UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CURRENT REPORT

PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Date of Report (Date of earliest event reported):

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation) |

(Commission File Number) |

(I.R.S. Employer Identification No.) |

(Address of principal executive offices, including zip code)

(Registrant’s telephone number, including area code)

N/A

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| Written communication pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

| Item 7.01 | Regulation FD Disclosure. |

As previously reported, beginning in November 2021, The GEO Group, Inc. (“GEO” and, together with its direct or indirect subsidiaries, the “Company”) engaged in confidential discussions with (i) certain members of an ad hoc group of holders (the “Noteholder Group”) of the Company’s 5.125% Senior Notes due 2023, 5.875% Senior Notes due 2024, and 6.00% Senior Notes due 2026 (such notes, collectively, the “Senior Notes”), (ii) certain members of an ad hoc group of term lenders (the “Term Lender Group”) under the Company’s Third Amended and Restated Credit Agreement, dated as of March 23, 2017 (as subsequently amended, the “Credit Agreement” and the term loans made thereunder, the “Term Loans”), and (iii) the administrative agent (the “Agent”) and certain lenders that have provided revolving credit loans and commitments under the Credit Agreement (such lenders, the “RCF Lenders” and such loans, the “RCF Loans”) concerning a potential refinancing, exchange, recapitalization, or other transaction or series of transactions to reduce the Company’s funded recourse debt and address its nearer term maturities (a “Potential Transaction”). The Company undertook these discussions on a confidential basis pursuant to non-disclosure agreements with the applicable members of the Noteholder Group and the Term Lender Group, and, in the case of the Agent and the RCF Lenders, the confidentiality provisions of the Credit Agreement.

As of January 5, 2022, the expiration date of its non-disclosure agreements with the Noteholder Group and the Term Lender Group, the Company had not reached agreement with respect to the material terms of a Potential Transaction. On January 6, 2022, in accordance with the terms of such non-disclosure agreements, the Company filed a Current Report on Form 8-K disclosing certain information provided to the Noteholder Group and the Term Lender Group on a confidential basis in connection with the above-referenced discussions, as well as a summary of the most recent proposal for a Potential Transaction delivered by each of the Company, the Noteholder Group, and the Term Lender Group prior to January 5, 2022 (the “First Refinancing Status Disclosure”).

Negotiations concerning a Potential Transaction continued after the First Refinancing Status Disclosure. On March 14, 2022, following discussions among the Company, the Agent, and the professional advisors to the Term Lender Group and the Noteholder Group, the Company executed new non-disclosure agreements with members of the Term Lender Group and the Noteholder Group, with the objective of finalizing an agreement in principle with respect to a Potential Transaction.

Despite achieving consensus on various material terms of a Potential Transaction, the Company and these creditor groups did not reach a final definitive agreement by May 2, 2022, the expiration date (as previously extended) of the above-referenced new non-disclosure agreements. In accordance with the terms of such non-disclosure agreements, the Company is disclosing through this Current Report a summary of the material terms of the most recent proposal for a Potential Transaction delivered by each of the Company, the Noteholder Group, and the Term Lender Group (the “Potential Transaction Information”). The Potential Transaction Information is attached as Exhibit 99.1 hereto and incorporated herein by reference.

As evidenced by the Potential Transaction Information, the Company believes it has made meaningful progress with the creditor groups since the First Refinancing Status Disclosure. While there can be no assurances that a Potential Transaction will be completed, and subject to the risk that market and/or credit conditions can change at any time, the Company believes a Potential Transaction can be completed on terms satisfactory to the Company. The Company thus plans to actively continue negotiations with the creditor groups concerning a Potential Transaction and, to facilitate such ongoing discussions, expects to enter into new non-disclosure agreements with certain members of the Term Lender Group and the Noteholder Group shortly.

In addition, the Company plans to continue to actively examine other options to address its funded recourse debt and its nearer term maturities, including, but not limited to, capital markets transactions, repurchases, redemptions exchanges, refinancings, repayments of existing indebtedness, and/or potential sales of Company-owned assets, if opportunities to do so are available on acceptable terms.

For information concerning the Noteholder Group, holders of the Senior Notes may contact Houlihan Lokey Capital, Inc., the financial advisor to the Noteholder Group, by email at bondholders@hl.com.

