Welltower Inc. |

||||

34- | ||||

(State or other jurisdiction of incorporation) |

(Commission File Number) |

(IRS Employer Identification No.) | ||

Welltower OP Inc. |

||||

(State or other jurisdiction of incorporation) |

(Commission File Number) |

(IRS Employer Identification No.) | ||

(Address of principal executive offices) |

(Zip Code) |

Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

Item 2.02 |

Results of Operation and Financial Condition. |

Item 9.01 |

Financial Statements and Exhibits. |

| 99.1 | Business Update Presentation of Welltower Inc. dated May 10, 2022. | |

| 104 | Cover Page Interactive Data File – the cover page XBRL tags are embedded within the Inline XBRL document. | |

| WELLTOWER INC. | ||

| By: | /s/ Matthew McQueen | |

| Name: | Matthew McQueen | |

| Title: | Executive Vice President – General | |

| Counsel & Corporate Secretary | ||

| WELLTOWER OP INC. | ||

| By: | /s/ Matthew McQueen | |

| Name: | Matthew McQueen | |

| Title: | President | |

Exhibit 99.1

Business Update May 10, 2022 Welltower

Forward Looking Statements and Risk Factors This document contains “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. When Welltower uses words such as “may,” “will,” “intend,” “should,” “believe,” “expect,” “anticipate,” “project,” “pro forma,” “estimate” or similar expressions that do not relate solely to historical matters, Welltower is making forward-looking statements. Forward-looking statements, including statements related to Funds From Operations guidance, are not guarantees of future performance and involve risks and uncertainties that may cause Welltower’s actual results to differ materially from Welltower’s expectations discussed in the forward-looking statements. This may be a result of various factors, including, but not limited to: the impact of the COVID-19 pandemic; uncertainty regarding the implementation and impact of the CARES Act and future stimulus or other COVID-19 relief legislation; the status of the economy; the status of capital markets, including availability and cost of capital; issues facing the health care industry, including compliance with, and changes to, regulations and payment policies, responding to government investigations and punitive settlements and operators’/tenants’ difficulty in cost effectively obtaining and maintaining adequate liability and other insurance; changes in financing terms; competition within the health care and seniors housing industries; negative developments in the operating results or financial condition of operators/tenants, including, but not limited to, their ability to pay rent and repay loans; Welltower’s ability to transition or sell properties with profitable results; the failure to make new investments or acquisitions as and when anticipated; natural disasters and other acts of God affecting Welltower’s properties; Welltower’s ability to re-lease space at similar rates as vacancies occur; Welltower’s ability to timely reinvest sale proceeds at similar rates to assets sold; operator/tenant or joint venture partner bankruptcies or insolvencies; the cooperation of joint venture partners; government regulations affecting Medicare and Medicaid reimbursement rates and operational requirements; liability or contract claims by or against operators/tenants; unanticipated difficulties and/or expenditures relating to future investments or acquisitions; environmental laws affecting Welltower’s properties; changes in rules or practices governing Welltower’s financial reporting; the movement of U.S. and foreign currency exchange rates; Welltower’s ability to maintain its qualification as a REIT; key management personnel recruitment and retention; and other risks described in Welltower’s reports filed from time to time with the SEC. Welltower undertakes no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events or otherwise, or to update the reasons why actual results could differ from those projected in any forward-looking statements.

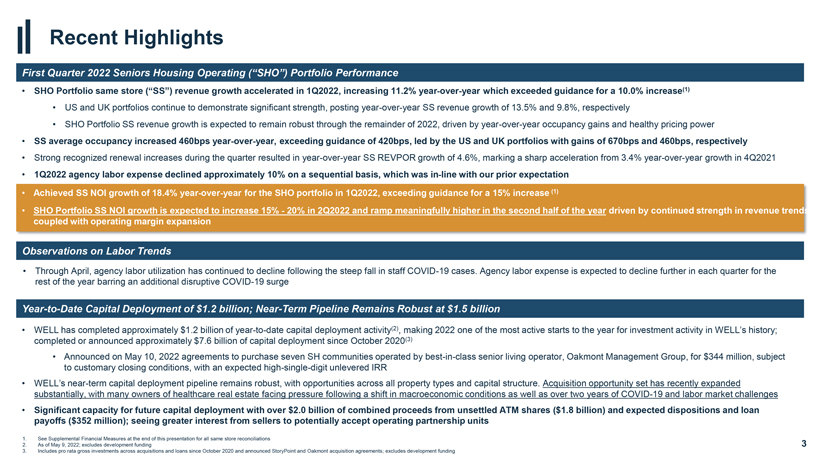

Recent Highlights First Quarter 2022 Seniors Housing Operating (“SHO”) Portfolio Performance • SHO Portfolio same store (“SS”) revenue growth accelerated in 1Q2022, increasing 11.2% year-over-year which exceeded guidance for a 10.0% increase(1) • US and UK portfolios continue to demonstrate significant strength, posting year-over-year SS revenue growth of 13.5% and 9.8%, respectively • SHO Portfolio SS revenue growth is expected to remain robust through the remainder of 2022, driven by year-over-year occupancy gains and healthy pricing power • SS average occupancy increased 460bps year-over-year, exceeding guidance of 420bps, led by the US and UK portfolios with gains of 670bps and 460bps, respectively • Strong recognized renewal increases during the quarter resulted in year-over-year SS REVPOR growth of 4.6%, marking a sharp acceleration from 3.4% year-over-year growth in 4Q2021 • 1Q2022 agency labor expense declined approximately 10% on a sequential basis, which was in-line with our prior expectation • Achieved SS NOI growth of 18.4% year-over-year for the SHO portfolio in 1Q2022, exceeding guidance for a 15% increase (1) • SHO Portfolio SS NOI growth is expected to increase 15%—20% in 2Q2022 and ramp meaningfully higher in the second half of the year driven by continued strength in revenue trends coupled with operating margin expansion Observations on Labor Trends • Through April, agency labor utilization has continued to decline following the steep fall in staff COVID-19 cases. Agency labor expense is expected to decline further in each quarter for the rest of the year barring an additional disruptive COVID-19 surge Year-to-Date Capital Deployment of $1.2 billion; Near-Term Pipeline Remains Robust at $1.5 billion • WELL has completed approximately $1.2 billion of year-to-date capital deployment activity(2), making 2022 one of the most active starts to the year for investment activity in WELL’s history; completed or announced approximately $7.6 billion of capital deployment since October 2020(3) • Announced on May 10, 2022 agreements to purchase seven SH communities operated by best-in-class senior living operator, Oakmont Management Group, for $344 million, subject to customary closing conditions, with an expected high-single-digit unlevered IRR • WELL’s near-term capital deployment pipeline remains robust, with opportunities across all property types and capital structure. Acquisition opportunity set has recently expanded substantially, with many owners of healthcare real estate facing pressure following a shift in macroeconomic conditions as well as over two years of COVID-19 and labor market challenges • Significant capacity for future capital deployment with over $2.0 billion of combined proceeds from unsettled ATM shares ($1.8 billion) and expected dispositions and loan payoffs ($352 million); seeing greater interest from sellers to potentially accept operating partnership units 1. See Supplemental Financial Measures at the end of this presentation for all same store reconciliations 2. As of May 9, 2022; excludes development funding 3 3. Includes pro rata gross investments across acquisitions and loans since October 2020 and announced StoryPoint and Oakmont acquisition agreements; excludes development funding

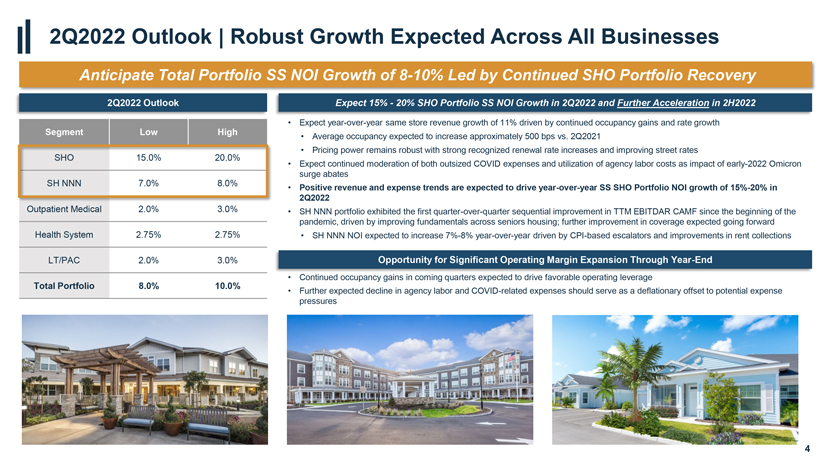

2Q2022 Outlook | Robust Growth Expected Across All Businesses Anticipate Total Portfolio SS NOI Growth of 8-10% Led by Continued SHO Portfolio Recovery 2Q2022 Outlook Segment Low High Outpatient Medical 2.0% 3.0% Health System 2.75% 2.75% LT/PAC 2.0% 3.0% Total Portfolio 8.0% 10.0% Expect 15%—20% SHO Portfolio SS NOI Growth in 2Q2022 and Further Acceleration in 2H2022 • Expect year-over-year same store revenue growth of 11% driven by continued occupancy gains and rate growth • Average occupancy expected to increase approximately 500 bps vs. 2Q2021 • Pricing power remains robust with strong recognized renewal rate increases and improving street rates • Expect continued moderation of both outsized COVID expenses and utilization of agency labor costs as impact of early-2022 Omicron surge abates • Positive revenue and expense trends are expected to drive year-over-year SS SHO Portfolio NOI growth of 15%-20% in 2Q2022 • SH NNN portfolio exhibited the first quarter-over-quarter sequential improvement in TTM EBITDAR CAMF since the beginning of the pandemic, driven by improving fundamentals across seniors housing; further improvement in coverage expected going forward • SH NNN NOI expected to increase 7%-8% year-over-year driven by CPI-based escalators and improvements in rent collections Opportunity for Significant Operating Margin Expansion Through Year-End • Continued occupancy gains in coming quarters expected to drive favorable operating leverage • Further expected decline in agency labor and COVID-related expenses should serve as a deflationary offset to potential expense pressures

