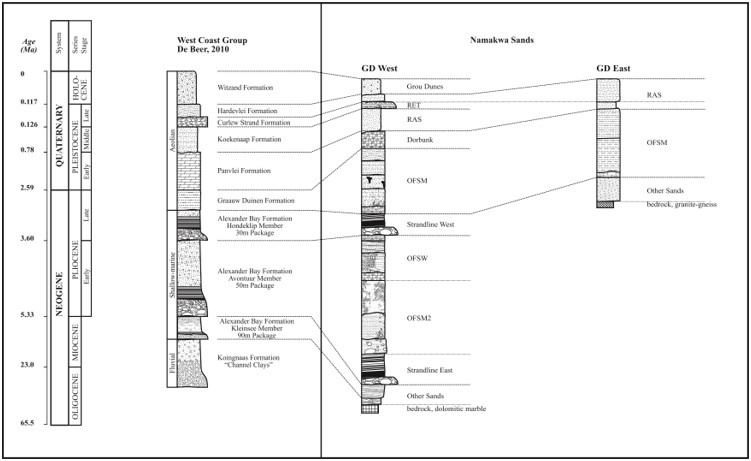

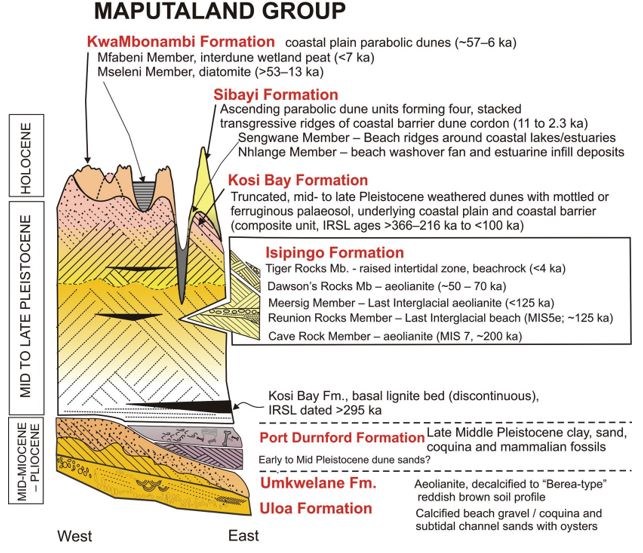

Geological Setting, Mineralisation and Deposit, page E-2

Geological Setting, Mineralisation and Deposit, page E-2

9. Please modify your filings and ensure you have provided at least one stratigraphic column and one cross-section of the local geology as required by Item

601(b)(96)(iii)(B)(6)(iii) of Regulation S-K.

Response:

The Company respectfully refers the Staff to the cross-sections of the local geology on page 5 of Exhibit 96.1, page 4 of Exhibit 96.2, page 6 of Exhibit 96.3 and page 9 of Exhibit 96.4 of the 2022 Form 10-K, which the Company respectfully submits to the Staff are in compliance with requirements of Item 601(b)(96)(iii)(B)(6)(iii) of Regulation S-K. In response to the Staff’s comment, the Company provides the

stratigraphic columns as shown in the Appendices on pages B-1, C-1, D-1 and E-1. The Company will amend the TRSs to include this information, and will file such amendments as Exhibits to the 2023 Form 10-K.

|

Securities and Exchange Commission

Division of Corporation Finance

Page 6

|

Exhibits 96.1, 96.2, 96.3, and 96.4

Sample Preparation, Analyses and Security, page E-3

Sample Preparation, Analyses and Security, page E-3

10. Please modify your filing and provide the opinion of the QP regarding the adequacy of the sample preparation, security, and analytical procedures as required

by Item 601(b)(96)(iii)(B)(8)(iv) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment. Each QP has confirmed to the Company that the general opinion reflected on Section 22 – Interpretation and Conclusions of each TRS (on page 19 of Exhibit 96.1,

page 21 of Exhibit 96.2, page 24 of Exhibit 96.3 and page 24 of Exhibit 96.4 of the 2022 Form 10-K) reflects such QP’s view with respect to the adequacy of the sample preparation, security and analytical

procedures. Nonetheless, the Company respectfully acknowledges the Staff’s interpretation and the QPs will revise their TRSs to include a statement to the effect that it is the QPs view that the sample preparation, security and analytical

procedures are adequate.

Exhibits 96.1, 96.2, 96.3, and 96.4

Mineral Processing and Metallurgical Testing, page E-4

Mineral Processing and Metallurgical Testing, page E-4

11. We reviewed the Mineral Processing and Metallurgical Testing section of your technical report summary. Please modify your filing to disclose your estimated

metallurgical recoveries with the QP’s opinion on the adequacy of the metallurgical data as required by Item 601(b)(96)(iii)(B)(10)(v) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-1, C-1, D-1 and E-2. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4

Mineral Resource Estimates, page E-5

Mineral Resource Estimates, page E-5

12. Please modify your filing and disclose the cutoff grade for your resource estimates with all the parameters used to prepare this calculation. This would

include your commodity price, operating costs, and metallurgical recovery. See Item 601(b)(96)(iii)(B)(11)(iii) of Regulation S‑K.

|

Securities and Exchange Commission

Division of Corporation Finance

Page 7

|

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-2, C-1, D-2 and E-2. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

13. Please modify your filing and revise your resource and reserve summaries in your exhibits to clarify whether your cutoff grades are a breakeven and

internal/marginal cutoff grade.

Response:

The Company respectfully acknowledges the Staff’s comment and provides a discussion of the applicable cutoff grades used by the Company in the Appendices on pages B-2, C-1, D-2 and E-2. The Company will amend the TRSs to

include this information, and will file such amendments as Exhibits to the 2023 Form 10-K.

14. Please modify your filing and disclose the QP’s opinion on whether all issues related to resource technical and/or economic factors influencing economic

extraction can be resolved with further work. See Item 601(b)(96)(iii)(B)(11)(vii) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment. Each QP has confirmed to the Company that the general opinion reflected on Section 22 – Interpretation and Conclusions of each TRS (on page 19 of Exhibit 96.1,

page 21 of Exhibit 96.2, page 24 of Exhibit 96.3 and page 24 of Exhibit 96.4 of the 2022 Form 10-K) reflects such QP’s view that all issues related to resource technical and

economic factors influencing economic extraction can be resolved with further work. Nonetheless, the Company respectfully acknowledges the Staff’s interpretation and provides the QP’s opinion as shown in the Appendices on pages B-2, C-2, D-2 and E-3.

The Company will amend the TRSs to include this information, and will file such amendments as Exhibits to the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4

Mineral Reserve Estimates, page E-6

Mineral Reserve Estimates, page E-6

15. Please modify your filing and disclose the cutoff grade for your reserve estimates along with all the parameters used to prepare this calculation. See Item

601(b)(96)(iii)(B)(12)(iii) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-2, C-1, D-2 and E-2. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

|

Securities and Exchange Commission

Division of Corporation Finance

Page 8

|

16. We note you did not state a commodity sales price for your resource and reserve estimates. Please state the price used to determine your resources/reserves

and disclose, with particularity, the reasons this price was selected and any assumptions underlying this selection. See Item 601(b)(96)(iii)(B)(12)(iii) of Regulation S-K.