The information furnished in this Item 7.01, including Exhibit 99.1 hereto, shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise subject to the liabilities of that section, nor shall such information be deemed incorporated by reference in any filings under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such filing. The filing of this Item 7.01 of this Current Report on Form 8-K shall not be deemed an admission as to the materiality of any information herein that is required to be disclosed solely by reason of Regulation FD.

Forward-looking statements

This Current Report on Form 8-K (including Exhibit 99.1 hereto) contains forward-looking statements regarding future events and future performance of GEO that involve risks and uncertainties that could materially and adversely affect actual results, including statements regarding GEO’s proposed steps and potential alternatives to address its future debt maturities. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate,” or “continue” or the negative of such words and similar expressions. Risks and uncertainties that could cause actual results to vary from current expectations and forward-looking statements contained in this Current Report include, but are not limited to: (i) GEO’s ability to meet its financial guidance for 2022 given the various risks to which its business is exposed; (ii) GEO’s ability to reach agreement concerning a Potential Transaction on advantageous terms, or at all, or otherwise deleverage and repay, refinance, or otherwise address its debt maturities in an amount or on the timeline it expects, or at all; (iii) GEO’s ability to obtain financing or access the capital markets in the future on acceptable terms, or at all; (iv) GEO’s ability to identify and successfully complete any potential sales of additional Company-owned assets on commercially advantageous terms on a timely basis, or at all; (v) general economic and market conditions, including changes to governmental budgets and its impact on new contract terms, contract renewals, renegotiations, per diem rates, fixed payment provisions, and occupancy levels; (vi) GEO’s ability to successfully pursue growth and continue to create shareholder value; and (vii) a variety of other factors contained in GEO’s other filings with the U.S. Securities and Exchange Commission, many of which are difficult to predict and outside of GEO’s control.

| Item 9.01 | Financial Statements and Exhibits. |

(d) Exhibits:

| Exhibit Number |

Description of Exhibit | |

| 99.1 | Potential Transaction Information | |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) | |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Date: May 2, 2022 | THE GEO GROUP, INC. | |||||

| By: | /s/ Brian R. Evans | |||||

| Name: | Brian R. Evans | |||||

| Title: | Senior Vice President and Chief Financial Officer (Principal Financial Officer) | |||||

Exhibit 99.1 CONFIDENTIAL C O N F I D E N T I A L M A Y 2 0 2 2 Liability Management Transaction Proposals

CONFIDENTIAL Disclaimer Confidentiality The information in this presentation (together with the information set forth herein and any oral statements made in connection herewith, the “Presentation”) was previously delivered to certain parties on a confidential basis by The GEO Group, Inc. and certain of its subsidiaries (collectively, the “Company”) in connection with the evaluation of a potential financing transaction involving the Company. This Presentation is provided for informational purposes only and does not constitute an offer, or a solicitation of an offer, to buy or sell any securities, investment, or other product. This Presentation does not create any obligation of any party to enter into any further agreement or arrangement. Unless and until a definitive agreement has been fully executed and delivered, no contract or agreement providing for a potential transaction will exist and none of the Company nor any other party will be under any legal obligation with respect to a potential transaction. Information This Presentation does not purport to contain all of the information that