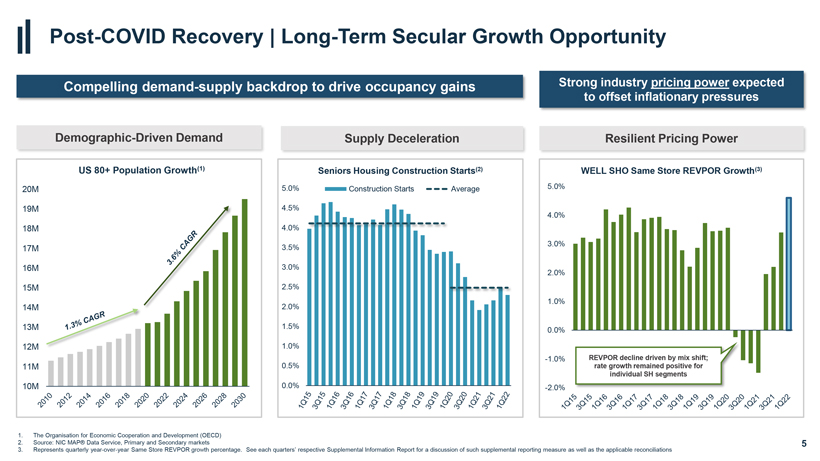

Post-COVID Recovery | Long-Term Secular Growth Opportunity Compelling demand-supply backdrop to drive occupancy gains Strong industry pricing power expected to offset inflationary pressures Demographic-Driven Demand US 80+ Population Growth(1) 20M 19M 18M 17M 16M 15M 14M 13M 12M 11M 10M 1. The Organisation for Economic Cooperation and Development (OECD) 2. Source: NIC MAP® Data Service, Primary and Secondary markets 3. Represents quarterly year-over-year Same Store REVPOR growth percentage. See each quarters’ respective Supplemental Information Report for a discussion of such supplemental reporting measure as well as the applicable reconciliations Supply Deceleration Seniors Housing Construction Starts(2) Construction Starts Average 5.0% 4.5% 4.0% 3.5% 3.0% 2.5% 2.0% 1.5% 1.0% 0.5% 0.0% Resilient Pricing Power WELL SHO Same Store REVPOR Growth(3) 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% -1.0% -2.0%

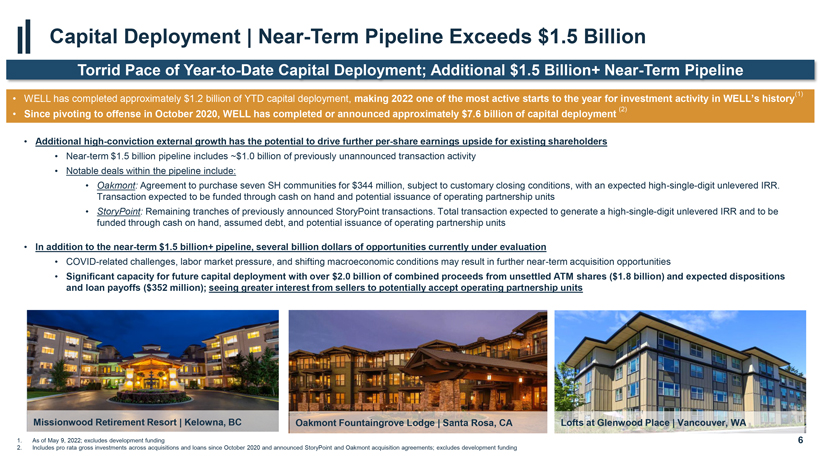

REVPOR decline driven by mix shift; rate growth remained positive for individual SH segments Capital Deployment | Near-Term Pipeline Exceeds $1.5 Billion Torrid Pace of Year-to-Date Capital Deployment; Additional $1.5 Billion+ Near-Term Pipeline (1) • WELL has completed approximately $1.2 billion of YTD capital deployment, making 2022 one of the most active starts to the year for investment activity in WELL’s history (2) • Since pivoting to offense in October 2020, WELL has completed or announced approximately $7.6 billion of capital deployment Additional high-conviction external growth has the potential to drive further per-share earnings upside for existing shareholders • Near-term $1.5 billion pipeline includes ~$1.0 billion of previously unannounced transaction activity • Notable deals within the pipeline include: • Oakmont: Agreement to purchase seven SH communities for $344 million, subject to customary closing conditions, with an expected high-single-digit unlevered IRR. Transaction expected to be funded through cash on hand and potential issuance of operating partnership units • StoryPoint: Remaining tranches of previously announced StoryPoint transactions. Total transaction expected to generate a high-single-digit unlevered IRR and to be funded through cash on hand, assumed debt, and potential issuance of operating partnership units • In addition to the near-term $1.5 billion+ pipeline, several billion dollars of opportunities currently under evaluation • COVID-related challenges, labor market pressure, and shifting macroeconomic conditions may result in further near-term acquisition opportunities • Significant capacity for future capital deployment with over $2.0 billion of combined proceeds from unsettled ATM shares ($1.8 billion) and expected dispositions and loan payoffs ($352 million); seeing greater interest from sellers to potentially accept operating partnership units Missionwood Retirement Resort | Kelowna, BCOakmont Fountaingrove Lodge | Santa Rosa, CA Lofts at Glenwood Place | Vancouver, WA 1. As of May 9, 2022; excludes development funding 2. Includes pro rata gross investments across acquisitions and loans since October 2020 and announced StoryPoint and Oakmont acquisition agreements; excludes development funding Oakmont Capriana | Brea, CA Wingate | Needham, MA Oakmont of Segovia | Palm Desert, CA 7 1. Includes pro rata gross investments across acquisitions and loans since January 1, 2022 through May 9, 2022; excludes development funding

Capital Deployment | Closed Transactions 2022 YTD

Capital Deployment Volume(1)

GROSS

$1.2B INVESTMENTS

? Initial yield of 5.1%

? Stable yield of 6.6%

? Blended high-single-digit unlevered IRR

ular & Off-Market Transactions

21 Total

Transactions(1)

22 OM and SH

Properties Acquired

2.7K Seniors Housing Units Acquired

ficant Discount to Replacement Cost

$269K / unit

Avg. Last Dollar Basis US and Canadian SH transactions

? Seniors housing acquisitions executed at an average investment of $48.9M per property

?

Located in highly attractive micro-markets

Seniors Housing Update

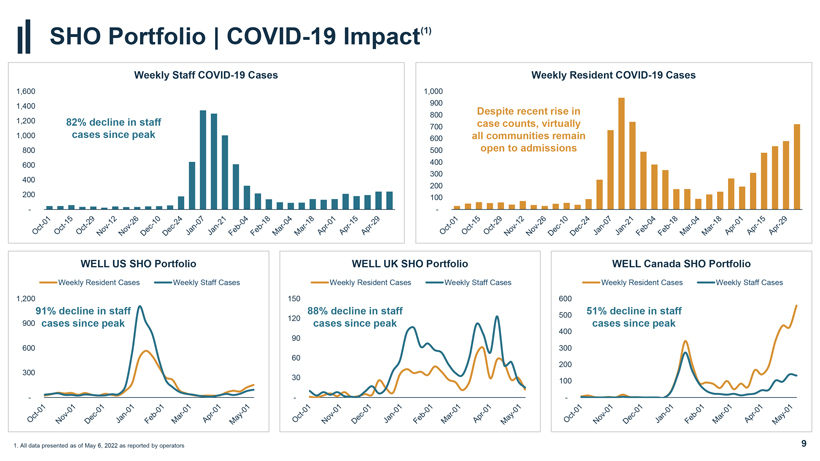

SHO Portfolio | COVID-19 Impact(1)

Weekly Resident COVID-19 Cases

1,000

900

800 Despite recent rise in 700 case counts, virtually 600 all communities remain 500 open

to admissions

400 300 200 100

-

1. All data presented as of May 6, 2022 as reported by operators

Weekly Staff COVID-19 Cases

82% decline in staff cases since peak

1,600 1,400 1,200 1,000 800 600 400 200

WELL US SHO Portfolio

Weekly Resident Cases Weekly Staff Cases

1,200

91% decline in staff 900 cases since peak

600

300

WELL UK SHO Portfolio

Weekly Resident Cases Weekly Staff Cases

88% decline in staff cases since peak

150 120 90 60 30

WELL Canada SHO Portfolio

Weekly Resident Cases Weekly Staff Cases

51% decline in staff cases since peak

600 500 400 300 200 100

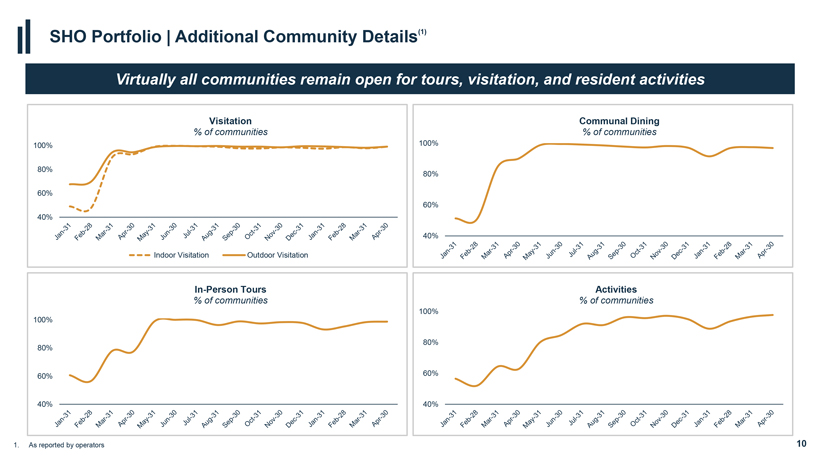

SHO Portfolio | Additional Community Details(1)

Virtually all communities remain open for tours, visitation, and resident activities

Visitation

% of communities

Communal Dining

% of communities

100% 80% 60% 40%

Indoor Visitation Outdoor Visitation

100% 80% 60% 40%

Activities

% of communities

100%

80%

60%

40%

100% 80% 60% 40%

In-Person Tours

% of communities

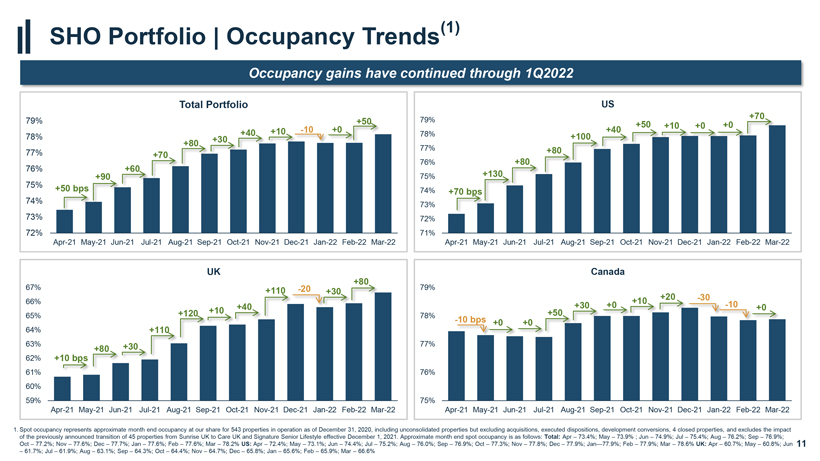

SHO Portfolio | Occupancy

Trends(1)

Occupancy gains have continued through 1Q2022

79%

78%

77% 76% 75% 74% 73% 72%

Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22

Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22

79% 78% 77% 76% 75% 74% 73% 72% 71%

67% 66% 65% 64% 63% 62% 61% 60% 59%

79% 78% 77% 76% 75%

Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22

1. Spot occupancy represents approximate month end occupancy at our share for 543 properties in operation as of

December 31, 2020, including unconsolidated properties but excluding acquisitions, executed dispositions, development conversions, 4 closed properties, and excludes the impact of the previously announced transition of 45 properties from Sunrise