The Company respectfully acknowledges the Staff’s comment and provides the commodity sales prices as shown in the Appendices on pages B-2, C-2, D-3 and E‑3. The Company will amend the TRSs to include this information,

and will file such amendments as Exhibits to the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4 A

Mining Methods, page E-7

Mining Methods, page E-7

17. Please provide annual numerical values for your life of mine production schedule. This would include annual processed ore with associated grades for the life

of mine. See Item 601(b)(96)(iii)(B)(13) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-3, C-3, D-3 and E-3. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4 A

Processing and Recovery Methods, page E-8

Processing and Recovery Methods, page E-8

18. We note your property has been in operation for several years. Please disclose your annual plant throughput and recoveries over

the last 3 years. Item 601(b)(96)(iii)(B)(14)(ii) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment. Please refer to the respective Section 14 – Processing and Recovery Methods of each TRS, on page 15 of Exhibit 96.1, page 14 of Exhibit 96.2, page 17 of Exhibit

96.3 and page 15 of Exhibit 96.4 of the 2022 Form 10-K where plant throughput and saleable product yield (recovery) are described.

|

Securities and Exchange Commission

Division of Corporation Finance

Page 9

|

The Company respectfully advises the Staff that in its view Item 601(b)(96)(iii)(B)(14)(ii) of Regulation S-K requires only a description of the current or proposed mineral processing methods and the reasons for

selecting these methods as the most suitable for extracting the valuable products from the mineralization under consideration, which must include plant throughput and design, equipment characteristics and specifications. The Company respectfully

advises the Staff that it does not believe Item 601(b)(96)(iii)(B)(14)(ii) of Regulation S-K requires annual throughput and recovery statistics over the last three years. Nonetheless, the Company acknowledges the Staff’s interpretation and provides

the disclosure as shown in the Appendices on pages B-3, C-3, D-3 and E-3. The Company will amend the TRSs to include this information, and will file such amendments as Exhibits to the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4 A

Market Studies, page E-9

Market Studies, page E-9

19. Please provide the relevant market price projections for your life of mine and include the 5-year historic prices with your forecast pricing as required by

Item 601(b)(96)(iii)(B)(16) of Regulation S-K.

Response:

The Company respectfully advises the Staff that it did not provide this information based on its initial interpretation of Item 601(b)(96)(iii)(B)(16) of Regulation S-K, which does not require “5-year historic prices.”

Nonetheless the Company respectfully acknowledges the Staff’s interpretation and provides the disclosure as shown in the Appendices on pages B-2, C-2, D-3 and E-3. The Company will amend the TRSs to include this information, and will file such

amendments as Exhibits to the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4 A

Environmental studies, permitting and plans, negotiations, or agreements with local individuals or groups, page E-10

Environmental studies, permitting and plans, negotiations, or agreements with local individuals or groups, page E-10

20. We reviewed the Environmental Studies, Permitting, And Plans, Negotiations, Or Agreements with Local Individuals or Groups section of your technical report

summary. Please modify your filing and include the QP’s opinion as to the adequacy of current plans for environmental compliance, permitting, and addressing issues with local individuals or groups required by Item 601(b)(96)(iii)(B)(17)(vi) of

Regulation S-K.

|

Securities and Exchange Commission

Division of Corporation Finance

Page 10

|

Response:

The Company respectfully acknowledges the Staff’s comment. Each QP has confirmed to the Company that the general opinion reflected on Section 22 – Interpretation and Conclusions of each TRS (on page 19 of Exhibit 96.1,

page 21 of Exhibit 96.2, page 24 of Exhibit 96.3 and page 24 of Exhibit 96.4 of the 2022 Form 10-K) reflects such QP’s view with respect to the adequacy of current plans for

environmental compliance, permitting and addressing issues with local individuals or groups. Nonetheless, the Company respectfully acknowledges the Staff’s interpretation and provides the QP’s opinion as shown in the Appendices on pages B-3, C-3,

D-4 and E-4. The Company will amend the TRSs to include this information, and will file such amendments as Exhibits to the 2023 Form 10-K.

Exhibits 96.1, 96.2, 96.3, and 96.4 A

Capital and Operating Cost, page E-11

Capital and Operating Cost, page E-11

21. Please revise to provide a tabulation of all the operating and capital costs for your life of mine used to prepare your economic analysis. See Item

601(b)(96)(iii)(B)(18)(i) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-3, C-3, D-4 and E-4. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

22. Please modify your filing and define the accuracy of your capital and operating costs estimates as required by Item 601(b)(96)(iii)(B)(18)(i) of Regulation

S-K.

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-4, C-3, D-4 and E-4. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

23. Please modify your filings to disclose your closing/reclamation costs as required by Item 601(b)(96)(iii)(B)(18)(i) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-4, C-4, D-4 and E-4. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

|

Securities and Exchange Commission

Division of Corporation Finance

Page 11

|

Exhibits 96.1, 96.2, 96.3, and 96.4 A

Economic Analysis, page E-12

Economic Analysis, page E-12

24. We note you did not disclose an economic analysis for your reserves in this section. Please modify your filing to provide an annual cash flow, summarizing the

results on an after-tax basis. Your financial analysis should disclose your production, prices, revenues, capital, sustaining capital, reclamation, operating costs, royalties, taxes, DD&A, pre- and post-tax cash flows for the life of your

property’s reserves. This information should be clearly related to information developed and disclosed in previous sections, such as reserve quantities, mine/plant recoveries, prices, operating costs, capital expenditures, royalties, taxes, and

other line items necessary to define your after-tax cash flow. See Item 601(b)(96)(iii)(B)(19)(ii) of Regulation S‑K.

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-5, C-4, D-5 and E-5. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

25. Please include a sensitivity analysis and discuss the impact on your cash flow analysis as required by Item 601(b)(96)(iii)(B)(19)(iii) of Regulation S-K.

Response:

The Company respectfully acknowledges the Staff’s comment and provides the disclosure as shown in the Appendices on pages B-5, C-5, D-5 and E-5. The Company will amend the TRSs to include this information, and will file

such amendments as Exhibits to the 2023 Form 10-K.

* * * *

|

Securities and Exchange Commission

Division of Corporation Finance

Page 12

|

If you require additional information, please do not hesitate to contact Jonathan Flood or the undersigned at (203)

705-3800.

|

Very truly yours,

|

|

|

/s/ John Srivisal

|

|

|

John Srivisal

|

|

|

Senior Vice President and Chief Financial Officer

|

|

* * * *

Appendix A

ITEM 2. PROPERTIES

Summary Disclosure Supplements

Figure 1 Showing global site and offices including locations with resources and reserves.2

2 The Company supplementally advises the Staff that our Paraiba, Brazil mining operations were removed from Figure 1 because such operations ceased during 2020 in line with our life of mine plan.