may be required to evaluate a possible decision to participate in a potential financing transaction with respect to the Company; is not intended to address the specific investment objectives, financial situations, or financial needs of any particular person; and is not intended to form the basis of any such decision by the recipient or its clients. This Presentation does not constitute investment, tax, or legal advice. No representation or warranty, express or implied, is or will be given by the Company or any of its affiliates, subsidiaries, shareholders, partners, directors, officers, employees, agents, or advisors or any other person as to the accuracy or completeness of the information in this Presentation or any other written, oral, or other communications transmitted or otherwise made available to any party in the course of its evaluation of a potential transaction. No responsibility or liability whatsoever is accepted for the accuracy or sufficiency thereof or for any errors, omissions, or misstatements, negligent or otherwise, relating thereto or for possible loss of profit arising from the use of this Presentation, its contents, its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith. The information contained in this Presentation is preliminary in nature and is subject to updating, completion, revision, amendment, verification, and other changes, which could be material. The Company disclaims any duty to update the information contained in this Presentation. Forward-looking Statements This Presentation includes “forward-looking statements” within the meaning of United States securities laws. Forward-looking statements are any statements that are not based on historical information. Statements other than statements of historical facts included in this Presentation, including, without limitation, statements regarding the Company’s future financial position (including financial projections), business strategy, the impact of COVID-19 on its business, the efficacy and distribution of COVID-19 vaccines, budgets, projected costs and plans and objectives of management for future operations, are forward-looking statements. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “estimate” or “continue” or the negative of such words or variations of such words and similar expressions, but the absence of these words does not mean that a statement is not forward-looking. Such forward-looking statements are based upon the current beliefs and expectations of the Company’s management and are inherently subject to significant business, economic, and competitive uncertainties and contingencies, many of which are difficult to predict and generally beyond the control of the Company. The Company’s actual results and the timing of events may differ from the expectations, estimates, and projections anticipated in these forward-looking statements, and, consequently, you should not rely on these forward-looking statements as predictions of future events. Nothing in this Presentation should be regarded as a representation by any person that the forward-looking statements set forth herein will be achieved or that any of the contemplated results of such forward-looking statements will be achieved. You should carefully consider the risks and uncertainties described under the heading “Risk Factors” in the Company’s latest Annual Report filed with the SEC on Form 10-K and in subsequent reports filed with or furnished to the SEC. These filings identify and address important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward- looking statements. Forward-looking statements in this Presentation speak only as of the date they are made and are qualified in their entirety by reference to the cautionary statements herein and the risk factors described above. The Company neither undertakes nor accepts any obligation to release publicly any updates or revisions to any forward-looking statements to reflect any change in its expectations or any change in events, conditions, or circumstances on which any such statement is based, except as may be required by law. 1