UK to Care UK and Signature Senior Lifestyle effective December 1, 2021. Approximate month end spot occupancy is as follows: Total: Apr – 73.4%; May – 73.9% ; Jun – 74.9%; Jul – 75.4%; Aug – 76.2%; Sep – 76.9%; Oct

– 77.2%; Nov – 77.6%; Dec – 77.7%; Jan – 77.6%; Feb – 77.6%; Mar – 78.2% US: Apr – 72.4%; May – 73.1%; Jun – 74.4%; Jul – 75.2%; Aug – 76.0%; Sep – 76.9%; Oct – 77.3%; Nov –

77.8%; Dec – 77.9%; Jan—77.9%; Feb – 77.9%; Mar – 78.6% UK: Apr – 60.7%; May – 60.8%; Jun

– 61.7%; Jul – 61.9%; Aug –

63.1%; Sep – 64.3%; Oct – 64.4%; Nov – 64.7%; Dec – 65.8%; Jan – 65.6%; Feb – 65.9%; Mar – 66.6%

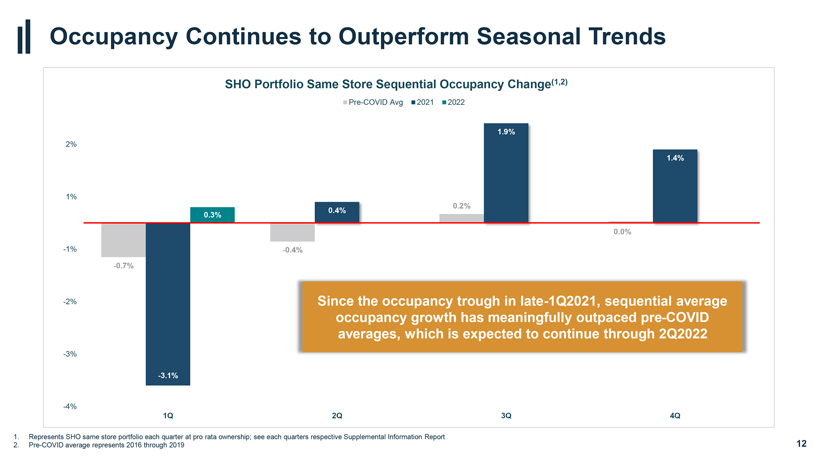

Occupancy Continues to Outperform Seasonal Trends

SHO Portfolio Same Store Sequential Occupancy Change(1,2)

Pre-COVID Avg 2021 2022

Since the

occupancy trough in late-1Q2021, sequential average occupancy growth has meaningfully outpaced pre-COVID averages, which is expected to continue through 2Q2022

1. Represents SHO same store portfolio each quarter at pro rata ownership; see each quarters respective Supplemental Information Report

2. Pre-COVID average represents 2016 through 2019

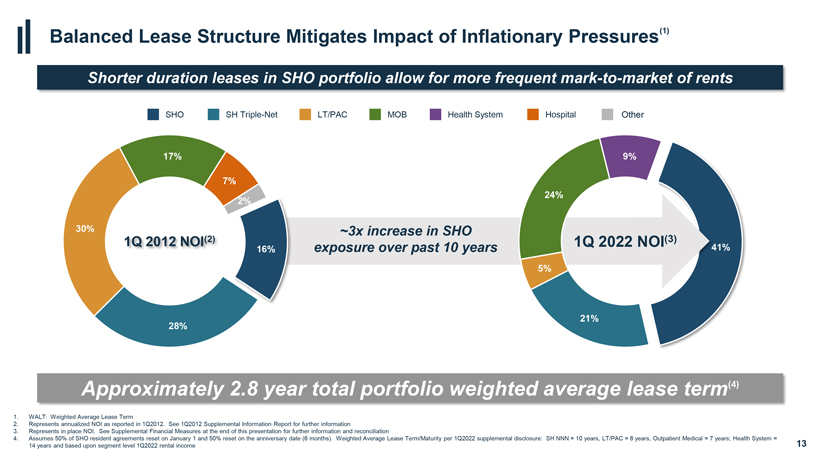

Approximately 2.8 year total portfolio weighted average lease term(4)

1. WALT: Weigh

2. Represents annualized NOI as

reported in 1Q2012. See 10May22 Q2 Supplemental 16:40

Information Report for furthr information

3. Represents in place

NOI. See Supplemental Financial Measures at the end of this presentation for further information and reconciliation

4. Assumes 50% of SHO resident agreements reset

on January 1 and 50% reset on the anniversary date (6 months). Weighted Average Lease Term/Maturity per 1Q2022 supplemental disclosure: SH NNN = 10 years, LT/PAC = 8 years, Outpatient Medical = 7 years; Health System =

14 years and based upon segment level 1Q2022 rental income 13

Balanced Lease Structure Mitigates Impact of Inflationary Pressures(1)

Shorter duration leases in SHO portfolio allow for more frequent mark-to-market of rents

SHO

SH Triple-Net

LT/PAC

MOB

Health System

Hospital

Life Other

1Q 2012 NOI(2)

~3x increase in SHO exposure over past 10 years

1Q 2022 NOI(3)

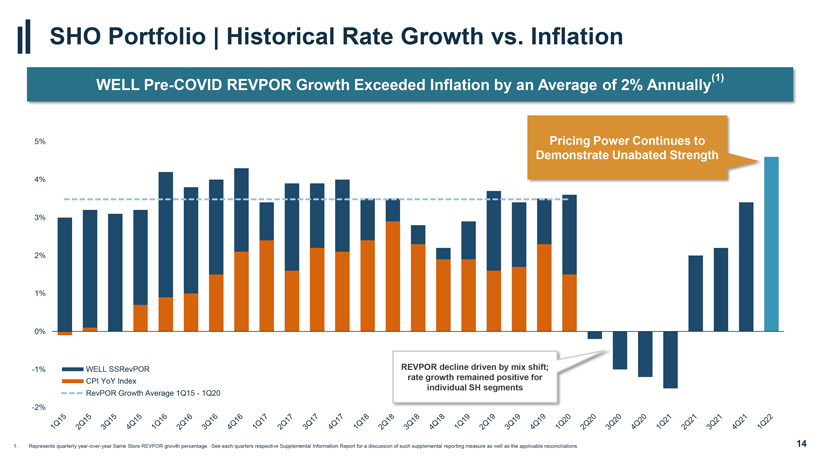

SHO Portfolio | Historical Rate Growth vs. Inflation

(1)

WELL Pre-COVID REVPOR Growth Exceeded Inflation by

an Average of 2% Annually

Pricing Power Continues to Demonstrate Unabated Strength

WELL SSRevPOR CPI YoY Index

RevPOR Growth Average 1Q15—1Q20

REVPOR decline driven by mix shift; rate growth remained positive for individual SH segments

1. Represents quarterly year-over-year Same Store REVPOR growth percentage. See each quarters respective Supplemental Information Report for a discussion of such supplemental reporting measure as well as the applicable reconciliations

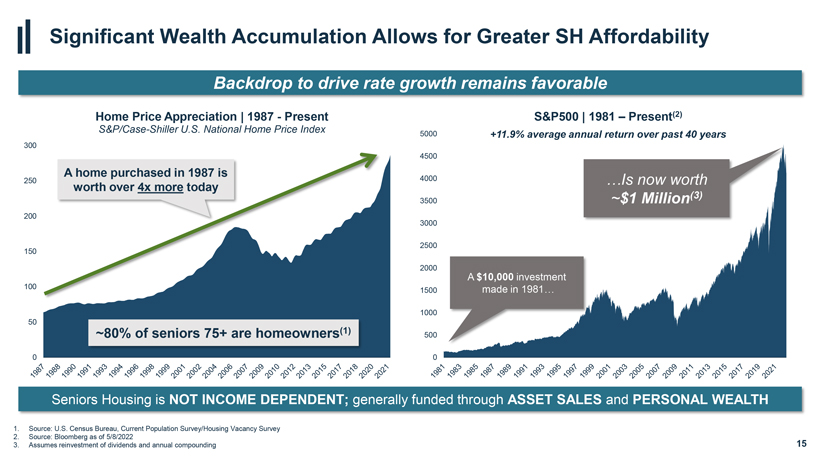

Seniors Housing is NOT INCOME DEPENDENT; generally funded through ASSET SALES and PERSONAL WEALTH

1. Source: U.S. Census Bureau, Current Population Survey/Housing Vacancy Survey

2. Source:

Bloomberg as of 5/8/2022

3. Assumes reinvestment of dividends and annual compounding 15

Significant Wealth Accumulation Allows for Greater SH Affordability

Backdrop to drive rate growth remains favorable

Home Price Appreciation | 1987—Present

S&P/Case-Shiller U.S. National Home Price Index

S&P500 | 1981 –

Present(2)

+11.9% average annual return over past 40 years

…Is now worth

~$1 Million(3)

~80% of seniors 75+ are homeowners(1)

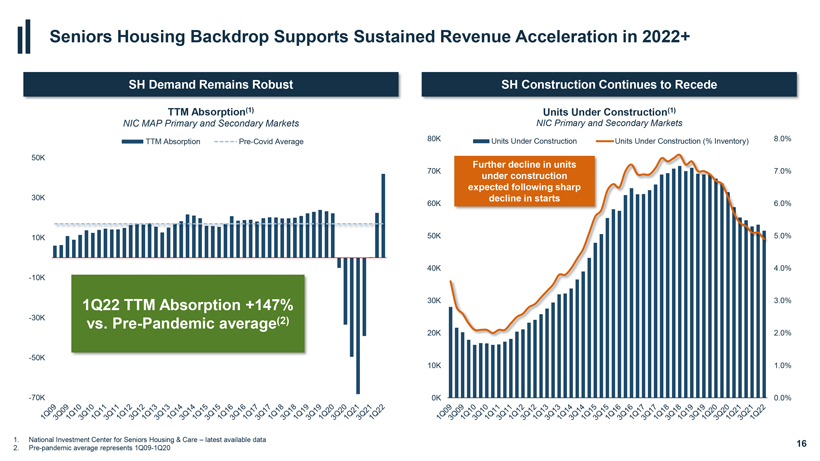

Seniors Housing Backdrop Supports Sustained Revenue Acceleration in 2022+

SH Demand Remains Robust

SH Construction Continues to Recede

TTM Absorption(1)

NIC MAP Primary and Secondary Markets

TTM Absorption Pre-Covid Average

Units Under Construction(1)

NIC Primary and Secondary Markets

Units Under Construction Units Under Construction (%

Inventory)

Further decline in units under construction expected following sharp decline in starts

1Q22 TTM Absorption +147% vs. Pre-Pandemic average(2)