A-1

|

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-2

|

|

TRONOX MINERAL SANDS - 2023 AGGREGATE MINERAL PRODUCTION FOR THE PAST THREE YEARS (metric tons per year)

|

||||||||||||

|

2023

|

2022

|

2021

|

||||||||||

|

Rutile(1)

|

||||||||||||

|

Australia

|

||||||||||||

|

18,850

|

25,519

|

|||||||||||

|

Atlas-Campaspe

|

-

|

-

|

||||||||||

|

South Africa

|

||||||||||||

|

Namakwa Sands

|

31,304

|

28,994

|

||||||||||

|

KZN Sands

|

16,326

|

21,478

|

||||||||||

|

All Other Properties

|

92,644

|

65,603

|

||||||||||

|

Total

|

159,124

|

141,594

|

||||||||||

|

Ilmenite(2)

|

||||||||||||

|

Australia

|

||||||||||||

|

Cooljarloo

|

143,049

|

185,481

|

||||||||||

|

Atlas-Campaspe

|

-

|

-

|

||||||||||

|

South Africa

|

||||||||||||

|

Namakwa Sands

|

567,050

|

408,471

|

||||||||||

|

KZN Sands

|

290,407

|

429,271

|

||||||||||

|

All Other Properties

|

155,593

|

167,758

|

||||||||||

|

Total

|

1,156,099

|

1,190,981

|

||||||||||

|

Zircon(3)

|

||||||||||||

|

Australia

|

||||||||||||

|

Cooljarloo

|

21,694

|

27,490

|

||||||||||

|

Atlas-Campaspe

|

-

|

-

|

||||||||||

|

South Africa

|

||||||||||||

|

Namakwa Sands

|

107,967

|

112,844

|

||||||||||

|

KZN Sands

|

31,839

|

40,368

|

||||||||||

|

All Other Properties

|

38,233

|

39,123

|

||||||||||

|

Total

|

199,733

|

219,825

|

||||||||||

|

HMC(4)

|

||||||||||||

|

Australia

|

||||||||||||

|

Cooljarloo

|

265,982

|

316,942

|

||||||||||

|

Atlas-Campaspe

|

-

|

-

|

||||||||||

|

South Africa

|

||||||||||||

|

Namakwa Sands

|

1,576,618

|

1,663,243

|

||||||||||

|

KZN Sands

|

429,521

|

498,502

|

||||||||||

|

All Other Properties

|

321,902

|

436,146

|

||||||||||

|

Total

|

2,591,023

|

2,914,833

|

||||||||||

(1) includes natural rutile + leucoxene

(2) includes multiple grades of TiO2 grades of ilmenite

(3) includes multiple grades of zircon

(4) HMC = Heavy Mineral Concentrate

The following tables summarize our reserves and resources as well as their contained in-situ total heavy minerals (THM) and heavy mineral (HM) assemblages as of December 31, 2023 based on long-term price

assumptions. The sole purpose of the operational and related financial data presented is to demonstrate the economic feasibility of the mineral reserves for the purpose of reporting in accordance with subpart 1300 of Regulation S-K, and should not be

used for other purposes. The information presented originates from comprehensive techno-economic modelling, which is subject to change as assumptions and inputs are updated, and as a result does not guarantee future operational or financial

performance. Consistent with industry standards, Tronox values its mineral reserves based on the prices at which its titanium and zircon mineral products would sell on freely traded markets, as forecasted by third-party industry consultancies.

The decrease in resources at all operating sites in 2023 as compared to 2022 is primarily attributed to mining depletion. In addition, as of December 31, 2023 the remaining resources for Crayfish, Ginkgo and Wonnerup

were removed from the resources table because they were considered unlikely to ever be economically viable due to their being either too low in grade, too deeply buried, sterilized by previous mining operations or located within environmentally

sensitive locations.

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-3

The decrease in reserves at all operating sites in 2023 as compared to 2022 is primarily attributed to mining depletion. In July 2023, mining ceased at Crayfish due to poor project economics. The remaining Crayfish

material was removed from reserves.

|

Mineral Assemblage (% of THM)

|

||||||||||||||||||||||||

|

2023

|

2022

|

|||||||||||||||||||||||

|

MINE /

DEPOSIT

|

Resource

Category

|

Material

(million

tons)

|

HM%

|

Ilmenite

|

Rutile

and

Leucoxene

|

Zircon

|

Change (+/-)

from 2022

(%)

|

Material

(million tons)

|

HM%

|

Ilmenite

|

Rutile

and Leucoxene

|

Zircon

|

||||||||||||

|

Namakwa Sands Dry Mine – Western Cape RSA(2)

|

||||||||||||||||||||||||

|

Measured

|

104

|

8.0%

|

30.2

|

5.9

|

6.9

|

|||||||||||||||||||

|

Indicated

|

86

|

6.5%

|

28.3

|

5.6

|

6.9

|

|||||||||||||||||||

|

Measured + Indicated

|

191

|

7.3%

|

29.3

|

5.8

|

6.9

|

|||||||||||||||||||

|

Inferred

|

110

|

5.5%

|

35.1

|

8.1

|

6.6

|

|||||||||||||||||||

|

Total

|

300

|

6.7%

|

31.4

|

6.6

|

6.7

|

|||||||||||||||||||

|

KZN Sands Hydraulic Mine – KwaZulu-Natal RSA(3)

|

||||||||||||||||||||||||

|

Measured

|

48

|

4.2%

|

64.3

|

8.1

|

7.7

|

|||||||||||||||||||

|

Indicated

|

1

|

2.0%

|

53.5

|

7.0

|

7.5

|

|||||||||||||||||||

|

Measured + Indicated

|

49

|

4.1%

|

64.1

|

8.1

|

7.6

|

|||||||||||||||||||

|

Inferred

|

56

|

3.4%

|

54.6

|

6.9

|

7.1

|

|||||||||||||||||||

|

Total

|

105

|

3.7%

|

59.1

|

7.4

|

7.3

|

|||||||||||||||||||

|

Cooljarloo – Dredge Mine – Western Australia(4)

|

||||||||||||||||||||||||

|

Measured

|

10

|

1.6%

|

59.3

|

7.7

|

9.8

|

|||||||||||||||||||

|

Indicated

|

282

|

1.5%

|

61.4

|

6.7

|

10.5

|

|||||||||||||||||||

|

Measured + Indicated

|

292

|

1.5%

|

61.3

|

6.8

|

10.4

|

|||||||||||||||||||

|

Inferred

|

12

|

2.9%

|

58.0

|

7.3

|

9.0

|

|||||||||||||||||||

|

Total

|

304

|

1.6%

|

61.1

|

6.8

|

10.4

|

|||||||||||||||||||

|

Dongara Planned Dry Mine – Western Australia(5)