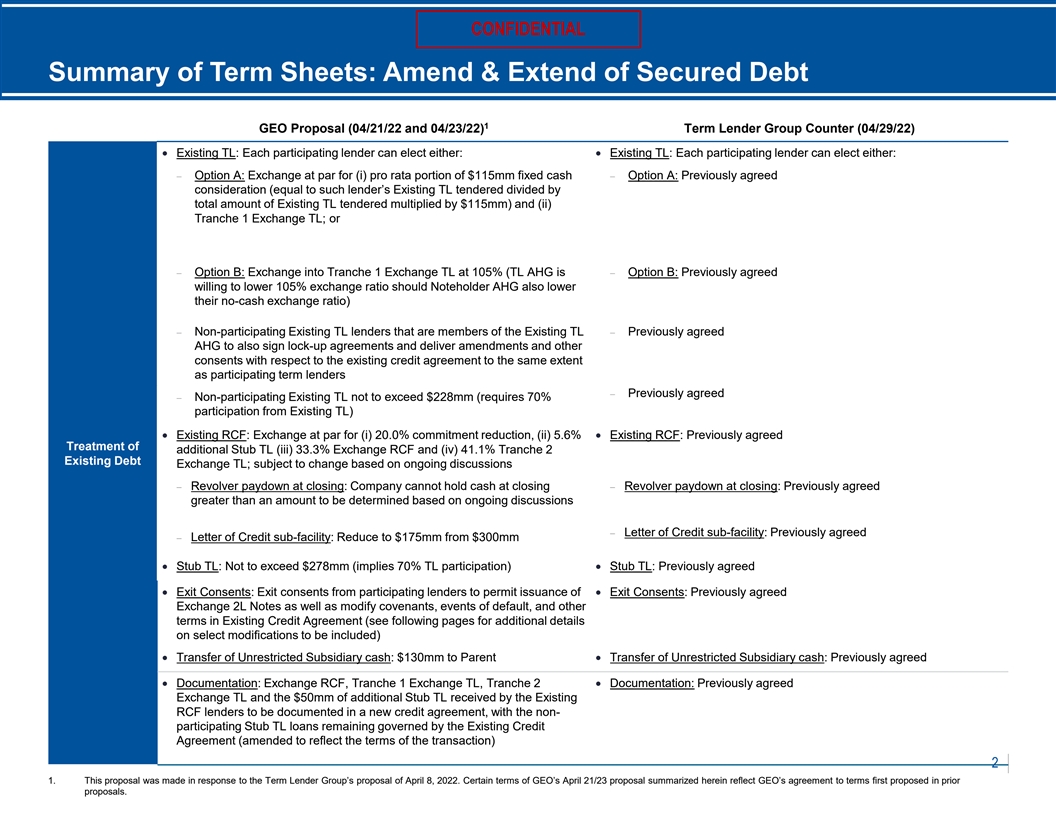

CONFIDENTIAL Summary of Term Sheets: Amend & Extend of Secured Debt 1 GEO Proposal (04/21/22 and 04/23/22) Term Lender Group Counter (04/29/22) · Existing TL: Each participating lender can elect either: · Existing TL: Each participating lender can elect either: - Option A: Exchange at par for (i) pro rata portion of $115mm fixed cash - Option A: Previously agreed consideration (equal to such lender’s Existing TL tendered divided by total amount of Existing TL tendered multiplied by $115mm) and (ii) Tranche 1 Exchange TL; or - Option B: Exchange into Tranche 1 Exchange TL at 105% (TL AHG is - Option B: Previously agreed willing to lower 105% exchange ratio should Noteholder AHG also lower their no-cash exchange ratio) - Non-participating Existing TL lenders that are members of the Existing TL - Previously agreed AHG to also sign lock-up agreements and deliver amendments and other consents with respect to the existing credit agreement to the same extent as participating term lenders - Previously agreed - Non-participating Existing TL not to exceed $228mm (requires 70% participation from Existing TL) · Existing RCF: Exchange at par for (i) 20.0% commitment reduction, (ii) 5.6% · Existing RCF: Previously agreed Treatment of additional Stub TL (iii) 33.3% Exchange RCF and (iv) 41.1% Tranche 2 Existing Debt Exchange TL; subject to change based on ongoing discussions - Revolver paydown at closing: Company cannot hold cash at closing - Revolver paydown at closing: Previously agreed greater than an amount to be determined based on ongoing discussions - Letter of Credit sub-facility: Previously agreed - Letter of Credit sub-facility: Reduce to $175mm from $300mm · Stub TL: Not to exceed $278mm (implies 70% TL participation)· Stub TL: Previously agreed · Exit Consents: Exit consents from participating lenders to permit issuance of · Exit Consents: Previously agreed Exchange 2L Notes as well as modify covenants, events of default, and other terms in Existing Credit Agreement (see following pages for additional details on select modifications to be included) · Transfer of Unrestricted Subsidiary cash: $130mm to Parent· Transfer of Unrestricted Subsidiary cash: Previously agreed · Documentation: Exchange RCF, Tranche 1 Exchange TL, Tranche 2 · Documentation: Previously agreed Exchange TL and the $50mm of additional Stub TL received by the Existing RCF lenders to be documented in a new credit agreement, with the non- participating Stub TL loans remaining governed by the Existing Credit Agreement (amended to reflect the terms of the transaction) 2 1. This proposal was made in response to the Term Lender Group’s proposal of April 8, 2022. Certain terms of GEO’s April 21/23 proposal summarized herein reflect GEO’s agreement to terms first proposed in prior proposals.