50K 30K 10K -10K -30K -50K -70K

80K 70K 60K 50K 40K 30K 20K 10K

0K

8.0%

7.0%

6.0%

5.0%

4.0%

3.0%

2.0%

1.0%

0.0%

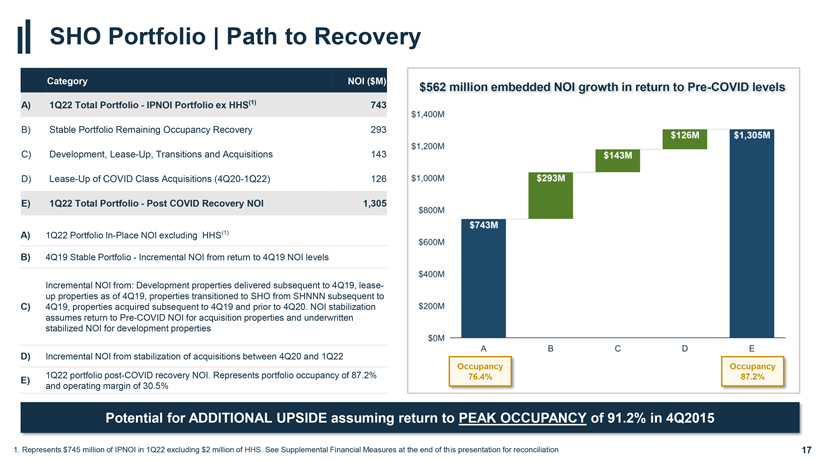

SHO Portfolio | Path to Recovery

Category NOI ($M)

A) 1Q22 Total Portfolio—IPNOI Portfolio ex HHS(1) 743

B) Stable Portfolio Remaining Occupancy Recovery 293 C) Development, Lease-Up, Transitions and Acquisitions 143 D) Lease-Up of COVID Class Acquisitions (4Q20-1Q22) 126

E) 1Q22 Total Portfolio—Post COVID Recovery NOI 1,305

A) 1Q22 Portfolio In-Place NOI excluding HHS(1)

B)

4Q19 Stable Portfolio—Incremental NOI from return to 4Q19 NOI levels

Incremental NOI from: Development properties delivered subsequent to 4Q19, lease-up properties as of 4Q19, properties transitioned to SHO from SHNNN subsequent to C) 4Q19, properties acquired subsequent to 4Q19 and prior to 4Q20. NOI stabilization assumes return to Pre-COVID NOI for acquisition properties and underwritten stabilized NOI for development properties

D) Incremental NOI from

stabilization of acquisitions between 4Q20 and 1Q22

1Q22 portfolio post-COVID recovery NOI. Represents portfolio occupancy of 87.2%

E) and operating margin of 30.5%

$562 million embedded NOI growth in return to Pre-COVID levels

Occupancy

76.4%

Occupancy

87.2%

Potential for ADDITIONAL UPSIDE assuming return to PEAK OCCUPANCY of 91.2% in 4Q2015

-001 Page 17

1. Represents $745 million of IPNOI in 1Q22 excluding $2 million of HHS. See Supplemental Financial Measures at the end of this presentation for reconciliation

Capital Deployment Update

Capital Deployment Since 4Q20

Capital Deployment Volume(1)

? Initial yield of 5.9%; Stable yield of approxima

tely 8.0%

GROSS ? Low last-dollar exposure and innovative structure offer downside protection

$7.6B INVESTMENTS ? Expected to generate high-single-digit to mid-teens unlevered IRRs to WELL

Granular & Off-Market Transactions

?

Predictive analytics and exclusive operator relationships used to execute off-market investments

77 Total Transactions ?

Maximizing risk-adjusted return to WELL through creative investments across the capital stack 297 OM and SH Properties Acquired ? Debt investments offer equity upside in form of warrants and/or bargain purchase options 30K Seniors Housing Units

Acquired ? Seniors housing acquisitions executed at an average investment of $22.0 million per property

Significant Discount to Replacement Cost

? Investments made at significant discount to replacement cost offer enhanced downside protection $195K / unit Avg. Last Dollar Basis US transactions ? Limited recent market

transactions priced above replacement cost serves to further curtail new supply 40K / unit Avg. Last Dollar Basis UK transactions

StoryPoint Fort Wayne | Fort Wayne, IN Oakmont PageIvy 19 Park at Otay Ranch | Chula Vista, CA

1. Includes pro rata gross investments across acquisitions and loans since October 2020 and announced StoryPoint and Oakmont acquisition agreements; excludes

development funding

HarborChase of Vero Beach | Vero Beach, FL

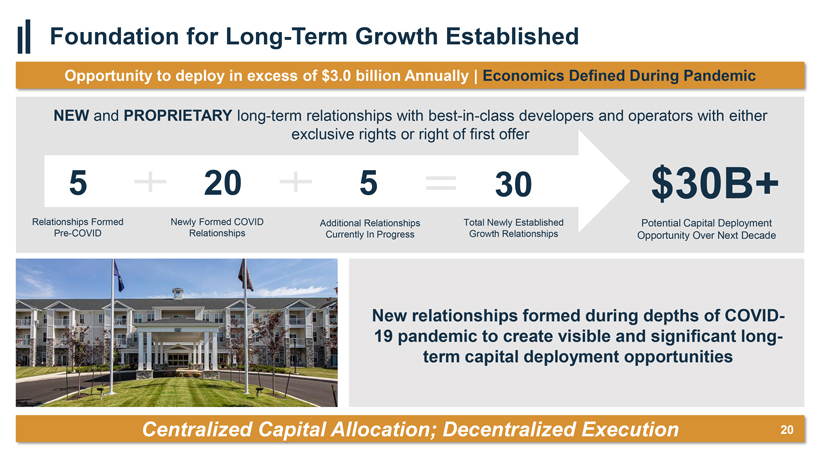

Foundation for Long-Term Growth Established

Opportunity to deploy in excess of $3.0 billion Annually | Economics Defined During Pandemic

NEW and PROPRIETARY long-term relationships with best-in-class developers and operators with either

exclusive rights or right of first offer

New relationships formed during depths of

COVID-19 pandemic to create visible and significant long-term capital deployment opportunities

Capital

Decentralized Execution

Relationships Formed Newly Formed COVID Additional Relationships Total Newly Established Potential Capital Deployment

Pre-COVID Relationships Currently In Progress Growth Relationships Opportunity Over Next Decade

Welltower Overview

World’s largest health & wellness real estate platform

Welltower at a Glance

Enterprise Value(1)

Dividend Yield(1)

125,000+

Seniors Housing & Wellness Housing Units

~23M sq. ft.

Outpatient Facilities

SHANKH MITRA TIMOTHY G. MCHUGH JOHN F. BURKART

Chief Executive Officer & Chief Financial Officer Chief Operating Officer Chief Investment Officer

MATTHEW G. MCQUEEN AYESHA MENON JOSHUA T. FIEWEGER

General Counsel & Senior Vice

President Chief Accounting Officer

Corporate Secretary Wellness

Housing & Development

Leadership Team

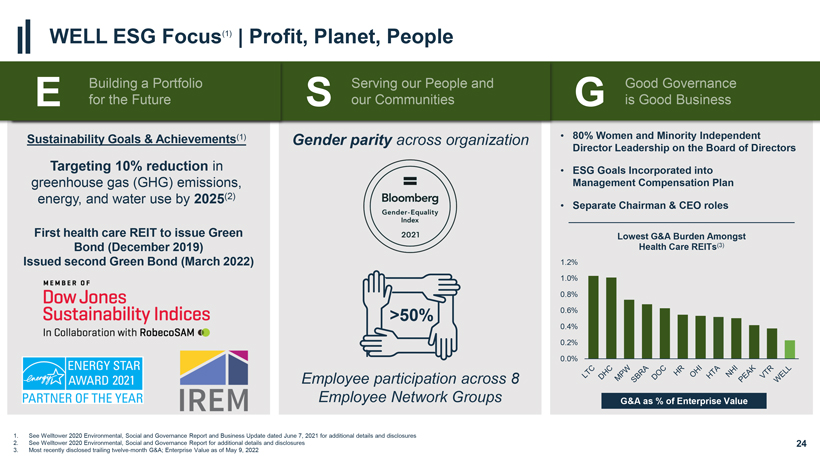

WELL ESG Focus(1) | Profit, Planet, People

Building a Portfolio Serving our People and E for the Future S our Communities

Sustainability

Goals & Achievements(1) Gender parity across organization

Targeting 10% reduction in greenhouse gas (GHG) emissions, energy, and water use by 2025(2)

First health care REIT to issue Green Bond (December 2019) Issued second Green Bond (March 2022)

>50%

Employee participation across 8

Employee Network Groups

Page 24

1. See Welltower 2020 Environmental, Social and Governance Report and Business Update dated June 7, 2021 for additional details and disclosures

2. See Welltower 2020 Environmental, Social and Governance Report for additional details and disclosures

3. Most recently disclosed trailing twelve-month G&A; Enterprise Value as of May 9, 2022

Good Governance

G is Good Business

• 80% Women and Minority Independent Director Leadership on the Board of Directors

•

ESG Goals Incorporated into Management Compensation Plan

• Separate Chairman & CEO roles

Lowest G&A Burden Amongst Health Care REITs(3)

1.2%

1.0%

0.8%

0.6%

0.4%

0.2%

0.0%

G&A as % of Enterprise Value

Drivers of Per Share Cash Flow Growth

SECULAR GROWTH Post-COVID fundamental recovery sustained by strong demographic trends, TAILWINDS shift to value-based health care, and social determinants of health

ACCRETIVE CAPITAL External growth strategy underpinned by value-oriented capital deployment DEPLOYMENT philosophy and data-driven decisions in innovative structures

DIVERSIFIED PLATFORM

Strongly aligned operating partners, positioned for significant growth

OF OPERATORS

STRONG INTERNAL

Entrepreneurial – Passionate – Diverse – Aligned

TALENT BASE

RISK Value-based investment philosophy and innovative structure of transactions offer MITIGANTS significant

downside protection Strong investment grade balance sheet and robust liquidity profile

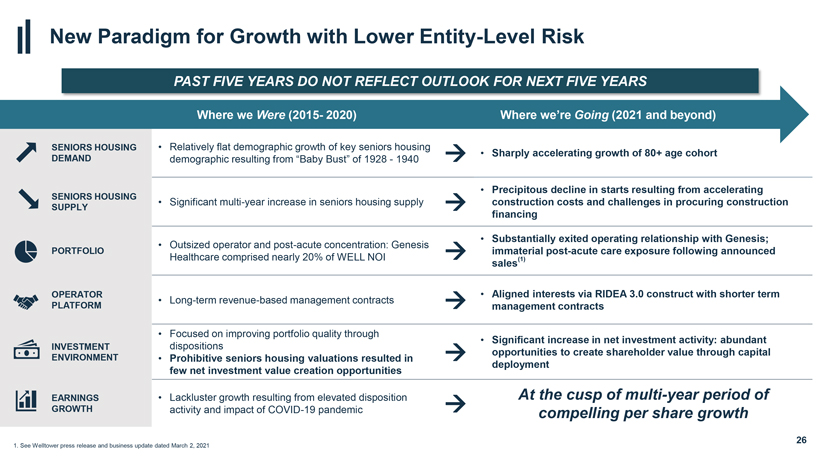

New Paradigm for Growth with Lower Entity-Level Risk

PAST FIVE YEARS DO NOT REFLECT OUTLOOK FOR NEXT FIVE YEARS

Where we Were (2015- 2020) Where

we’re Going (2021 and beyond)

SENIORS HOUSING • Relatively flat demographic growth of key seniors housing

• Sharply accelerating growth

of 80+ age cohort

DEMAND demographic resulting from “Baby Bust” of 1928—1940 ?

