VIA EDGAR

October 30, 2023

U.S. Securities and Exchange Commission

Division of Corporation Finance

Office of Manufacturing

100 F Street, N.W.

Washington, DC 20549

Attn: Ms. Eiko Yaoita Pyles and Mr. Andrew Blume

Re: Constellium SE

Form 20-F for the fiscal year ended December 31, 2022 Filed March 14, 2023

Form 6-K furnished February 22, 2023

Form 6-K furnished July 26, 2023

File No. 001-35931

Dear Ms. Pyles and Mr. Blume:

Set forth below are responses of Constellium SE, a company incorporated in France (together with its subsidiaries, “Constellium” or the “Company”), to the comments from the Staff of the Division of Corporation Finance (the “Staff”) of the U.S. Securities and Exchange Commission provided in your letter, dated September 29, 2023, with respect to the Company’s annual report on Form 20-F referenced above (the “Form 20-F”) and the Forms 6-K referenced above (the “6-Ks”). For the Staff’s convenience, the text of each of the Staff’s comments is set forth below in bold, followed in each case by the Company’s response.

Form 20-F for the fiscal year ended December 31, 2022 Operating and Financial Review and Prospects

Results of Operations, page 40

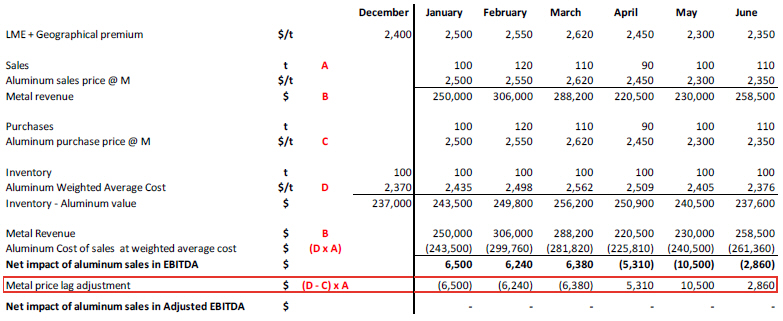

| 1. | When you discuss revenue fluctuations between periods, specifically describe the extent to which changes are attributable to changes in prices, changes in the volume or amount of goods or services being sold, and the introduction of new products or services. Although you quantify on pages 40, 43, and 45-46 the percentage change in tons shipped and revenue per ton for the applicable fiscal years, you do not quantify the impact of volumes or prices in terms of revenue dollars. See Item 303(b)(2) of Regulation S-K and SEC Release No. 33-8350. |

We respectfully acknowledge the Staff’s comment and in future filings, we will include the information requested by the Staff above in relation to the discussion of revenue fluctuations between periods.

1