|

||||||||||||||||||||||||

|

Measured

|

109

|

4.1%

|

50.2

|

9.0

|

10.8

|

|||||||||||||||||||

|

Indicated

|

31

|

3.5%

|

53.7

|

9.1

|

12.4

|

|||||||||||||||||||

|

Measured + Indicated

|

140

|

3.9%

|

52.0

|

9.1

|

11.6

|

|||||||||||||||||||

|

Inferred

|

46

|

3.7%

|

56.1

|

8.9

|

9.2

|

|||||||||||||||||||

|

Total

|

186

|

3.9%

|

52.1

|

9.0

|

10.7

|

|||||||||||||||||||

|

Atlas-Campaspe Dry Mine – New South Wales Australia(6)

|

||||||||||||||||||||||||

|

Measured

|

27

|

2.5%

|

58.8

|

10.9

|

11.7

|

|||||||||||||||||||

|

Indicated

|

-

|

-%

|

-

|

-

|

-

|

|||||||||||||||||||

|

Measured + Indicated

|

27

|

2.5%

|

58.8

|

10.9

|

11.7

|

|||||||||||||||||||

|

Inferred

|

83

|

3.1%

|

60.1

|

5.8

|

13.1

|

|||||||||||||||||||

|

Total

|

110

|

3.0%

|

59.8

|

6.9

|

12.8

|

|||||||||||||||||||

|

Port Durnford – KwaZulu-Natal RSA(7)

|

||||||||||||||||||||||||

|

Measured

|

143

|

4.5%

|

67.6

|

6.0

|

9.3

|

|||||||||||||||||||

|

Indicated

|

340

|

4.1%

|

67.4

|

6.1

|

9.3

|

|||||||||||||||||||

|

Measured + Indicated

|

483

|

4.2%

|

67.5

|

6.1

|

9.3

|

|||||||||||||||||||

|

Inferred

|

466

|

3.5%

|

71.8

|

6.3

|

10.0

|

|||||||||||||||||||

|

Total

|

949

|

3.9%

|

69.4

|

6.2

|

9.6

|

|||||||||||||||||||

|

Wonnerup Dry Mine – Western Australia(8)

|

||||||||||||||||||||||||

|

Measured

|

13

|

4.6%

|

77.5

|

12.0

|

8.8

|

|||||||||||||||||||

|

Indicated

|

6

|

4.8%

|

86.9

|

3.3

|

7.6

|

|||||||||||||||||||

|

Measured + Indicated

|

19

|

4.6%

|

80.5

|

9.2

|

8.4

|

|||||||||||||||||||

|

Inferred

|

3

|

4.4%

|

84.0

|

4.0

|

8.3

|

|||||||||||||||||||

|

Total

|

22

|

4.6%

|

81.0

|

8.5

|

8.4

|

|||||||||||||||||||

|

Ginkgo-Crayfish Dredge/ Dry Mines - New South Wales Australia(9)

|

||||||||||||||||||||||||

|

Measured

|

78

|

1.3%

|

47.9

|

18.2

|

12.4

|

|||||||||||||||||||

|

Indicated

|

-

|

-%

|

-

|

-

|

-

|

|||||||||||||||||||

|

Measured + Indicated

|

78

|

1.3%

|

47.9

|

18.2

|

12.4

|

|||||||||||||||||||

|

Inferred

|

59

|

1.1%

|

47.9

|

17.9

|

13.0

|

|||||||||||||||||||

|

Total

|

137

|

1.2%

|

47.9

|

18.1

|

12.6

|

|||||||||||||||||||

|

Kara/Cylinder - New South Wales Australia(10)

|

||||||||||||||||||||||||

|

Measured

|

-

|

-%

|

-

|

-

|

-

|

|||||||||||||||||||

|

Indicated

|

165

|

4.4%

|

49.4

|

12.9

|

12.0

|

|||||||||||||||||||

|

Measured + Indicated

|

165

|

4.4%

|

49.4

|

12.9

|

12.0

|

|||||||||||||||||||

|

Inferred

|

26

|

2.8%

|

54.4

|

24.4

|

14.2

|

|||||||||||||||||||

|

Total

|

191

|

4.1%

|

49.8

|

13.9

|

12.2

|

|||||||||||||||||||

|

Total Resources

|

||||||||||||||||||||||||

|

Measured

|

532

|

4.4%

|

49.9

|

7.5

|

8.8

|

|||||||||||||||||||

|

Indicated

|

911

|

3.6%

|

55.6

|

7.7

|

9.7

|

|||||||||||||||||||

|

Measured + Indicated

|

1,443

|

3.9%

|

53.2

|

7.6

|

9.3

|

|||||||||||||||||||

|

Inferred

|

861

|

3.5%

|

60.6

|

7.5

|

9.5

|

|||||||||||||||||||

|

Total

|

2,304

|

3.8%

|

55.8

|

7.6

|

9.4

|

|||||||||||||||||||

(See footnotes below the following table.)

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-4

TRONOX MINERAL SANDS – 2023-2022 RESERVES

|

Mineral Assemblage (% of THM)

|

||||||||||||||||||||||||

|

2023

|

2022

|

|||||||||||||||||||||||

|

MINE /

DEPOSIT

|

Reserve

Category

|

Material

(million

tons)

|

HM%

|

Ilmenite

|

Rutile

and

Leucoxene

|

Zircon

|

Change (+/-)

from 2022

(%)

|

Material

(million tons)

|

HM%

|

Ilmenite

|

Rutile

and Leucoxene |

Zircon

|

||||||||||||

|

Namakwa Sands Dry Mine – Western Cape RSA(2)

|

||||||||||||||||||||||||

|

Proven

|

136

|

7.4%

|

37.6

|

8.7

|

9.0

|

|||||||||||||||||||

|

Probable

|

551

|

5.4%

|

53.8

|

11.2

|

11.4

|

|||||||||||||||||||

|

Total

|

687

|

5.8%

|

49.7

|

10.6

|

10.8

|

|||||||||||||||||||

|

KZN Sands Hydraulic Mine – KwaZulu-Natal RSA(3)

|

||||||||||||||||||||||||

|

Proven

|

198

|

5.6%

|

61.7

|

7.4

|

7.6

|

|||||||||||||||||||

|

Probable

|

11

|

3.7%

|

51.8

|

5.0

|

7.0

|

|||||||||||||||||||

|

Total

|

209

|

5.5%

|

61.3

|

7.3

|

7.6

|

|||||||||||||||||||

|

Cooljarloo – Dredge Mine – Western Australia(4)

|

||||||||||||||||||||||||

|

Proven

|

210

|

1.6%

|

61.5

|

7.7

|

10.7

|

|||||||||||||||||||

|

Probable

|

130

|

2.0%

|

60.5

|

8.3

|

12.3

|

|||||||||||||||||||

|

Total

|

340

|

1.8%

|

61.1

|

8.0

|

11.4

|

|||||||||||||||||||

|

Atlas-Campaspe Dry Mine – New South Wales Australia(6)

|

||||||||||||||||||||||||

|

Proven

|

110

|

6.3%

|

60.7

|

11.8

|

12.5

|

|||||||||||||||||||

|

Probable

|

-

|

-%

|

-

|

-

|

-

|

|||||||||||||||||||

|

Total

|

110

|

6.3%

|

60.7

|

11.8

|

12.5

|

|||||||||||||||||||

|

Wonnerup Dry Mine – Western Australia(8)

