VIA EDGAR

December 20, 2023

U.S. Securities and Exchange Commission

Division of Corporation Finance

Office of Manufacturing

100 F Street, N.W.

Washington, DC 20549

Attn: Ms. Eiko Yaoita Pyles and Mr. Andrew Blume

Re: Constellium SE

Form 20-F for the fiscal year ended December 31, 2022 Filed March 14, 2023

Form 6-K furnished July 26, 2023

File No. 001-35931

Dear Ms. Pyles and Mr. Blume:

Set forth below are responses of Constellium SE, a company incorporated in France (together with its subsidiaries, “Constellium” or the “Company”), to the comments from the Staff of the Division of Corporation Finance (the “Staff”) of the U.S. Securities and Exchange Commission provided in your letter, dated November 21, 2023, with respect to the Company’s annual report on Form 20-F referenced above (the “Form 20-F”) and the Form 6-K referenced above (the “6-K”). For the Staff’s convenience, the text of each of the Staff’s comments is set forth below in bold, followed in each case by the Company’s response.

Form 20-F for the fiscal year ended December 31, 2022 Operating and Financial Review and Prospects

Segment Adjusted EBITDA, page 46

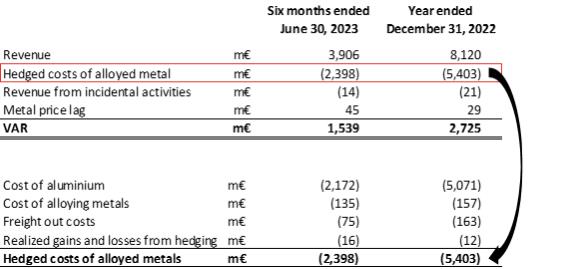

| 1. | We note your response to comment 3 and the example provided in Exhibit 1. Our comment is in response to your presentation of Adjusted EBITDA in total. You state that the metal price lag adjustment is intended to eliminate the non-cash timing difference between metal purchase costs intended to be passed through to customers and metal purchase costs accounted in cost of sales. This adjustment appears to have the effect of changing the basis of accounting for inventory, which is inconsistent with Question 100.04 of the non-GAAP C&DI’s. Please revise accordingly or explain in more detail why you believe this adjustment is appropriate. |

We respectfully acknowledge the Staff’s comment and submit that we believe our adjustment is appropriate as more fully described below.

1