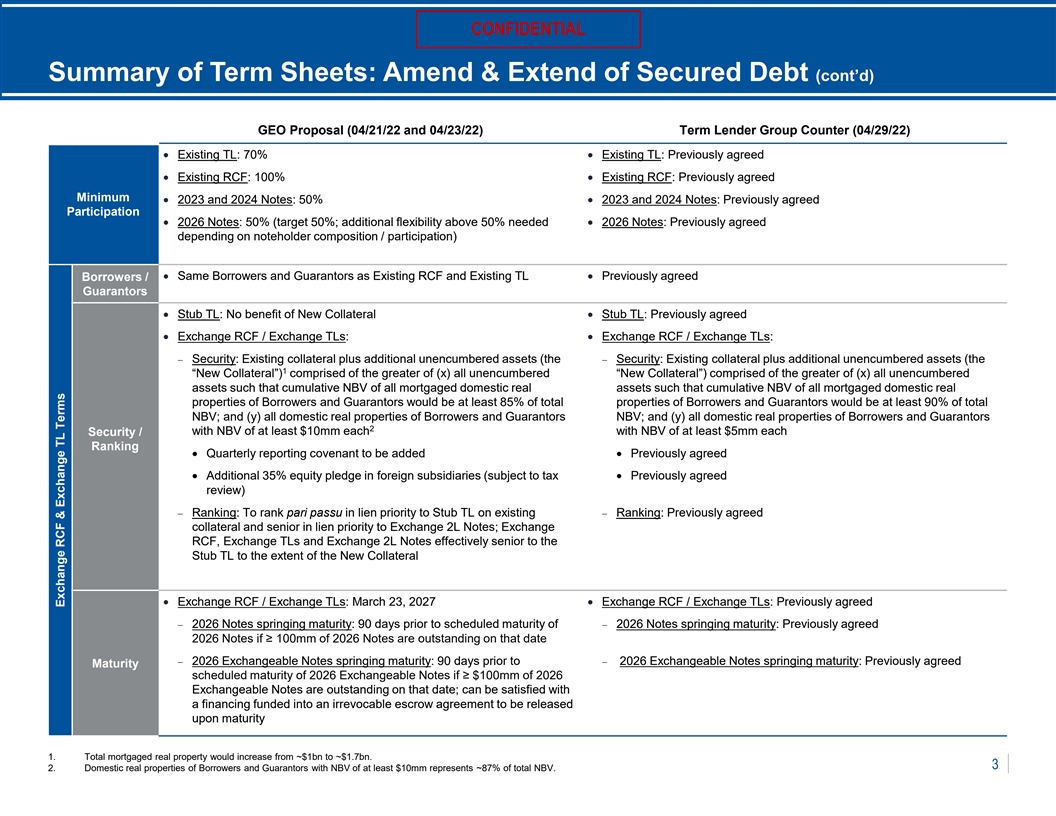

CONFIDENTIAL Summary of Term Sheets: Amend & Extend of Secured Debt (cont’d) GEO Proposal (04/21/22 and 04/23/22) Term Lender Group Counter (04/29/22) · Existing TL: 70% · Existing TL: Previously agreed · Existing RCF: 100% · Existing RCF: Previously agreed Minimum · 2023 and 2024 Notes: 50%· 2023 and 2024 Notes: Previously agreed Participation · 2026 Notes: 50% (target 50%; additional flexibility above 50% needed · 2026 Notes: Previously agreed depending on noteholder composition / participation) · Same Borrowers and Guarantors as Existing RCF and Existing TL· Previously agreed Borrowers / Guarantors · Stub TL: No benefit of New Collateral· Stub TL: Previously agreed · Exchange RCF / Exchange TLs: · Exchange RCF / Exchange TLs: - Security: Existing collateral plus additional unencumbered assets (the - Security: Existing collateral plus additional unencumbered assets (the 1 “New Collateral”) comprised of the greater of (x) all unencumbered “New Collateral”) comprised of the greater of (x) all unencumbered assets such that cumulative NBV of all mortgaged domestic real assets such that cumulative NBV of all mortgaged domestic real properties of Borrowers and Guarantors would be at least 85% of total properties of Borrowers and Guarantors would be at least 90% of total NBV; and (y) all domestic real properties of Borrowers and Guarantors NBV; and (y) all domestic real properties of Borrowers and Guarantors 2 with NBV of at least $10mm each with NBV of at least $5mm each Security / Ranking · Quarterly reporting covenant to be added· Previously agreed · Additional 35% equity pledge in foreign subsidiaries (subject to tax · Previously agreed review) - Ranking: To rank pari passu in lien priority to Stub TL on existing - Ranking: Previously agreed collateral and senior in lien priority to Exchange 2L Notes; Exchange RCF, Exchange TLs and Exchange 2L Notes effectively senior to the Stub TL to the extent of the New Collateral · Exchange RCF / Exchange TLs: March 23, 2027· Exchange RCF / Exchange TLs: Previously agreed - 2026 Notes springing maturity: 90 days prior to scheduled maturity of - 2026 Notes springing maturity: Previously agreed 2026 Notes if ≥ 100mm of 2026 Notes are outstanding on that date - 2026 Exchangeable Notes springing maturity: 90 days prior to - 2026 Exchangeable Notes springing maturity: Previously agreed Maturity scheduled maturity of 2026 Exchangeable Notes if ≥ $100mm of 2026 Exchangeable Notes are outstanding on that date; can be satisfied with a financing funded into an irrevocable escrow agreement to be released upon maturity 1. Total mortgaged real property would increase from ~$1bn to ~$1.7bn. 3 2. Domestic real properties of Borrowers and Guarantors with NBV of at least $10mm represents ~87% of total NBV. Exchange RCF & Exchange TL Terms