|

||||||||||||||||||||||||

|

Proven

|

9

|

5.3%

|

70.1

|

19.1

|

9.6

|

|||||||||||||||||||

|

Probable

|

4

|

5.7%

|

77.5

|

11.4

|

8.8

|

|||||||||||||||||||

|

Total

|

13

|

5.4%

|

72.6

|

16.5

|

9.4

|

|||||||||||||||||||

|

Ginkgo-Crayfish Dredge/ Dry Mines – New South Wales Australia(9)

|

||||||||||||||||||||||||

|

Proven

|

26

|

1.9%

|

51.5

|

16.3

|

12.7

|

|||||||||||||||||||

|

Probable

|

-

|

-

|

-

|

-

|

-

|

|||||||||||||||||||

|

Total

|

26

|

1.9%

|

51.5

|

16.3

|

12.7

|

|||||||||||||||||||

|

Total Resources

|

||||||||||||||||||||||||

|

Proven

|

689

|

4.7%

|

54.0

|

9.1

|

9.5

|

|||||||||||||||||||

|

Probable

|

696

|

4.7%

|

54.4

|

10.9

|

11.4

|

|||||||||||||||||||

|

Total

|

1,385

|

4.7%

|

54.2

|

10.0

|

10.5

|

|||||||||||||||||||

| (3) |

For KZN Sands, price assumptions used for resource and reserve estimations are $ per metric ton of Zircon, $ per metric ton of Ilmenite and $ per metric ton of Rutile. The

cutoff grade used for the resource estimate is based on a break-even cutoff of % ilmenite. Reserves are defined by a complex optimization process which is explained in detail in the Namakwa Sands TRS. Saleable product yield

(recovery) used for our reserve estimates were % per metric ton of Zircon, % per metric ton of Ilmenite and % per metric ton of Rutile.

|

| (4) |

For Cooljarloo, price assumptions used for resource and reserve estimations are $ per metric ton of Zircon, $ per metric ton of Chloride Ilmenite, $ per metric ton of Rutile

and $ per metric ton of Leucoxene. The cutoff grade used for the resource estimate is based on a nominal bottom cut of % HM. Reserves are defined by a complex optimization process which is explained in detail in the

Cooljarloo TRS. Saleable product yield (recovery) used for our reserve estimates were % per metric ton of Zircon, % per metric ton of Chloride Ilmenite, % per metric ton of Rutile and % per metric ton

of Leucoxene.

|

| (5) |

For Dongara, price assumptions used for preliminary resource economic assessments are $ per metric ton of Zircon, $ per metric ton of Chloride Ilmenite, $ per metric ton of

Rutile and $ per metric ton of Leucoxene.

|

| (6) |

For Atlas-Campaspe, price assumptions used for resource and reserve estimations are $ per metric ton of Zircon, $ per metric ton of Chloride Ilmenite, $ per metric ton of

Sulfate Ilmenite, $ per metric ton of Rutile and $ per metric ton of Leucoxene (East). The cutoff grade used for the resource estimate is based on a nominal bottom cut of % HM. Reserves are defined by a complex

optimization process which is explained in detail in the Atlas-Campaspe TRS. Saleable product yield (recovery) used for our reserve estimates were % per metric ton of Zircon, % per metric ton of Ilmenite, % per

metric ton of Rutile and % per metric ton of Leucoxene.

|

| (7) |

For Port Durnford, price assumptions used for preliminary resource economic assessments are $ per metric ton of Zircon, $ per metric ton of Ilmenite and $ per metric ton of

Rutile.

|

| (8) |

For Wonnerup, price assumptions used for resource and reserve estimations are $ per metric ton of Zircon, $ per metric ton of Chloride Ilmenite, $ per metric ton of Sulfate

Ilmenite, $ per metric ton of Secondary Ilmenite and $ per metric ton of Leucoxene.

|

| (9) |

For Ginkgo-Crayfish, price assumptions used for resource and reserve estimations are $ per metric ton of Zircon, $ per metric ton of Chloride Ilmenite, $ per metric ton of

Sulfate Ilmenite, $ per metric ton of Rutile and $ per metric ton of Leucoxene (East).

|

| (10) |

For Kara/Cylinder, price assumptions used for preliminary resource economic assessments are $ per metric ton of Zircon, $ per metric ton of Chloride Ilmenite, $ per metric ton

of Sulfate Ilmenite, $ per metric ton of Rutile and $ per metric ton of Leucoxene (East).

|

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-5

Individual Property Disclosure

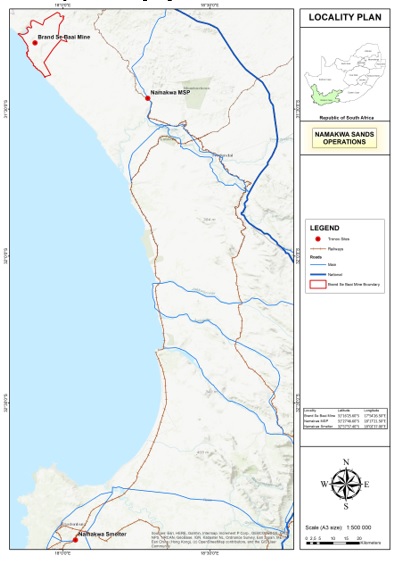

Tronox Northern Operations (Cooljarloo)

Tronox Management Pty Ltd is a subsidiary of Tronox Holdings plc and is the operator of Tronox Northern Operations which includes:

| • |

| • |

Cooljarloo West and Osprey deposits, which conjoin the Cooljarloo Mine operations;

|

| • |

Chandala Processing Plant, 60 km north of Perth, where the heavy mineral concentrates (HMC) are separated into saleable mineral products and also where ilmenite is further upgraded to synthetic rutile;

|

| • |

The laboratory and mineral testing facility is also located at the Chandala site.

|

Mining tenements in Australia are managed at the State or Territorial level. In Western Australia, Mining Leases, Exploration Licenses and Retention Licenses are granted and administered by the Western

Australian Department of Mines, Industry Regulation and Safety.

Tronox operates under four (4) mining leases which are 100% held by Tronox Management Pty Ltd., a wholly owned subsidiary of Tronox Holdings plc as shown in the Table below.

Mining Tenement Schedule

|

Region

|

Tenement

|

Tenement Type

|

Area (Ha)

|

Grant Date

|

Expiry/ Renewal Date

|

Commitment US$/a

|

Rent U$/a

|

Status of Rights

|

|

|

Cooljarloo

|

M70/1398

|

Mining Lease

|

9,744

|

2-Mar-20

|

1-Mar-41

|

701,600

|

138,900

|

Active Mining Lease

|

|

|

(Previously MSA 268)

|

|||||||||

|

Cooljarloo (West)

|

M70/1314

|

Mining Lease

|

3,782

|

18-Mar-15

|

17-Mar-36

|

272,300

|

53,915

|

EPA approval pending

|

|

|

Cooljarloo (West)

|

M70/1333

|

Mining Lease

|

420

|

4-Apr-16

|

3-Apr-37

|

30,310

|

6,000

|

EPA approval pending

|

|

|

Osprey

|

M70/1413

|

Mining Lease

|

1,319

|

5-Jul-22

|

4-Jul-23

|

132,000

|

31,680

|

Approvals process commenced

|

Tronox has one active mine site at Cooljarloo that was originally controlled by a State Agreement Act with the State of Western Australia. This area was covered by State Agreement Act MSA 268 which was

originally granted in 1989 for a period of 21 years. It was extended for a further 10-year term which expired in 2020. MSA 268 was replaced by Mining Lease M70/1398 which will expire in 2041.