• Precipitous

decline in starts re

sulting from accelerating

SENIORS HOUSING

• Significant multi-year increase in seniors housing supply construction costs and challenges in procuring construction

SUPPLY ?

financing

•

ntially exited operating relationship with Genesis;

• Outsized operator and post-acute concentration: Genesis

PORTFOLIO ? immaterial

post-acute care exposure following announced

Healthcare comprised nearly 20% of WELL NOI (1)

sales

OPERATOR • Aligned interests via RIDEA 3.0 construct with shorter term

• Long-term revenue-based management contracts

PLATFORM ? management contracts

• Focused on improving portfolio quality through

• Significant

increase in net inve

stment activity: abundant

INVESTMENT dispositions

opportunities to create s

hareholder value through capital

ENVIRONMENT • Prohibitive seniors housing valuations resulted in ?

deployment

few net investment value creation opportunities

EARNINGS • Lackluster growth resulting

from elevated disposition At the cusp of multi-year period of

GROWTH activity and impact of COVID-19 pandemic ? compelling

per share growth

26

1. See Welltower press release and business update dated

March 2, 2021

Seniors Housing

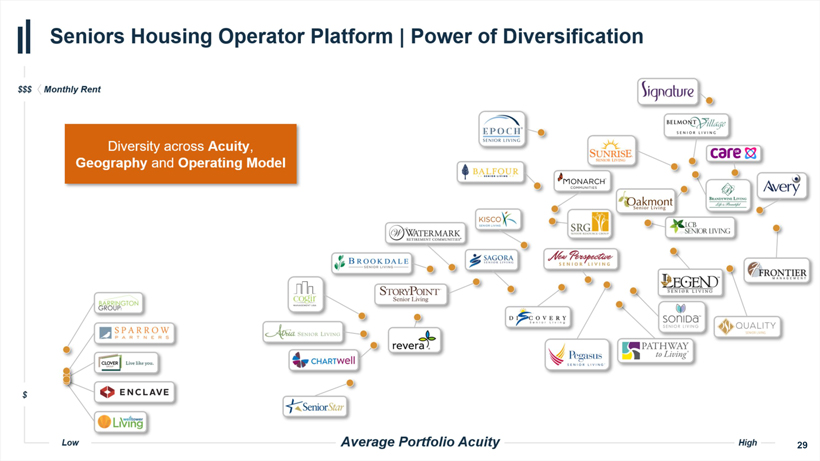

Seniors Housing Operator Platform | Power of Diversification

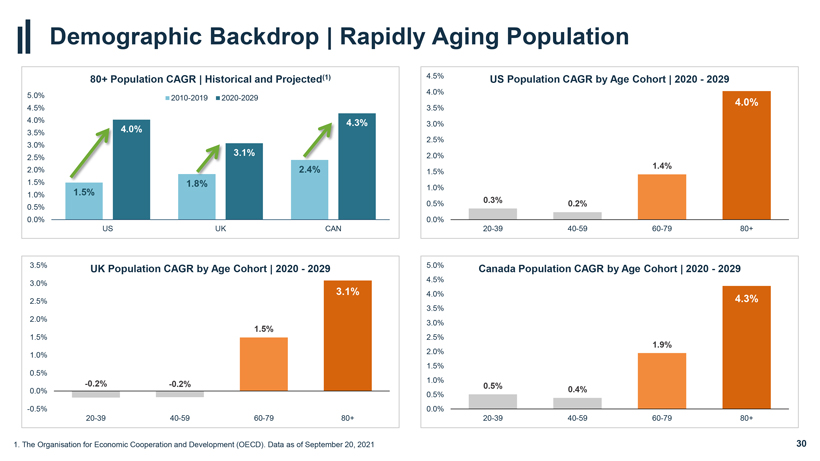

Demographic Backdrop | Rapidly Aging Population

1. The Organisation for Economic Cooperation and Development (OECD). Data as of September 20, 2021

80+ Population CAGR | Historical and Projected(1)

2010-2019 2020-2029

5.0%

4.5%

4.0%

3.5%

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

UK Population CAGR by Age Cohort | 2020—2029

3.5%

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0.0% -0.5%

-0.2%

-0.2%

1.

3.1%

US Population CAGR by Age Cohort | 2020—2029

0.3%

0.2%

1.4%

Canada Population CAGR by Age Cohort | 2020—2029

5.0%

4.5%

4.0%

3.5%

3.0%

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

0.5%

0.4%

1.9%

4.3%

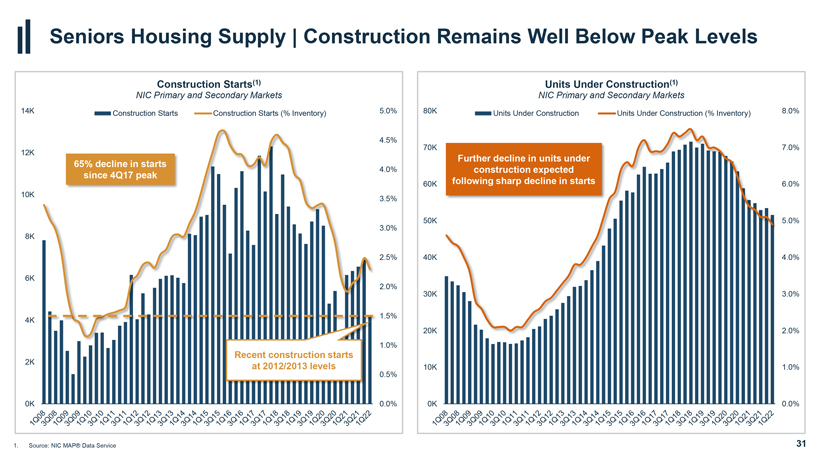

Seniors Housing Supply | Construction Remains Well Below Peak Levels

Construction Starts(1)

NIC Primary and Secondary Markets

Construction Starts Construction Starts (% Inventory)

65% decline in starts since 4Q17 peak

Recent construction starts at 2012/2013 levels

14K 12K 10K

8K 6K 4K 2K 0K

Units Under Construction(1)

NIC Primary and Secondary Markets

Units Under Construction Units Under Construction (%

Inventory)

Further decline in units under construction expected following sharp decline in starts

80K 70K 60K 50K 40K 30K 20K 10K

0K

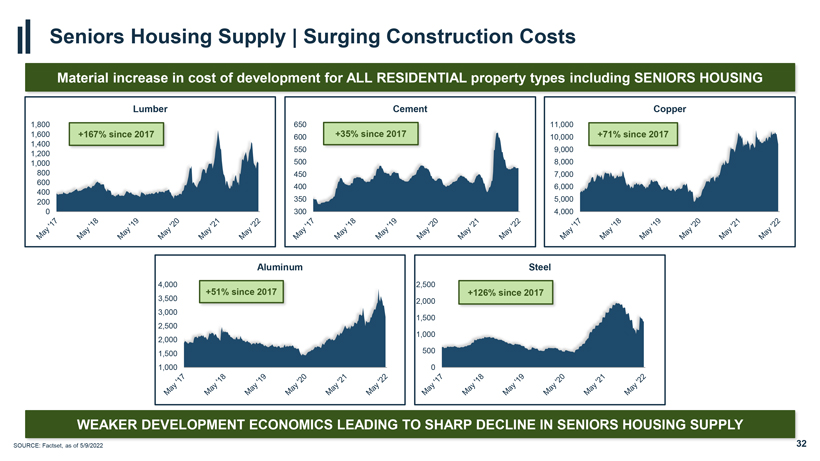

Seniors Housing Supply | Surging Construction Costs

Material increase in cost of development for ALL RESIDENTIAL property types including SENIORS HOUSING

1,800 1,600 1,400 1,200 1,000 800 600 400 200 0

+167% since 2017

Lumber

Cement

+35% since 2017

Copper

+71% since 2017

11,000 10,000 9,000 8,000 7,000 6,000 5,000 4,000

Aluminum

+51% since 2017

4,000 3,500 3,000 2,500 2,000 1,500 1,000

+126% since 2017

Steel

320796 WEAKER

-001 DEVELOPMENT 10May22 16:40 ECONOMICS PageLEADING 32

TO SHARP DECLINE IN SENIORS HOUSING SUPPLY

33

Balance Sheet Update

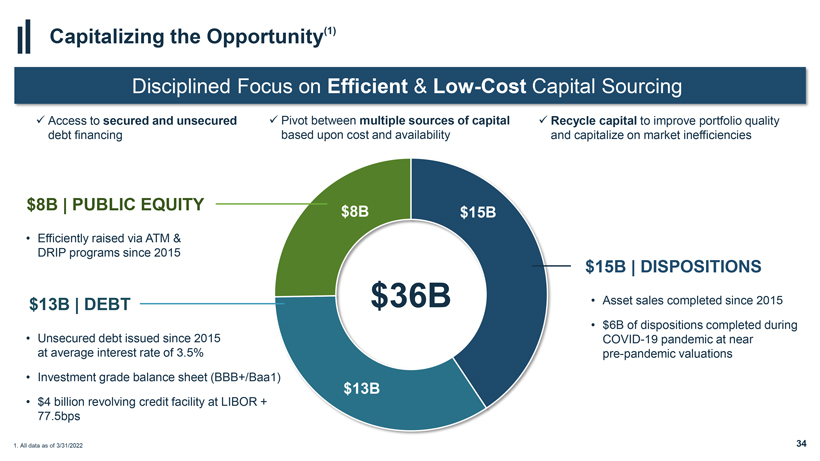

Capitalizing the Opportunity(1)

Disciplined Focus on Efficient & Low-Cost Capital Sourcing

? Access to secured and unsecured ? Pivot between multiple sources of capital ? Recycle capital to

improve portfolio quality debt financing based upon cost and availability and capitalize on market inefficiencies

$8B | PUBLIC EQUITY

$8B

• Efficiently raised via ATM &

DRIP programs since 2015

$15B | DISPOSITIONS

• Asset sales completed since 2015

• $6B of dispositions completed during COVID-19 pandemic at near pre-pandemic valuations

1. All data as of 3/31/2022

34

$13B | DEBT

• Unsecured debt issued since 2015 at average interest rate of 3.5%

• Investment

grade balance sheet (BBB+/Baa1)

