Exhibit 99.1

STORE Capital Announces Second Quarter 2022 Operating Results

Raises 2022 AFFO Per Share Guidance

SCOTTSDALE, Ariz., August 3, 2022 – STORE Capital Corporation (NYSE: STOR, “STORE Capital” or the “Company”), an internally managed net-lease real estate investment trust (REIT) that invests in Single Tenant Operational Real Estate, today announced operating results for the second quarter ended June 30, 2022.

For the quarter ended June 30, 2022:

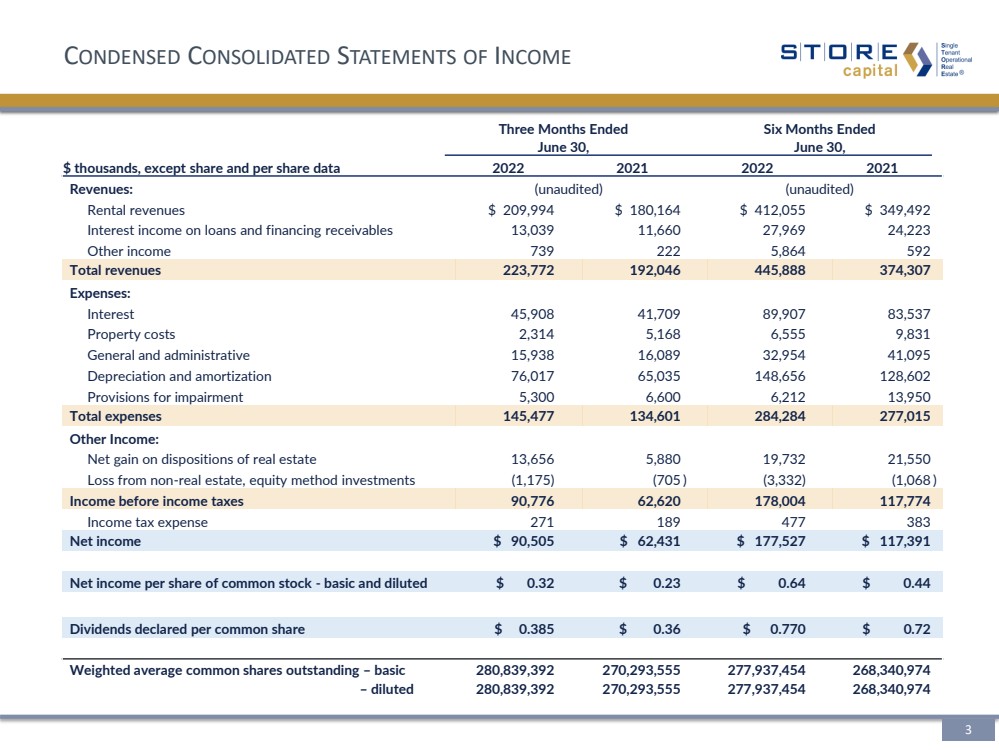

| ◾ | Total revenues of $223.8 million |

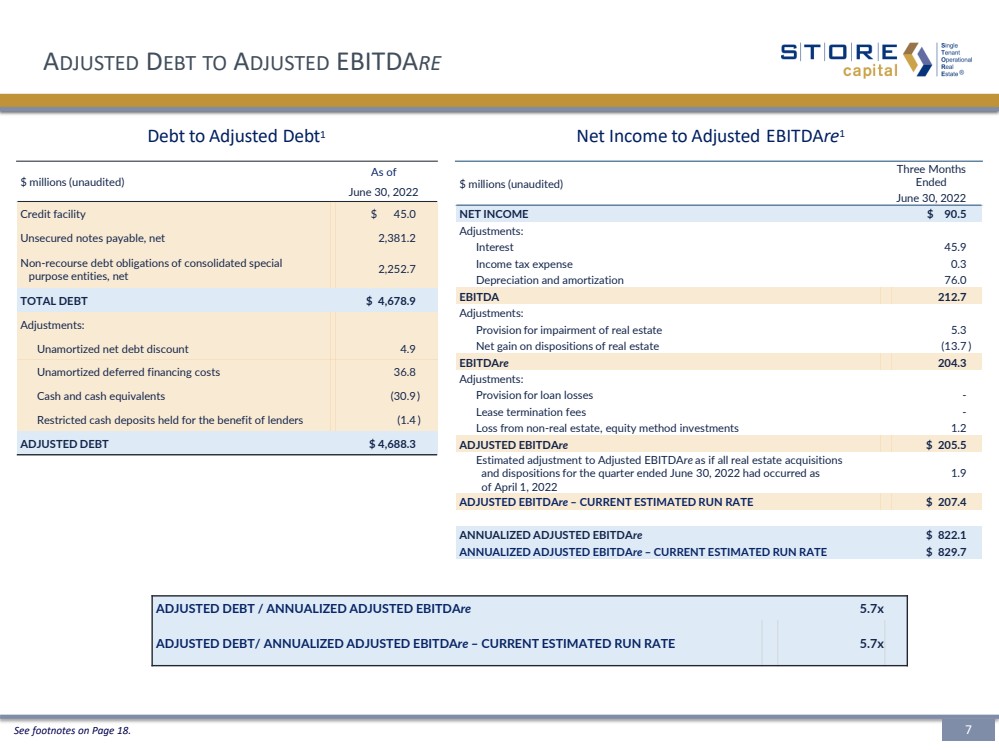

| ◾ | Net income of $90.5 million, or $0.32 per basic and diluted share, including an aggregate net gain of $13.7 million on dispositions of real estate |