Cooljarloo West is located within Mining Leases 70/1314 and 70/1333. Osprey is located within Mining Lease 70/1413. Granting of rights to mine are pending environmental approval.

The minerals in Western Australia belong to the Crown (the State of Western Australia) and Tronox is obligated to pay a 5% revenue- based royalty on saleable mineral products. This is factored into the

valuation models and optimisations conducted by Tronox.

A private royalty of 10c/t of VHM is paid for a portion of the northern section of the Cooljarloo tenement. Based on the current mine plan, mining in this royalty agreement area will cease by 2025 and

the amounts paid are not material to the business.

On Mining Lease 70/1333 Tronox agrees to pay the previous holder of the exploration lease a royalty of 1% of a previously agreed price for each tonne of Valuable Heavy Mineral recovered from the Mining

Lease. The cost will also be immaterial to the business.

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-6

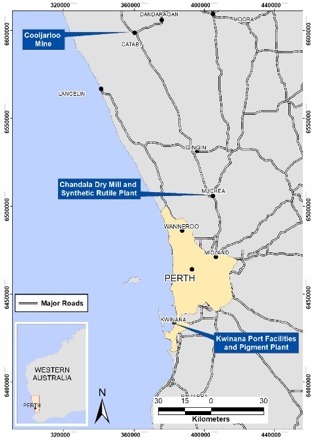

The Cooljarloo Mine is located at coordinates latitude 30°39'S and longitude 115°27'E.

Location of Western Australian Operations

The Brand Highway is a major bitumen road running from Muchea, just North of Perth up to Geraldton, a provincial city 450 km north of Perth. The road runs just past the Western boundary of the Chandala

site and just past the Eastern boundary of the Cooljarloo mine site. It is suitable for all weather and wide loads.

There is a 132 kV power line that also runs from Perth to Geraldton which passes near the Chandala site and through the mine site. Tronox has a substation on its property that draws and reticulates 22

kV power from the sub-station connected to the main high voltage distribution line. At the various locations power is ultimately transformed down to 415 V. The same situation exists for Chandala and it gets power from the same main line.

Two gas pipelines run just a kilometer to the West of the Chandala site. They are referred to as the Dampier to Bunbury Natural Gas pipeline (DBNG) and also the Parmelia line which originates just south

of Geraldton. The Chandala Mineral Separation Plant currently gets supply for driers and re-heaters from the Parmelia line.

The countryside surrounding both Chandala and Cooljarloo is relatively flat. This made the construction of buildings and fixed plant straightforward. Storage ponds for solid waste from the MSP were able

to be made quite shallow only being a few meters above natural ground level.

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-7

There is a large freshwater aquifer (Yarragadee) immediately to the west of the Brand highway adjacent to the Chandala site. Tronox has a borefield there that supplies the licensed 1 megaliter per annum

of water that the site requires. Even in times of severe drought, supply from this aquifer has never been at risk. Cooljarloo draws from an extensive field of relatively shallow bores and also an extension of the Yarragadee aquifer. To limit

pumping distances, it has been preferable to have multiple smaller bores around the site since the dredging operation has travelled more than 40 km within the mining lease area since 1989. Tailings disposal at Cooljarloo is all placed behind the

dredging operations and incorporated into the rehabilitated profile. There is a registered waste disposal pit where wastes from the MSP, the Synthetic Rutile plant and from the Kwinana pigment plant are licensed to be stored. These pits cells are

constructed above the water table and are clay lined. When each cell is full it is capped to minimize the ingress and egress of water.

The Chandala operation utilizes two port facilities. The Port of Fremantle is used for export of bagged and containerized mineral products and the Port of Bunbury is used for bulk shipments. Tronox

rents storage and warehousing facilities at or nearby to those sites.

For Cooljarloo there is a well-equipped modern permanent single person’s quarters (SPQ), capable of accommodating up to 160 people or approximately 70% of the work force. At Chandala, employees and

contractors are primarily sourced from the Perth metropolitan and surrounding areas.

History

Cooljarloo

The Cooljarloo tenements were originally pegged in 1972 by Kamilaroi Oil Company following the discovery of the Eneabba Deposits. They were subsequently obtained by Yalgoo Minerals Pty Ltd and Tific Pty

Ltd in 1985 which became part of TiO2 Corporation NL (TiO2).

In 1988 prior to mining commencing, the Cooljarloo Joint Venture was formed between Kerr-McGee Chemical Corp and Minproc Ltd, subsequent reorganizations of both partners led to 100% ownership under

Tronox in 2012.

No geological data generated by owners prior to the formation of the Cooljarloo Joint Venture is in use.

Cooljarloo West

In 1990 drilling by Peko Exploration Ltd delineated a zone of deep low-grade mineralisation but further drilling failed to intercept economic mineralisation. The tenements were relinquished in 1992.

Image Resources later pegged the area which were acquired by Tronox in 2005. Drilling completed by Tronox in 2007 delineated the deposits named Woolka Road, Harrier and Kestrel and Resources and

Reserves are based only on data generated by Tronox.

Cooljarloo Summary of Mineral Resources as of December 31, 2023

|

Mineral Assemblage

|

||||||||||||

|

Deposit

|

Mineral Resource

Classification

|

Tons of Material

(Mt)

|

Grade

HM% |

Ilmenite

(% of HM)

|

Rutile +

Leucoxene (%

of HM)

|

Zircon (% of

HM)

|

||||||

|

Cooljarloo

|

Measured

|

|||||||||||

|

Indicated

|

||||||||||||

|

Inferred

|

||||||||||||

|

Cooljarloo West

|

Measured

|

|||||||||||

|

Indicated

|

||||||||||||

|

Inferred

|

||||||||||||

|

Total Mineral Resources

|

||||||||||||

| (1) |

Mineral resources are exclusive of mineral reserves.

|

| (2) |

Price assumptions used for resource and reserve estimations are $ per metric ton of zircon, $ per metric ton of Chloride Ilmenite, $ per metric ton of Rutile and $

per metric ton of Leucoxene. Mineral prices used in Reserve estimation are substantially in line with the prices for each of our products published quarterly by independent consulting companies.

|

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-8

For a comparison of the reported resources as of December 31, 2023 with the resources as of December 31, 2022, see table on page A-3. The decrease in resources in 2023 as compared to 2022

is primarily attributable to mining depletion.