• $4 billion revolving credit facility at LIBOR +

77.5bps

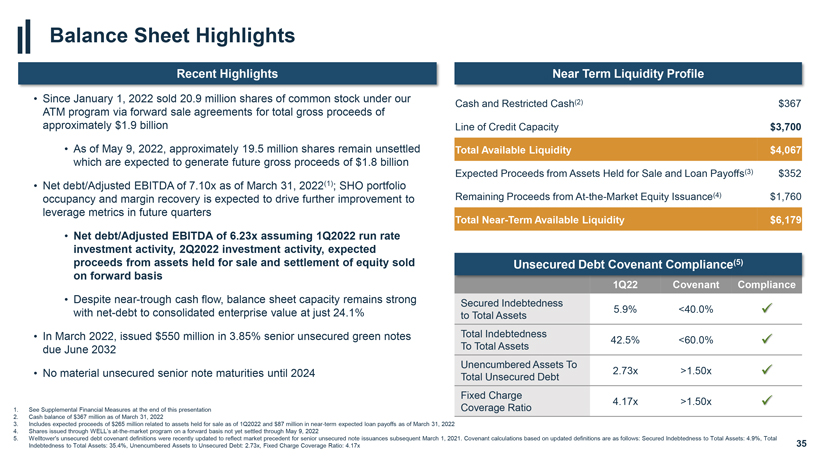

Balance Sheet Highlights

Recent Highlights

• Since January 1, 2022 sold 20.9 million

shares of common stock under our ATM program via forward sale agreements for total gross proceeds of approximately $1.9 billion

• As of May 9, 2022,

approximately 19.5 million shares remain unsettled which are expected to generate future gross proceeds of $1.8 billion

• Net debt/Adjusted EBITDA

of 7.10x as of March 31, 2022(1); SHO portfolio occupancy and margin recovery is expected to drive further improvement to leverage metrics in future quarters

• Net debt/Adjusted EBITDA of 6.23x assuming 1Q2022 run rate investment activity, 2Q2022 investment activity, expected proceeds from assets held for sale and

settlement of equity sold on forward basis

• Despite near-trough cash flow, balance sheet capacity remains strong with

net-debt to consolidated enterprise value at just 24.1%

• In March 2022, issued $550 million in 3.85% senior

unsecured green notes due June 2032

• No material unsecured senior note maturities until 2024

Near Term Liquidity Profile

Cash and Restricted Cash(2) $367 Line of Credit Capacity $3,700

Total Available Liquidity $4,067

Expected Proceeds from Assets Held for Sale and Loan Payoffs(3) $352

Remaining Proceeds from At-the-Market Equity Issuance(4) $1,760

Total Near-Term Available Liquidity $6,179

Unsecured Debt Covenant Compliance(5)

1Q22 Covenant Compliance

Secured Indebtedness

5.9% <40.0% ? to Total Assets Total Indebtedness

42.5% <60.0% ? To Total Assets

Unencumbered Assets To

2.73x >1.50x ? Total Unsecured Debt Fixed Charge

4.17x >1.50x ? Coverage Ratio

4.17x >1.50x ?

1. See Supplemental Financial Measures at the end of this presentation Coverage Ratio

2. Cash

balance of $367 million as of March 31, 2022

3. Includes expected 320796 proceeds - 001 of

$265 million related to assets 10May22 held for sale as 16:40 of Q2

22 and $87 million inPage n r-term expected 35 loan payoffs as of March 31, 2022

4. Shares issued through WELL’s at-the-market program on a forward basis not yet settled

through May 9, 2022

5. Welltower’s unsecured debt covenant definitions were recently updated to reflect market precedent for senior unsecured note

issuances subsequent March 1, 2021. Covenant calculations based on updated definitions are as follows: Secured Indebtedness to Total Assets: 4.9%, Total Indebtedness to Total Assets: 35.4%, Unencumbered Assets to Unsecured Debt: 2.73x, Fixed

Charge Coverage Ratio: 4.17x

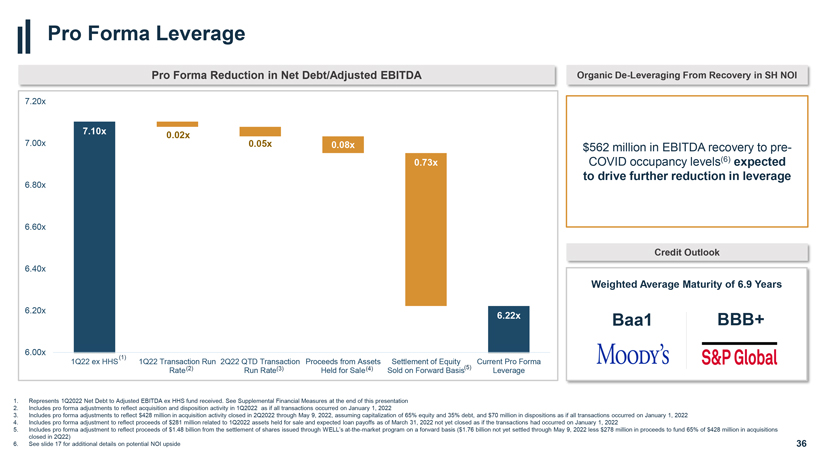

Pro Forma Leverage

Pro

Forma Reduction in Net Debt/Adjusted EBITDA

1Q22 ex HHS

1Q22 Transaction Run

2Q22 QTD Transaction

Proceeds from Assets

Settlement of Equity

Current Pro Forma

Rate(2)

Run Rate(3)

Held for Sale(4)

Sold on Forward Basis(5)

Leverage

1. Represents 1Q2022 Net Debt to Adjusted EBITDA ex HHS fund received. See

Supplemental Financial Measures at the end of this presentation

2. Includes pro forma adjustments to reflect acquisition and disposition activity in 1Q2022 as if

all transactions occurred on January 1, 2022

3. Includes pro forma adjustments to reflect $428 million in acquisition activity closed in 2Q2022 through

May 9, 2022, assuming capitalization of 65% equity and 35% debt, and $70 million in dispositions as if all transactions occurred on January 1, 2022

4. Includes proforma adjustment to reflect proceeds of

$28 million related to Q2 22 assets held for sale and loan payoffs as of March 31, 2022 not yet closed as if the transactions had occurred on

January 1, 2022

5. Includes pro forma adjustment to reflect proceeds of $1.48 billion from the settlement of shares issued through WELL’s at-the-market program on a forward basis ($1.76 billion not yet settled through May 9, 2022 less $278 million in proceeds to fund 65% of $428 million in

acquisitions

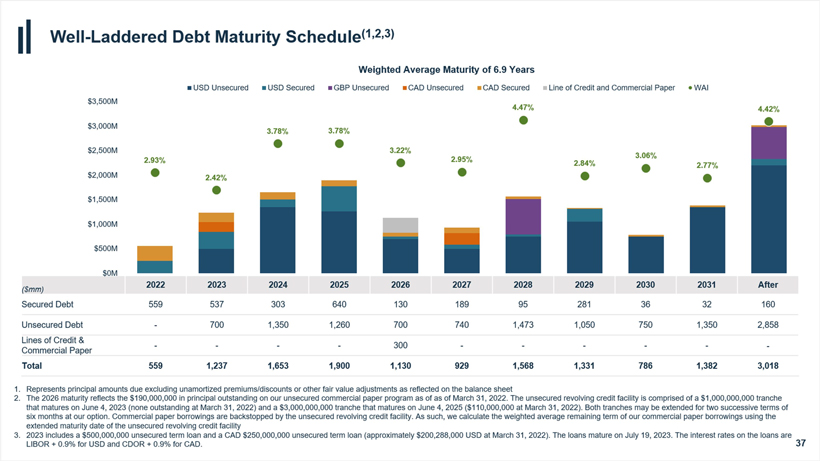

Weighted Average Maturity of 6.9 Years

Baa1 BBB+

closed in 2Q22)

6. See slide 17 for additional details on potential NOI upside

1. Represents principal amounts

due excluding unamortized premiums/discounts or other fair value adjustments as reflected on the balance sheet

2. The 2026 maturity reflects the $190,000,000 in

principal outstanding on our unsecured commercial paper program as of as of March 31, 2022. The unsecured revolving credit facility is comprised of a $1,000,000,000 tranche

that matures on June 4, 2023 (none outstanding at March 31, 2022) and a $3,000,000,000 tranche that matures on June 4, 2025 ($110,000,000 at March 31, 2022).

Both tranches may be extended for two successive terms of

six months at our option. Commercial paper borrowings are backstopped by the unsecured revolving credit

facility. As such, we calculate the weighted average remaining term of our commercial paper borrowings using the

extended maturity date of the unsecured revolving

credit facility

3. 2023 includes a $500,000,000 unsecured term loan and a CAD $250,000,000 unsecured term loan (approximately $200,288,000 USD at March 31,

2022). The loans mature on July 19, 2023. The interest rates on the loans are

LIBOR + 0.9% for USD and CDOR + 0.9% for CAD.

38

Supplemental Financial Measures

Non-GAAP Financial Measures

We believe that revenues, net income and net income attributable to common stockholders (“NICS”), as defined by U.S. generally accepted accounting principles (“U.S.

GAAP”), are the most appropriate earnings measurements. However, we consider Net Operating Income (“NOI”), In-Place NOI (“IPNOI”), Same Store NOI (“SSNOI”), REVPOR and Same

Store REVPOR (“SS REVPOR”), EBITDA and Adjusted EBITDA to be useful supplemental measures of our operating performance. Excluding EBITDA and Adjusted EBITDA these supplemental measures are disclosed on our pro rata ownership basis.

Pro rata amounts are derived by reducing consolidated amounts for minority partners’ noncontrolling ownership interests and adding our minority ownership

share of unconsolidated amounts. We do not control unconsolidated investments. While we consider pro rata disclosures useful, they may not accurately depict the legal and economic implications of our joint venture arrangements and should be used

with caution.

Our supplemental reporting measures and similarly entitled financial measures are widely used by investors, equity and debt analysts and rating

agencies in the valuation, comparison, rating and investment recommendations of companies. Our management uses these financial measures to facilitate internal and external comparisons to historical operating results and in making operating

decisions. Additionally, these measures are utilized by the Board of Directors to evaluate management.

None of the supplemental reporting measures represent net

income or cash flow provided from operating activities as determined in accordance with U.S. GAAP and should not be considered as alternative measures of profitability or liquidity. Finally, the supplemental reporting measures, as defined by us, may

not be comparable to similarly entitled items reported by other real estate investment trusts or other companies. Multi-period amounts may not equal the sum of the individual quarterly amounts due to rounding.

