![]()

Notice of Exempt Solicitation (Pursuant to Rule 14a-103)

This is not a solicitation of authority to vote your proxy. Please DO NOT send us your proxy card; The proponents are not able to vote your proxies, nor does this communication contemplate such an event. The proponents urge shareholders to vote for Item No. 8 on the registrant’s definitive proxy materials.

Name of the Registrant: General Electric Co.

Name of persons relying on exemption: MKT Forces Trading Ltd.

Address of persons relying on exemption: Unit 9-2, 94 Elizabeth Street, Melbourne, VIC, Australia 3000

Written materials are submitted pursuant to Rule 14a-6(g)(1) promulgated under the Securities Exchange Act of 1934. Submission is not required of this filer under the terms of the Rule, and is made voluntarily.

Proposal to General Electric (NYSE: GE) seeks disclosure around asset resilience to a net zero pathway

Key Points

| ● | Summary of Proposal: The proponents request GE provide an audited report to address how application of the International Energy Agency’s (IEA) Net Zero Emissions by 2050 pathway (NZE) would affect the assumptions and estimates that underlie GE’s valuation and expected cash flow assessments. |

| ● | This proposal seeks information investors need to assess GE’s position prior to the GE Vernova spinoff as GE’s gas strategy is misaligned with its own net zero by 2050 commitment, doubling down on gas power contrary to the gas demand modelling provided by reputable net zero emissions scenarios. |

| ● | This misalignment presents financial risk for the company and its investors, and sees GE placing too much faith on unproven technologies and missing out on wind power opportunities, with gas acting as a barrier to renewable penetration in emerging markets. |

| ● | GE’s current disclosure is contrary to stated investor expectations and lags behind its peers’ disclosure.Shareholders voting for this proposal would provide a clear signal to GE that they require information related to asset resilience to a net zero emissions by 2050 pathway, and would ensure that GE will provide this information through disclosure related to GE Vernova. |

About the Proponents

MKT Forces Trading Ltd. (Market Forces) is an environmental advocacy organisation seeking to shift finance away from activities contrary to the Paris agreement climate goals and into activities that protect and sustain the environment.

Henry H. Barrett, through his representative, Newground Social Investment, which manages money for institutions and individuals of means who are principled, proactive, and inspired to make a difference with their investments.

Please contact Bernadette Maheandiran (bernadette@marketforces.org.au) with any questions about this proposal. For the full investor briefing, please visit marketforces.org.au.1

GE’s new gas plans misaligned with net zero scenarios

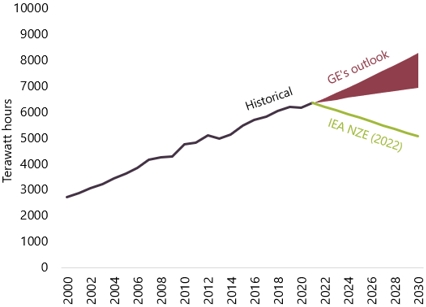

General Electric (GE) has failed to respond to investor demands to align corporate strategy with the Paris Agreement and net zero emissions by 2050, a proposal2 supported by 98% of GE’s shareholders. Instead, GE is undermining the company’s commitments to these climate goals, continuing to pursue plans for new gas and liquefied natural gas (LNG) to power assets (targeting a gas turbine market of 25 to 30 gigawatts annually).3 Such plans contradict the gas demand modelling provided by the IEA in its widely-referenced NZE scenario.4

Global gas power generation - Historical, IEA NZE and GE outlook

“GE’s outlook” is an estimate based on the company’s stated expectation of “low-single-digits” growth in gas generation over the next decade, which we have interpreted as 1-3% per annum. Source: Ember, 5 IEA, 6 GE7

1 https://www.marketforces.org.au/proposal-to-ge-on-asset-resilience-disclosure-march-2023/

2 https://engagements.ceres.org/ceres_engagementdetailpage?recID=a0l1H00000BseQrQAJ

3 https://www.ge.com/sites/default/files/ge_ar2022_annualreport.pdf

4 https://www.iea.org/reports/world-energy-outlook-2022

5 https://ember-climate.org/data-catalogue/yearly-electricity-data/

6 https://www.iea.org/reports/world-energy-outlook-2022

7https://www.ge.com/sites/default/files/ge_ar2022_annualreport.pdf

| 2 |

GE’s new gas plans pose unacceptable financial risk to investors and miss opportunities

Given the upcoming spinoff of its power business, GE’s proposed LNG buildout could damage the financial position and reputation of “GE Vernova” and other GE businesses, as well as the net zero emissions commitments of investors in these businesses. GE is betting shareholder capital on these new gas plans,8 apparently disregarding the financial risks posed by a Paris-aligned energy transition and ongoing demand destruction due to volatile LNG prices.

| ● | Lower utilisation rates, phase outs and cancellations of fossil gas and LNG assets may result in losses to GE’s long term equipment and services revenues, and also risk presently GE-owned gas power assets becoming stranded. This risk is exacerbated by today’s high gas prices, elevating sovereign risk in emerging markets, with cancellations in the construction phase and potentially large write-downs on GE’s balance sheet becoming more likely. |

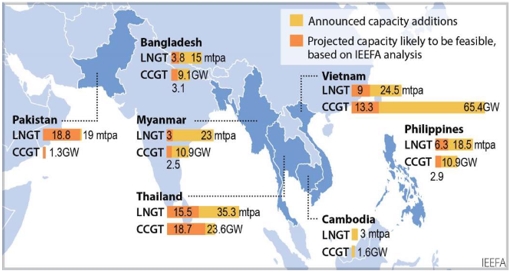

Likely feasibility of proposed LNG capacity additions in emerging Asia

IEEFA, Examining

Cracks in Emerging Asia’s LNG-to-Power Value Chain9

| ● | Such value destruction would not be a first for GE. Its ill-fated acquisition of French company Alstom’s gas power and grid assets in 2015 eventually resulted in a US$22 billion goodwill impairment three years later and coincided with a precipitous decline in the company’s share price. |

With renewable energy tariffs getting cheaper and outcompeting gas,10 GE and its GE Vernova spin off faces financial risk from its plans for expensive and volatile fossil gas projects - not just through equity ownership, but also through gas turbine supply and servicing earnings. Yet GE fails to disclose adequate information for investors to properly assess the company’s transition risk exposure and management practices.