Cooljarloo Summary of Mineral Reserves as of December 31, 2023

|

Mineral Assemblage

|

||||||||||||||

|

Deposit

|

Mineral Resource

Classification

|

Tons of Material

(Mt)

|

Grade

HM% |

Ilmenite

(% of HM)

|

Rutile +

Leucoxene (%

of HM)

|

Zircon (% of

HM)

|

Change

From 2022

|

|||||||

|

Cooljarloo

|

Proved

|

|||||||||||||

|

Probable

|

||||||||||||||

|

Cooljarloo West

|

Proved

|

|||||||||||||

|

Probable

|

||||||||||||||

|

Total Mineral Resources

|

||||||||||||||

For a comparison of the reported reserves as of December 31, 2023 with the resources as of December 31, 2022, see table on page A-4. The

decrease in reserves in 2023 as compared to 2022 is primarily attributable to mining depletion.

The Cooljarloo project was established in 1988. Being situated on an historical coastline, the ore body is made up of conventional mineral sands strandlines and eminently suited to dredge mining and

gravity concentration.

Since commencement, the operation has been running continuously and has thus far consumed 640 Mt of ore at approximately 2.8% HM grade. The current reserves are 307 Mt tons at 1.8% HM grade, which gives

a further 15 years of life. The current resources, which are exclusive of reserves, are 295 Mt at 1.6% HM.

Extensive and systematic exploration drilling activities are conducted at Cooljarloo and adjacent deposits on an annual basis to upgrade resources and reserves. Final reserve delineation drilling is

completed to a 50m x 40m or 50m x 20m spacing depending on the geological complexities of the orebody. Final drilling is completed three or more years in advance of the mining face to allow timely and accurate mine planning to be completed. Over

the past 13 years there has been an average of 52,000 meters of drilling completely annually at Cooljarloo. Drilling will continue is 2024.

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-9

Cooljarloo mine has operated with 2 dredges in the one pond since 1999. The original Ellicott Cooljarloo1 dredge operates in tandem with the smaller capacity Neumann built Pelican dredge which was

brought into service in 2012. These bucket wheel dredges operate in a purpose-built pond which sits within the ore mining limit. The original dredge and concentrator were sized to operate at 12 Mt per annum but the original dredge has progressively

been expanded and addition of the second dredge has seen the project expand to a maximum of 25Mt per annum to counteract the impact of lower ore grades and also enable improved resource utilization through economies of scale and increased product

values.

A wet concentrator also floats in the dredge pond and is on two pontoons covering 2,250 square meters. Spiral gravity concentrators separate the higher density valuable minerals from the lower density

trash mineral and lowest density tailings quartz grains. The spiral circuit consists of five stages. Roughers, middlings, cleaners, recleaners and classifiers. Both dredges pump their feed simultaneously to the floating wet concentrator via

floating pipelines and high voltage cables for power.

Over the past 36 years of operation the metallurgical circuitry of the wet plant has remained relatively unchanged save for expanding the throughput to approximately 2850 tph. This allowed the

processing of lower grade ore which has been shown to have a better revenue to cost ratio compared to the original project assumptions. At the time of the capacity increase, spirals that were at the end of their useful life were replaced with more

modern units, of higher efficiency, to cope with both additional throughputs, the lower average feed grade, higher clay fines in the ore and maintain an acceptable mineral recovery.

HMC at Cooljarloo is loaded by front end loader into 93 tonne triple road trains for haulage to the Chandala Mineral Separation Plant (MSP). Both the mine and MSP are based on physical separation

processes. There is no need for chemical or physical alteration to achieve good product recovery and quality. Attritioning is a critical process step to ensure clean mineral surfaces that are responsive to the electrostatic HT separators. The

attritioned HMC is presented by filter belt to a natural gas fired drier that not only removes the moisture but heats the mineral so that it is most responsive to the primary stage electrostatic separation circuit.

The unit operations at the MSP are many and varied but the significant ones are as follows:

| • |

vibrating and reciprocating woven wire screening;

|

| • |

mechanical slurry attritioning;

|

| • |

gas fired fluid bed drying, reheating and cooling;

|

| • |

HT Roll, Coronastat and Plate electrostatic separators;

|

| • |

Rare Earth Drum, Rare Earth Roll, Induced Roll and Semi-Lift magnetic separators;

|

| • |

Hydrosizing; and

|

| • |

spiral gravity and centrifugal jig concentrators.

|

The equipment and infrastructure at both Cooljarloo and Chandala are in good order having been upgraded several times such that the total throughput of the mining operation now averages 21 Mt per annum

and whilst the Mineral Separation Plant has not needed capacity increase, updated technology and implementation of continuous improvement programmes have resulted in significant increases in mineral recoveries.

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-10

Since Cooljarloo is an operating mine and processing plant, capital is mostly a sunk cost. There is minor stay in business capital incurred annually and there is US$55M of capital forecast with the move

to the nearby Cooljarloo West dredging orebody expected in approximately 2033.

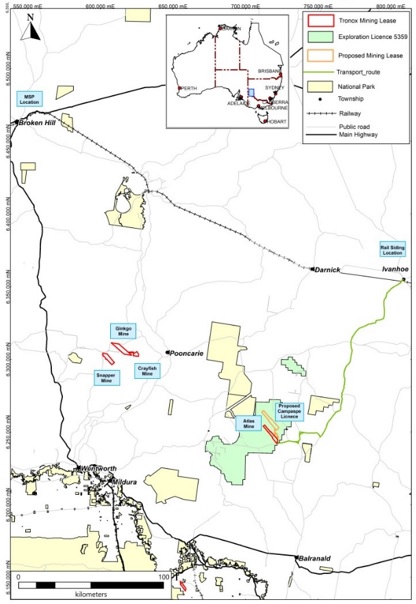

Tronox Eastern Operations (Atlas-Campaspe)

Tronox Mining Australia Ltd is a subsidiary of Tronox Holdings plc and is the operator of Tronox Eastern Operations which includes:

| • |

The Ginkgo Mine, 110 km north of Wentworth in southwestern New South Wales, where heavy mineral concentrates are currently produced from dredge mining operations;

|

| • |

The Snapper and Crayfish rehabilitation sites, adjacent to Ginkgo where former mineral sands mines are undergoing restoration following the completion of mining;

|

| • |

The Atlas-Campaspe project in southwestern New South Wales, 120 km northeast of Mildura, where heavy mineral concentrates are currently produced from dry mining operations at Atlas and site development

and approval activities have commenced for future mining operations at Campaspe;

|

| • |

A rail siding and HMC stockpile facility at Ivanhoe, approximately 140 km northeast of the Atlas Mine, where HMC is dispatched to Broken Hill for further processing.

|

| • |

Broken Hill Mineral Separation Plant in southwestern New South Wales, where the heavy mineral concentrates (HMC) are separated into mineral products and either railed approximately 430 km to the Port of

Adelaide or railed directly to Western Australia using the Trans Australian Railway;

|

| • |

Port of Adelaide, South Australia, where bulk mineral sands products from Broken Hill are loaded for export.

|

Mining tenements in Australia are managed at the State or Territorial level. In New South Wales, Mining Leases, Exploration Licenses and Assessment Leases are granted and administered by the New South

Wales Department of Primary Industries Mineral Resources Division.