39

NOI, IPNOI, SSNOI, REVPOR & SS REVPOR

We define NOI as total revenues, including tenant reimbursements, less property operating expenses. Property operating expenses represent costs associated with managing,

maintaining and servicing tenants for our properties. These expenses include, but are not limited to, property-related payroll and benefits, property management fees paid to operators, marketing, housekeeping, food service, maintenance, utilities,

property taxes and insurance. General and administrative expenses represent costs unrelated to property operations and transaction costs. These expenses include, but are not limited to, payroll and benefits, professional services, office expenses

and depreciation of corporate fixed assets.

IPNOI represents NOI excluding interest income, other income and non-IPNOI and

adjusted for timing of current quarter portfolio changes such as acquisitions, development conversions, segment transitions, dispositions and investments held for sale.

SSNOI is used to evaluate the operating performance of our properties using a consistent

population which controls for changes in the composition of our portfolio. As used herein, same store is generally defined as those revenue-generating properties

in the portfolio for the relevant year-over-year reporting periods. Land parcels, loans and sub-leases as well as any properties acquired, developed/redeveloped (including major refurbishments where 20% or

more of units are simultaneously taken out of commission for 30 days or more), sold or classified as held for sale during that period are excluded from the same store amounts. Properties undergoing operator and/or segment transitions (except Seniors

Housing Triple-net to Seniors Housing Operating with the same operator) are also excluded from same store amounts. Normalizers include adjustments that in management’s opinion are appropriate in

considering SSNOI, a supplemental, non-GAAP performance measure. None of these adjustments, which may increase or decrease SSNOI, are reflected in our financial statements prepared in accordance with U.S.

GAAP. Significant normalizers (defined as any that individually exceed 0.50% of SSNOI growth per property type) are separately disclosed and explained in the relevant supplemental reporting package. No reconciliation of the forecasted range for

SSNOI on a combined basis or by property type is included in this release because we are unable to quantify certain amounts that would be required to be included in the comparable GAAP financial measure without unreasonable efforts, as we believe

such reconciliation would imply a degree of precision that could be confusing or misleading to investors.

No reconciliation of the forecasted range for SSNOI on a

combined basis or by property type is included in this release because we are unable to quantify certain amounts that would be required to be included in the comparable GAAP financial measure without unreasonable efforts, and we believe such

reconciliation would

imply a degree of precision that could be confusing or misleading to investors.

REVPOR represents the average revenues generated per occupied room per month at our seniors housing operating properties. It is calculated as our pro rata version of total resident

fees and services revenues from the income statement divided by average monthly occupied room days. SS REVPOR is used to evaluate the REVPOR performance of our properties under a consistent population which eliminates changes in the composition of

our portfolio. It is based on the same pool of properties used for SSNOI and includes any revenue normalizations used for SSNOI. We use REVPOR and SS REVPOR to evaluate the revenue-generating capacity and profit potential of its seniors housing

operating portfolio independent of fluctuating occupancy rates. They are also used in comparison against industry and competitor statistics, if known, to evaluate the quality of our seniors housing operating portfolio.

We believe NOI, IPNOI, SSNOI, REVPOR and SS REVPOR provide investors relevant and useful information because they measure the operating performance of our properties at the

property level on an unleveraged basis. We use these metrics to make decisions about resource allocations and to assess the property level performance of our properties.

40

In-Place NOI Reconciliations

(1) Represents Welltower’s interest in joint ventures where Welltower is the minority partner.

(2) Represents minority partner’s interest in joint ventures where Welltower is the majority partner and includes an adjustment to remove NOI related to a leasehold portfolio

interest for 26

properties assumed by a wholly-owned affiliate in conjunction with the Holiday Retirement transaction. Subsequent to the initial transaction, we

purchased eight of the leased properties and one of the properties was sold by the landlord and removed from the lease. No rent will be paid in excess of net cash flows relating to the leasehold properties.

(3) Excludes amounts recognized in other income related to the Health and Human Services Provider Relief Fund in the US and similar programs in the UK and Canada.

(4) Primarily includes development properties and land parcels.

(5) Primarily represents non-cash NOI

(6) Represents timing adjustments for current quarter acquisitions, construction conversions and segment or operator transitions.

41

(dollars in thousands)

Net income (loss)

Loss (gain) on real estate dispositions, net

Loss (income) from unconsolidated entities

Income tax expense (benefit)

Other expenses

Provision for loan losses, net

Loss (gain) on extinguishment of debt, net

Loss (gain) on derivatives and financial

instruments, net

General and administrative expenses

Depreciation and

amortization

Interest expense

Consolidated net operating income

NOI attributable to unconsolidated investments(1)

NOI attributable to noncontrolling

interests(2)

Pro rata net operating income (NOI)

Adjust:

Interest income

Other income(3)

Sold / held for sale

Non operational(4)

Non In-Place NOI(5)

Timing adjustments(6)

In-Place NOI

Annualized

In-Place NOI

In-Place NOI by property type

Seniors Housing Operating $ Seniors Housing Triple-Net Outpatient Medical Health System Long-Term/Post-Acute Care Total In-Place NOI $

1Q22 $ 65,751 (22,934) 2,884 5,013 26,069 (804) (12) 2,578 37,706 304,088 121,696 542,035 20,142 (34,999) 527,178

(39,673) (11,133) (2,804) 1,053 (21,668) 3,384 456,337 $ 1,825,348

1Q22 % of Total

745,316 41 % 383,528 21 % 434,884 24 %

172,368 9 % 89,252 5 % 1,825,348 100 %

1. Represents Welltower’s interests in joint ventures where Welltower is the minority partner.

2. Represents minority partners’ interests in joint ventures where Welltower is the majority partner and includes an adjustment to remove NOI related to

certain leasehold properties.

3. Represents SHO revenues at Welltower pro rata ownership.

4. Includes where appropriate adjustments to reflect consistent property ownership percentages, to translate Canadian properties at a USD/CAD rate of 1.2684 and to translate UK

properties at a GBP/USD rate of 1.38.

5. Represents SS SHO revenues at Welltower pro rata ownership.

6. Represents average occupied units for SS properties on a pro

rata basis.

7. Represents pro rata SS average revenues generated

per occupied room per month.

42

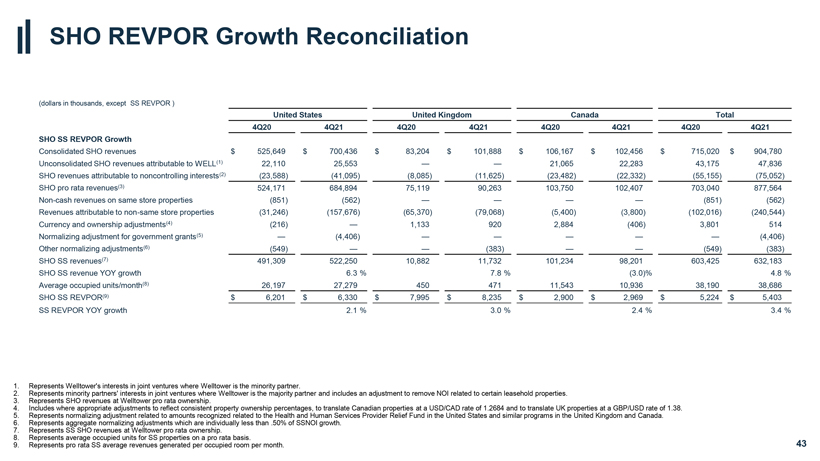

SHO REVPOR Growth Reconciliation

(dollars in thousands, except SS REVPOR )

SHO SS REVPOR Growth

Consolidated SHO revenues

Unconsolidated SHO revenues attributable to WELL(1) SHO revenues

attributable to noncontrolling interests(2) SHO pro rata revenues(3) Non-cash revenues on same store properties Revenues attributable to non-same store properties

Currency and ownership adjustments(4) SHO SS revenues(5) SHO SS revenue YOY growth Average occupied units/month(6) SHO SS REVPOR(7) SS REVPOR YOY growth

United

States United Kingdom Canada Total

1Q21 1Q22 1Q21 1Q22 1Q21 1Q22 1Q21 1Q22

SHO REVPOR Growth Reconciliation

1. Represents Welltower’s interests in joint ventures where Welltower is the minority partner.

2. Represents minority partners’ interests in joint ventures where Welltower is the majority partner and includes an adjustment to remove NOI related to certain leasehold

properties.

3. Represents SHO revenues at Welltower pro rata ownership.

4.

Includes where appropriate adjustments to reflect consistent property ownership percentages, to translate Canadian properties at a USD/CAD rate of 1.2684 and to translate UK properties at a GBP/USD rate of 1.38.

5. Represents normalizing adjustment related to amounts recognized related to the Health and Human Services Provider Relief Fund in the United States and similar programs in the

United Kingdom and Canada.

6. Represents aggregate normalizing adjustments which are individually less than .50% of SSNOI growth

7. Represents SS SHO revenues at Welltower pro rata ownership.

8. Represents average occupied

units for SS properties on a pro rata basis.

9. Represents pro rata SS average revenues generated per occupied room per month. 43

(dollars in thousands, except SS REVPOR )

SHO SS REVPOR Growth

Consolidated SHO revenues

Unconsolidated SHO revenues attributable to WELL(1) SHO revenues

attributable to noncontrolling interests(2) SHO pro rata revenues(3) Non-cash revenues on same store properties Revenues attributable to non-same store properties

Currency and ownership adjustments(4) Normalizing adjustment for government grants(5) Other normalizing adjustments(6) SHO SS revenues(7) SHO SS revenue YOY growth Average occupied units/month(8) SHO SS REVPOR(9) SS REVPOR YOY growth

United States United Kingdom Canada Total

4Q20 4Q21 4Q20 4Q21 4Q20 4Q21 4Q20 4Q21

$ 525,649 $ 700,436 $ 83,204 $ 101,888 $ 106,167 $ 102,456 $ 715,020 $ 904,780 22,110 25,553 — — 21,065 22,283 43,175 47,836 (23,588) (41,095) (8,085) (11,625) (23,482)

(22,332) (55,155) (75,052) 524,171 684,894 75,119 90,263 103,750 102,407 703,040 877,564 (851) (562) — — — — (851) (562) (31,246) (157,676) (65,370) (79,068) (5,400) (3,800) (102,016) (240,544) (216) — 1,133 920 2,884 (406)

3,801 514

— (4,406) — — — — — (4,406) (549) — — (383) — — (549) (383) 491,309 522,250 10,882 11,732 101,234

98,201 603,425 632,183

6.3 % 7.8 % (3.0)% 4.8 % 26,197 27,279 450 471 11,543 10,936 38,190 38,686 $ 6,201 $ 6,330 $ 7,995 $ 8,235 $ 2,900 $ 2,969 $