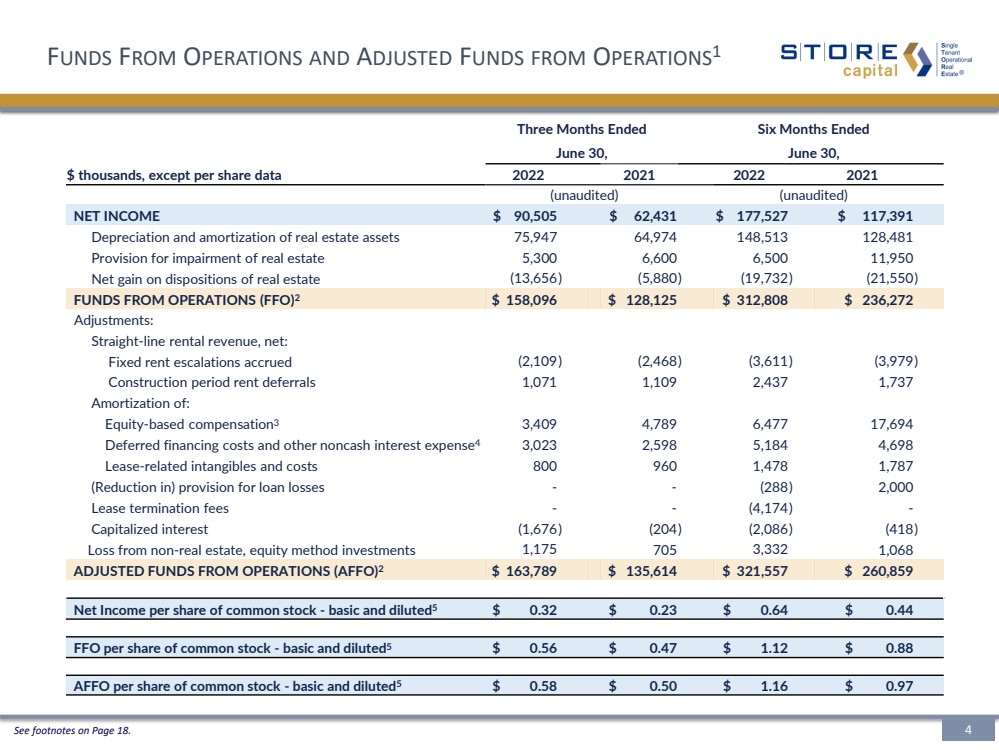

| ◾ | AFFO of $163.8 million, or $0.58 per basic and diluted share |

| ◾ | Declared a regular quarterly cash dividend per common share of $0.385 |

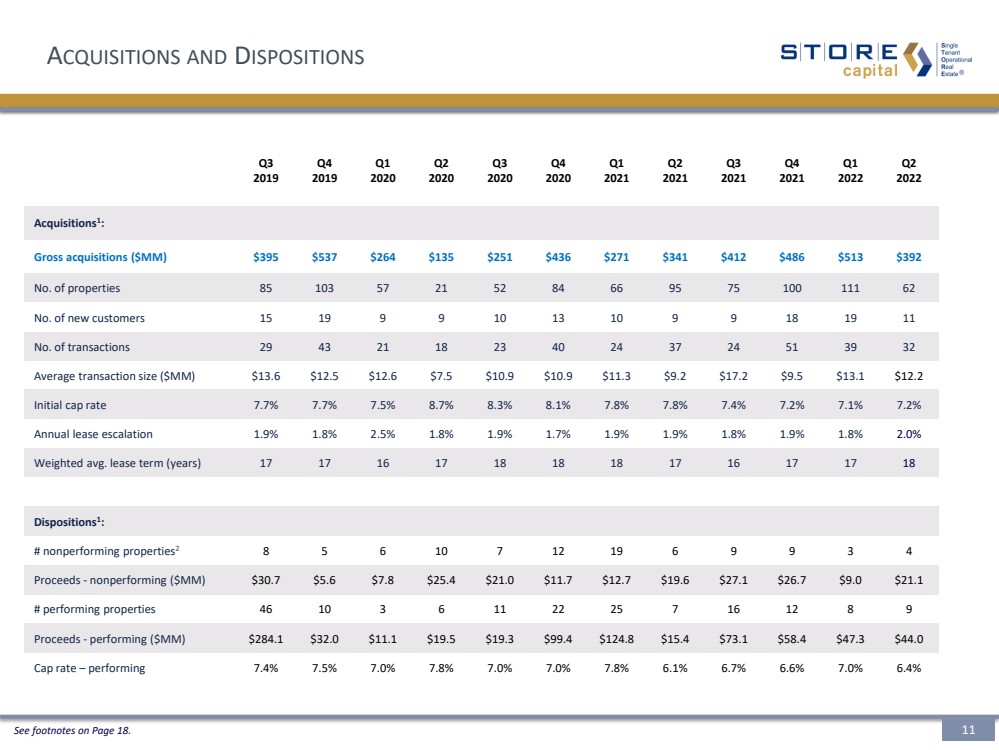