The Development Consent for Atlas and Campaspe was granted in June 2014 and construction of the Atlas Project was completed in early 2023. The Atlas deposit is secured by Mining Lease 1767. The Campaspe

deposit is secured by the Atlas/Campaspe Mineral Sands Project Development Consent SSD_5012 from the Government of New South Wales. In November 2023 a mining lease application (MLA 639) was lodged over the Campaspe deposit, Grant of this tenement

is pending.

The minerals in New South Wales belong to the Crown (the State of NSW) and Tronox is obligated to pay a 4% revenue-based royalty on all saleable minerals produced.

All the land encompassing the intended mining area has been purchased by Tronox so no mining compensation payments to landowners will be required as part of the Atlas-Campaspe Project.

The net book value of Atlas-Campaspe, inclusive of mining and beneficiary equipment located in New South Wales as well as relevant mining tenements, as of December 31, 2023 was $

.

The Atlas mine is located at coordinates latitude 33°53’S and longitude 143°21’E. The Campaspe mine is located at coordinates latitude 33°49’S and longitude 143°22’E.

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-11

Regional location of Atlas/Campaspe Project

Infrastructure

Atlas

The Atlas minesite is located in southwestern New South Wales, 120 km northeast of Mildura and 90 km north of Balranald. Access to the licence area is via the Balranald Ivanhoe Hwy, the

Boree Plains —Gol Gol road and then through the official Atlas Mine Access Road. The Atlas mine consists of a centrally based Wet Concentrator Plant (WCP) and a Dry Mining Unit (DMU) both rated to 500 tph.

An on-site 200-person accommodation village has been constructed to house the workforce and consists of permanent and demountable buildings and facilities such as: Administration and Office Building;

Workshops; Process Area Crib Room and Amenities; Gymnasium; Basketball Court and Main Store. Electrical power is supplied directly from a centralized 5 Mwh diesel generation system.

Hydrological investigations identified a bore field location at the Northern end of the mine path, approximately 5km from the central start-up pit location. This bore field supplies water for the mining

operations and ancillaries. A total of seven bore pumps supply the required volume.

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-12

A RO Plant and potable water treatment plant sized to deliver 115m3/hour has been installed to supply wash water for the HMC and potable water for site buildings, wash pads and the accommodation

village.

A communication building is located adjacent to the communication tower for telecom and the Local Area Network (LAN). Data and telephone connection between the communications

building, process area, administration area and accommodation village are via a buried fiber optic cable.

HMC from the Atlas mine is transported by a combination of trucks and train. The road network consists of approximately 37 km of existing unsealed roads between the Atlas-Campaspe

Mine site access road and the intersection with the sealed Balranald-Ivanhoe Road. The remaining section is a 138 km long bitumen road leading to the Ivanhoe rail siding. HMC is loaded into a train for transport to the Broken Hill Mineral

Separation Plant (BH MSP) over approximately 301 km of railway.

Campaspe Project Status and Site Development Works

At the conclusion of mining at Atlas production will transition to Campaspe. Detailed mine planning and final approvals are underway. The development of the Campaspe site and

required plant to operate includes:

| • |

fencing of the mine lease (47 km);

|

| • |

construction of the access road (11 km);

|

| • |

construction of the mine corridor road (5.4 km);

|

| • |

construction of the process water dam (210,000 m3);

|

| • |

development of the mining pit;

|

| • |

development of the bore field and water reticulation systems;

|

| • |

relocation of workshops and amenities;

|

| • |

expansion of the accommodation village from 200 to 300 beds;

|

| • |

construction of a Primary Concentration Plant (PCP); and

|

| • |

relocation of Ginkgo/Snapper field booster pumps and piping.

|

History

In the Murray Basin fine heavy mineral occurrences were identified from 1982 to 1986 by Rio Tinto. Subsequently many smaller, coarser and high-grade deposits were also identified, and these formed the

first mineral sands mines to be developed in the region. Bemax Resources discovered the Ginkgo, Snapper and Crayfish deposits at Pooncarie in the early to mid-2000’s. Mining commenced at Ginkgo in 2005 and Snapper in 2010. Mining at Snapper was

completed in April 2022 and Crayfish was completed in July 2023. Ginkgo is still being mined today by Tronox.

The Atlas-Campaspe Project replaces production from the completed Snapper and Crayfish deposits and the Ginkgo mining operation when it ceases production in mid-2024. Atlas commenced full production in

early 2023.

Securities and Exchange Commission

Division of Corporation Finance

Appendix A – Page A-13

Summary of Resources and Reserves

Atlas-Campaspe Summary of Mineral Resources as of December 31, 2023

|

Deposit

|

Mineral Reserve

Classification

|

Ore Tons (Mt)

|

Grade

HM%

|

Mineral Assemblage

|

||||||||

|

Ilmenite +

Leucoxene (% of

HM)

|

Rutile (%

of HM)

|

Zircon (%

of HM) |

||||||||||

|

Atlas

|

Measured

|

|||||||||||

|

Indicated

|

||||||||||||

|

Inferred

|

||||||||||||

|

Campaspe

|

Measured

|

|||||||||||

|

Indicated

|

||||||||||||

|

Inferred

|

||||||||||||

|

Total Mineral Resources

|

||||||||||||

| (1) |

Mineral resources are exclusive of mineral reserves.

|

For a comparison of the reported resources as of December 31, 2023 with the resources as of December 31, 2022, see table on page A-3. The

decrease in resources in 2023 as compared to 2022 is primarily attributable to mining depletion.

Atlas-Campaspe Summary of Mineral Reserves as of December 31, 2023

|

Deposit

|

Mineral Reserve

Classification

|

Ore Tons

(Mt)

|

Grade

HM%

|

Mineral Assemblage

|

Change from

2022

|

|||||||||

|

Ilmenite +

Leucoxene (% of

HM)

|

Rutile (% of HM)

|

Zircon (%

of HM)

|

||||||||||||

|

Atlas

|

Proved

|

|||||||||||||

|

|

Probable

|

|||||||||||||

|

Campaspe

|

Proved

|

|||||||||||||

|

Probable

|

||||||||||||||

|

Total Mineral Reserves

|

||||||||||||||

| (1) |

Price assumptions used for resource and reserve estimations are $ per metric ton of zircon, $ per metric ton of Chloride Ilmenite, $ per metric ton of Sulfate Ilmenite,

$ per metric ton of Rutile and $ per metric ton of Leucoxene (East). Mineral prices used in reserve estimation are substantially in line with the prices for each of our products, published quarterly by independent

consulting companies.

|

| (2) |

Conversion of in ground grade to saleable product yield (recovery), considering all the losses during mining and processing, is typically % for ilmenite, % for rutile, %

for Leucoxene and % for zircon.

|

For a comparison of the reported reserves as of December 31, 2023 with the resources as of December 31, 2022, see table on page A-4. The decrease in reserves in 2023 as compared to 2022 is primarily attributable to mining depletion.

Condition of Property