8 https://marketforces.net/ge/

9 http://ieefa.org/wp-content/uploads/2021/12/Examining-Cracks-in-Emerging-Asias-LNG-to-Power-Value-Chain_December-2021.pdf

10 https://www.irena.org/news/pressreleases/2022/Jul/Renewable-Power-Remains-Cost-Competitive-amid-Fossil-Fuel-Crisis

| 3 |

GE’s disclosure falls afoul of investor expectations and is out of line with peers

GE's misalignment with established net zero scenarios and the ensuing financial risks make it imperative that GE provide additional disclosure, already provided by peer companies, to inform investors of the resilience of GE’s energy-related assets in a credible net zero by 2050 pathway.

Pre-spin-off 10-K disclosures are unlikely to contain the level of information needed for investors to assess the viability of GE’s plans, despite GE’s claims to the contrary.11 GE’s 10-K disclosures relating to the GE Healthcare12 spin-off contained little information about the company’s long-term assumptions or capital allocation plans, nor any assessment of the business’s resilience under different scenarios. Given the immense transition risk facing the gas power industry, such disclosures constitute essential information for potential investors in GE Vernova.

GE’s disclosures fall short of large global energy companies

| Disclosure element | GE’s disclosure | Peer disclosure |

| Capital expenditures |

GE does not disclose the breakdown of capex being allocated to gas and renewables in its power business.

GE has also not provided information on how its capital allocation plans would be affected by the application of a 1.5°C scenario. |

Major turbine producer Mitsubishi Heavy Industries (MHI) discloses capex and investment plans of up to 2 trillion yen by 2030 to meet its commitment to be net zero by 2040.13

Siemens Energy discloses last-period capex allocated to EU Taxonomy-eligible activities (largely renewables).14

BP provides a target for capital allocation to transition-related industries to 2030.15 |

| Potential impairments |

GE does not disclose how carrying values (and hence impairments) would be impacted by a 1.5°C-aligned scenario.

GE’s latest reporting includes ‘energy transition’ as a key strategic risk, but only describes financial risk in broad terms.16 |

Shell discloses a sensitivity analysis for the carrying values of its gas assets using a range of price scenarios, including IEA NZE.17

Eni discloses the potential impact of climate-related risks and opportunities on the organization’s financial position in terms of fair value of assets.18 |

11 https://www.sec.gov/Archives/edgar/data/40545/000130817923000208/ge4121681-def14a.htm#d412168a040

12 https://investor.gehealthcare.com/sec-filings/sec-filing/10-k/0001932393-23-000025

13 https://www.mhi.com/library/business/pdf/2021_cn_summary.pdf

14 https://assets.siemens-energy.com/siemens/assets/api/uuid:2c6beb5b-85ef-4200-a361-6a4550a31b9b/2022-12-12-siemens-energy-ag-annual-report-2022.pdf?ste_sid=ef86c36af69e156c6dfef6e10dd3672f

15 https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/news-and-insights/press-releases/bp-integrated-energy-company-strategy-update.pdf

16 https://www.ge.com/sites/default/files/ge_ar2022_annualreport.pdf

17 https://reports.shell.com/annual-report/2021/_assets/downloads/shell-annual-report-2021.pdf

18 https://www.eni.com/assets/documents/eng/just-transition/2020/Eni-for-2020-Carbon-neutrality-by-2050.pdf

| 4 |

GE is also out of line with investor expectations such as the IGCC sector strategy for power companies19 and the Net Zero Asset Managers initiative.20 Climate Action 100+ finds GE’s decarbonisation strategy and capital alignment do not meet its criteria.21 Carbon Tracker and the Climate Accounting and Audit Project’s analysis of highly carbon-exposed companies22 finds GE to be completely lacking in reporting material climate-related matters in its financial statements.

Selected Assessments of GE Disclosure Omissions By Climate Action 100+

|

Capital Alignment ● The company is working to decarbonise its capital expenditures ● Discloses the methodology used to determine the Paris alignment of its future capital expenditures |

(Do not meet criteria) |

|

Climate Accounting and Audit ● The audited financial statements and notes thereto incorporate material climate-related matters. ● The audit report demonstrates that the auditor considered the effects of material climate-related matters in its audit. ● The audited financial statements and notes thereto incorporate the material impacts of the global drive to net zero greenhouse gas (GHG) emissions by 2050 (or sooner), (...) equivalent to achieving the Paris Agreement goal of limiting global warming to no more than 1.5°C. |

|

|

TCFD Disclosure ● The company employs climate-scenario planning to test its strategic and operational resilience. |

|

At the upcoming GE AGM on 3 May 2023, investors are therefore urged to vote FOR Shareholder Proposal No. 4 — Assess Energy-Related Asset Resilience (No. 8 on Definitive Proxy Solicitation Materials).

19 https://www.climateaction100.org/approach/global-sector-strategies/electric-utilities/

20 https://www.netzeroassetmanagers.org/

21 https://www.climateaction100.org/company/general-electric-company/#skeletabsPanel5

22 https://carbontracker.org/reports/still-flying-blind-the-absence-of-climate-risk-in-financial-reporting/

5