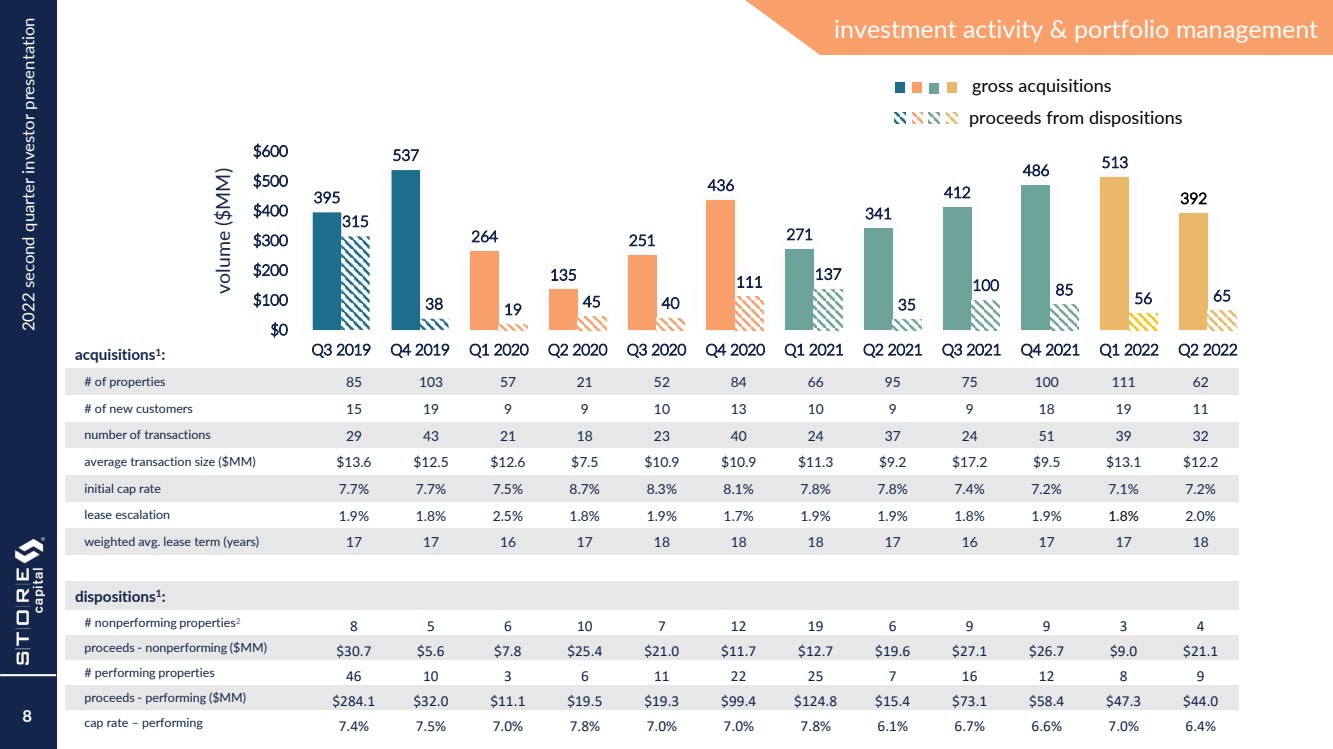

| ◾ | Invested $391.9 million in 62 properties at a weighted average initial cap rate of 7.2% |

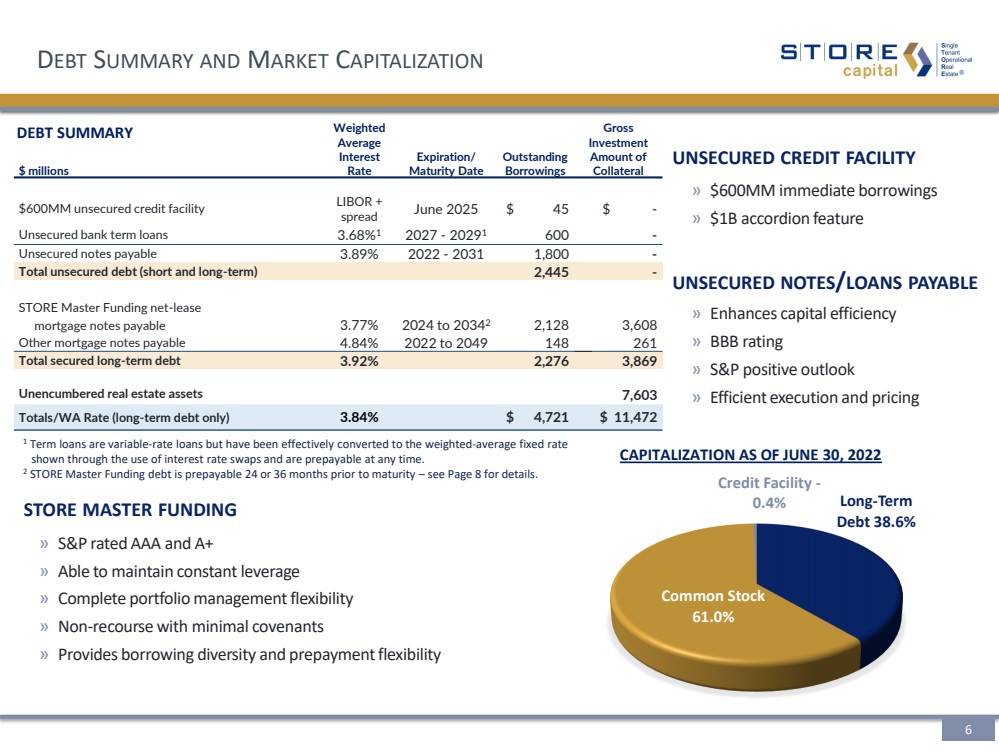

| ◾ | Closed on an aggregate $600 million of five-year ($400 million) and seven-year ($200 million) unsecured bank term debt at a weighted average interest rate of 3.68% |

| ◾ | Raised $83.4 million in net proceeds from the sale of approximately 3.1 million common shares under the Company’s at-the-market equity program |