5,224 $ 5,403

2.1 % 3.0 % 2.4 % 3.4 %

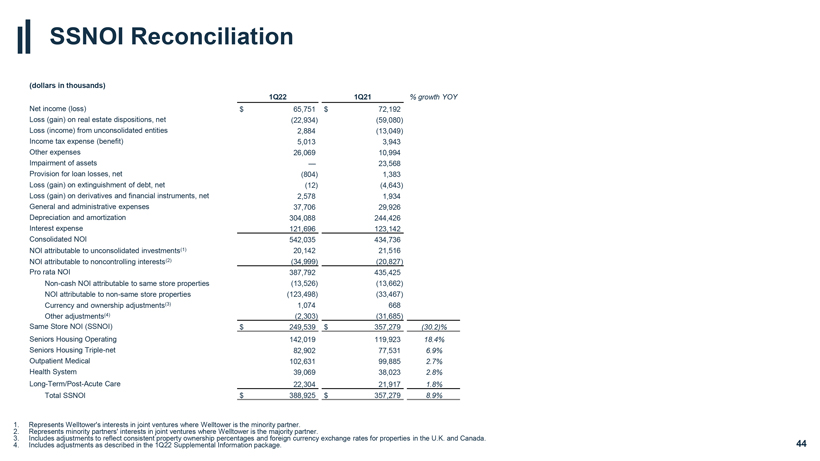

SSNOI Reconciliation

(dollars in thousands)

Net income (loss)

Loss (gain) on real estate dispositions, net Loss (income) from unconsolidated entities Income tax expense (benefit) Other expenses Impairment of assets Provision for loan losses,

net Loss (gain) on extinguishment of debt, net

Loss (gain) on derivatives and financial instruments, net General and administrative expenses Depreciation and

amortization Interest expense Consolidated NOI

NOI attributable to unconsolidated investments(1) NOI attributable to noncontrolling interests(2) Pro rata NOI

Non-cash NOI attributable to same store properties NOI attributable to non-same

store properties Currency and ownership adjustments(3) Other adjustments(4) Same Store NOI (SSNOI) Seniors Housing Operating Seniors Housing

Triple-net Outpatient Medical Health System Long-Term/Post-Acute Care Total SSNOI

1Q22 $ 65,751 (22,934) 2,884 5,013 26,069

—

(804) (12) 2,578 37,706 304,088 121,696 542,035 20,142 (34,999)

387,792 (13,526) (123,498) 1,074 (2,303) $ 249,539 142,019 82,902 102,631 39,069 22,304 $ 388,925

1Q21 % growth YOY $ 72,192 (59,080) (13,049) 3,943 10,994

23,568 1,383 (4,643) 1,934 29,926 244,426 123,142 434,736 21,516 (20,827) 435,425 (13,662) (33,467) 668 (31,685) $ 357,279 (30.2)% 119,923 18.4% 77,531 6.9% 99,885 2.7% 38,023 2.8% 21,917 1.8% $ 357,279 8.9%

EBITDA and Adjusted EBITDA

We measure our credit strength both in terms of leverage ratios and coverage ratios. The leverage ratios indicate how much of our balance sheet capitalization is

related to long-term debt, net of cash and cash equivalents and restricted cash. We expect to maintain capitalization ratios and coverage ratios sufficient to maintain a capital structure consistent with our current profile. The ratios are based on

EBITDA and Adjusted EBITDA. EBITDA is defined as earnings (net income per income statement) before interest expense, income taxes, depreciation and amortization. Adjusted EBITDA is defined as EBITDA excluding unconsolidated entities and including

adjustments for stock-based compensation expense, provision for loan losses, gains/losses on extinguishment of debt, gains/losses/impairments on properties, gains/losses on derivatives and financial instruments, other expenses, additional other

income and other impairment charges. We believe that EBITDA and Adjusted EBITDA, along with net income, are important supplemental measures because they provide additional information to assess and evaluate the performance of our operations. Our

leverage ratios include net debt to Adjusted EBITDA. Net debt is defined as total long-term debt, excluding operating lease liabilities, less cash and cash equivalents and restricted cash.

45

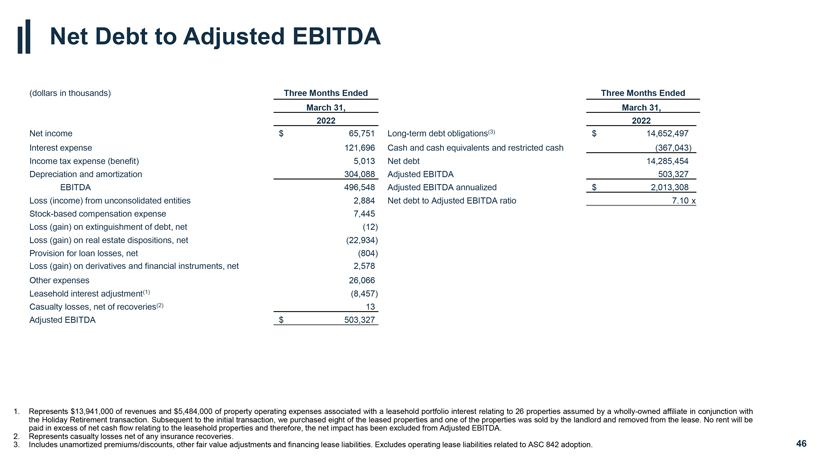

Net Debt to Adjusted EBITDA

1. Represents $13,941,000 of revenues and $5,484,000 of property operating expenses associated with a leasehold portfolio interest relating to 26 properties

assumed by a wholly-owned affiliate in conjunction with

the Holiday Retirement transaction. Subsequent to the initial transaction, we purchased eight of the leased

properties and one of the properties was sold by the landlord and removed from the lease. No rent will be

paid in excess of net cash flow relating to the leasehold

properties and therefore, the net impact has been excluded from Adjusted EBITDA.

2. Represents casualty losses net of any insurance recoveries.

3. Includes unamortized premiums/discounts, other fair value adjustments and financing lease liabilities. Excludes operating lease liabilities related to ASC 842 adoption.

46

(dollars in thousands)

Net income Interest expense

Income tax expense (benefit) Depreciation and amortization EBITDA

Loss (income) from unconsolidated entities Stock-based compensation expense Loss (gain) on extinguishment of debt, net Loss (gain) on real estate dispositions, net

Provision for loan losses, net

Loss (gain) on derivatives and financial instruments, net Other expenses Leasehold interest adjustment(1) Casualty losses, net of

recoveries(2) Adjusted EBITDA

Three Months Ended

March 31,

2022 $ 65,751 121,696 5,013 304,088 496,548 2,884 7,445 (12) (22,934) (804) 2,578 26,066 (8,457) 13 $ 503,327

Long-term debt obligations(3)

Cash and cash equivalents and restricted cash Net debt Adjusted

EBITDA

Adjusted EBITDA annualized Net debt to Adjusted EBITDA ratio

Three

Months Ended March 31, 2022 $ 14,652,497 (367,043) 14,285,454 503,327 $ 2,013,308

7.10 x

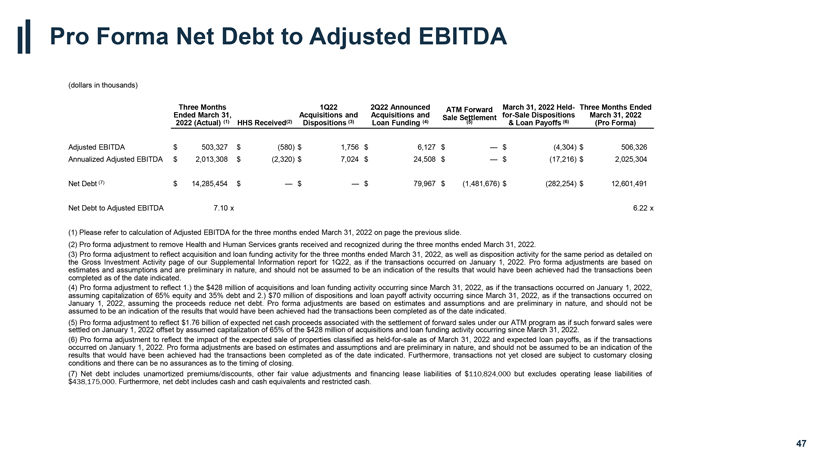

Pro Forma Net Debt to Adjusted EBITDA

(dollars in thousands)

Three Months 1Q22 2Q22 Announced ATM Forward March 31, 2022 Held-

Three Months Ended

Ended March 31, Acquisitions and Acquisitions and Sale Settlement for-Sale Dispositions

March 31, 2022

2022 (Actual) (1) HHS Received(2) Dispositions (3) Loan Funding (4) (5) & Loan Payoffs (6) (Pro Forma)

Adjusted EBITDA $ 503,327 $ (580) $ 1,756 $ 6,127 $ — $ (4,304) $ 506,326

Annualized

Adjusted EBITDA $ 2,013,308 $ (2,320) $ 7,024 $ 24,508 $ — $ (17,216) $ 2,025,304

Net Debt (7) $ 14,285,454 $ — $ — $ 79,967 $ (1,481,676) $

(282,254) $ 12,601,491

Net Debt to Adjusted EBITDA 7.10 x 6.22 x

(1) Please

refer to calculation of Adjusted EBITDA for the three months ended March 31, 2022 on page the previous slide.

(2) Pro forma adjustment to remove Health and

Human Services grants received and recognized during the three months ended March 31, 2022.

(3) Pro forma adjustment to reflect acquisition and loan funding

activity for the three months ended March 31, 2022, as well as disposition activity for the same period as detailed on

the Gross Investment Activity page of

our Supplemental Information report for 1Q22, as if the transactions occurred on January 1, 2022. Pro forma adjustments are based on estimates and assumptions and are preliminary in nature, and should not be assumed to be an indication of the

results that would have been achieved had the transactions been completed as of the date indicated.

(4) Pro forma adjustment to reflect 1.) the $428 million

of acquisitions and loan funding activity occurring since March 31, 2022, as if the transactions occurred on January 1, 2022, assuming capitalization of 65% equity and 35% debt and 2.) $70 million of dispositions and loan payoff

activity occurring since March 31, 2022, as if the transactions occurred on January 1, 2022, assuming the proceeds reduce net debt. Pro forma adjustments are based on estimates and assumptions and are preliminary in nature, and should not

be assumed to be an indication of the results that would have been achieved had the transactions been completed as of the date indicated.

(5) Pro forma adjustment

to reflect $1.76 billion of expected net cash proceeds associated with the settlement of forward sales under our ATM program as if such forward sales were settled on January 1, 2022 offset by assumed capitalization of 65% of the

$428 million of acquisitions and loan funding activity occurring since March 31, 2022.

(6) Pro forma adjustment to reflect the impact of the expected

sale of properties classified as held-for-sale as of March 31, 2022 and expected loan payoffs, as if the transactions occurred on January 1, 2022. Pro forma

adjustments are based on estimates and assumptions and are preliminary in nature, and should not be assumed to be an indication of the results that would have been achieved had the transactions been completed as of the date indicated. Furthermore,

transactions not yet closed are subject to customary closing conditions and there can be no assurances as to the timing of closing.

(7) Net debt includes

unamortized premiums/discounts, other fair value adjustments and financing lease liabilities of $110,824,000 but excludes operating lease liabilities of $438,175,000. Furthermore, net debt includes cash and cash equivalents and restricted cash.

47

48