For the six months ended June 30, 2022:

| ◾ | Total revenues of $445.9 million |

| ◾ | Net income of $177.5 million, or $0.64 per basic and diluted share, including an aggregate net gain of $19.7 million on dispositions of real estate |

| ◾ | AFFO of $321.6 million, or $1.16 per basic and diluted share |

| ◾ | Declared regular cash dividends per common share aggregating $0.770 |

| ◾ | Invested $904.4 million in 173 properties at a weighted average initial cap rate of 7.1% |

| ◾ | Raised $249.6 million in net proceeds from the sale of approximately 8.6 million common shares under the Company’s at-the-market equity program |

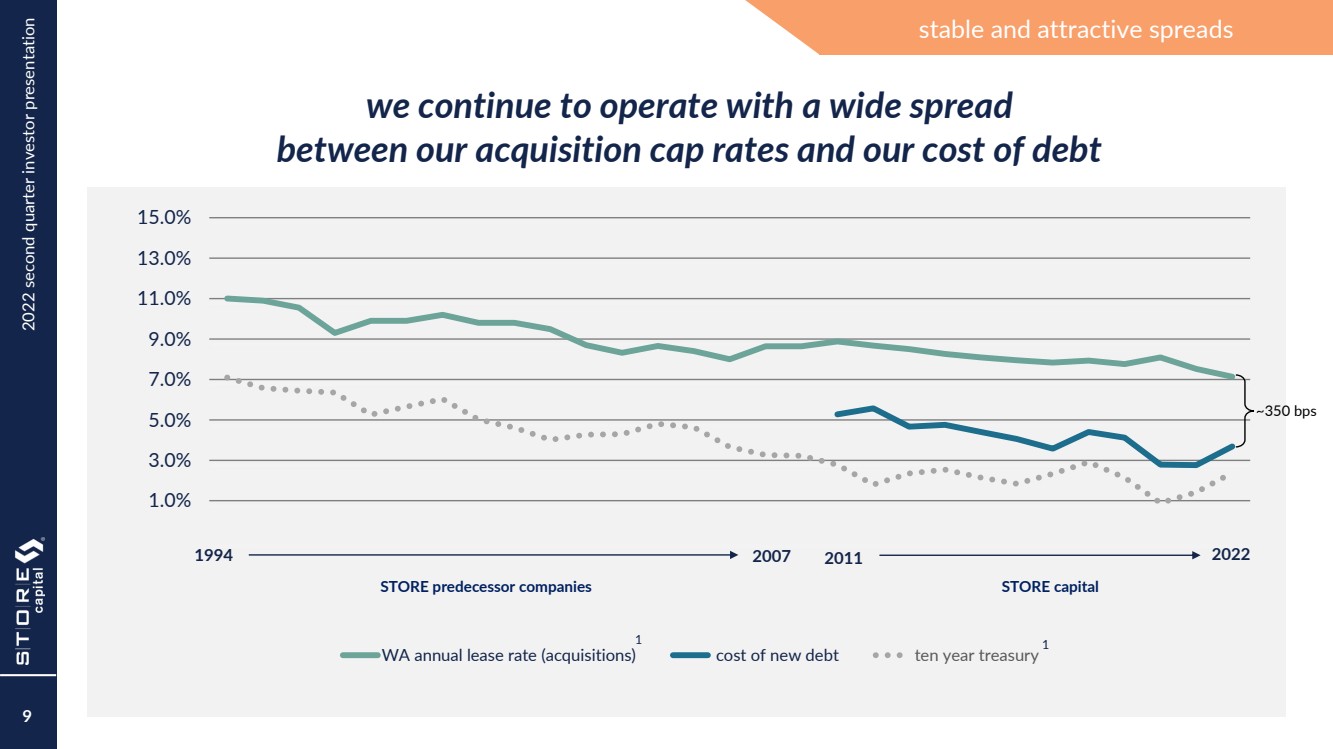

“Our momentum continued into the second quarter as we acquired $392 million in profit center real estate, while at the same time driving higher cap rates and lease escalations. We delivered strong revenue growth of 17% and a robust AFFO per share of $0.58. Our results were powered by our strong first half acquisition pace and the excellent performance of our portfolio,” said Mary Fedewa, STORE Capital’s President and Chief Executive Officer. “We address a very large market with our unique acquisition model and our financing flexibility allows us to optimize our cost of capital and maintain attractive spreads. As a result, we believe we can continue to deliver attractive risk-adjusted returns to our stakeholders in 2022 and beyond. Based on our