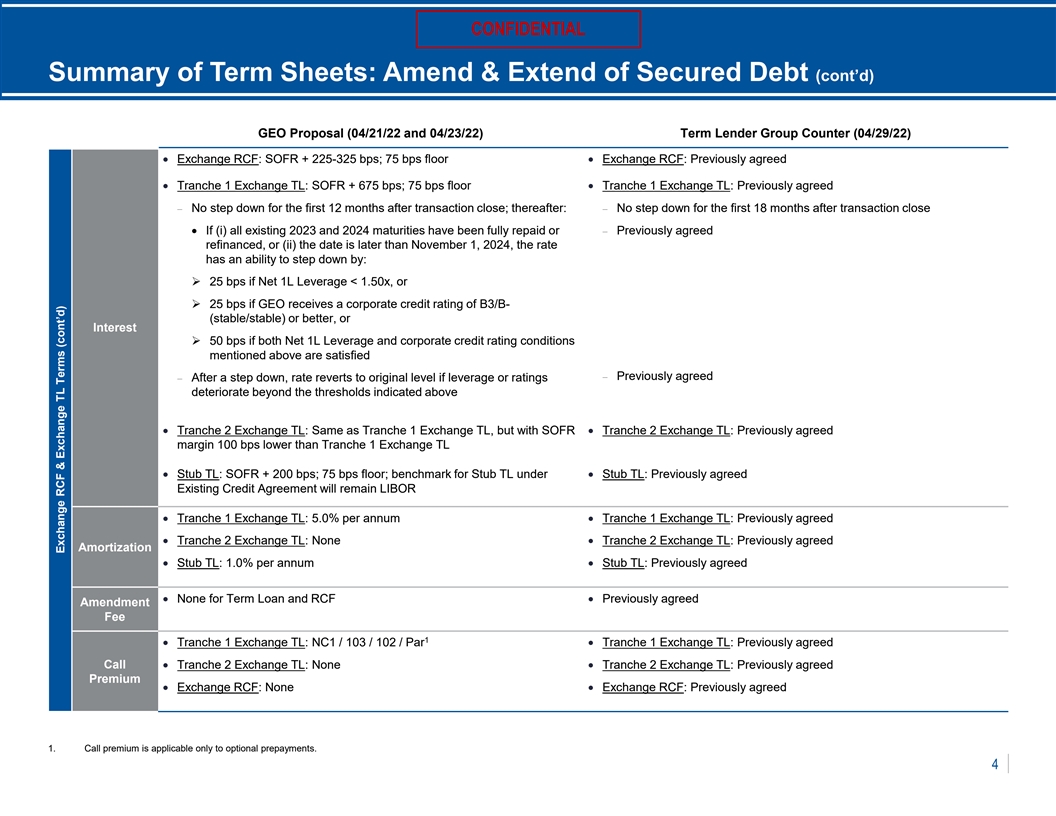

CONFIDENTIAL Summary of Term Sheets: Amend & Extend of Secured Debt (cont’d) GEO Proposal (04/21/22 and 04/23/22) Term Lender Group Counter (04/29/22) · Exchange RCF: SOFR + 225-325 bps; 75 bps floor · Exchange RCF: Previously agreed · Tranche 1 Exchange TL: SOFR + 675 bps; 75 bps floor · Tranche 1 Exchange TL: Previously agreed - No step down for the first 12 months after transaction close; thereafter:- No step down for the first 18 months after transaction close · If (i) all existing 2023 and 2024 maturities have been fully repaid or - Previously agreed refinanced, or (ii) the date is later than November 1, 2024, the rate has an ability to step down by: Ø 25 bps if Net 1L Leverage < 1.50x, or Ø 25 bps if GEO receives a corporate credit rating of B3/B- (stable/stable) or better, or Interest Ø 50 bps if both Net 1L Leverage and corporate credit rating conditions mentioned above are satisfied - Previously agreed - After a step down, rate reverts to original level if leverage or ratings deteriorate beyond the thresholds indicated above · Tranche 2 Exchange TL: Same as Tranche 1 Exchange TL, but with SOFR · Tranche 2 Exchange TL: Previously agreed margin 100 bps lower than Tranche 1 Exchange TL · Stub TL: SOFR + 200 bps; 75 bps floor; benchmark for Stub TL under · Stub TL: Previously agreed Existing Credit Agreement will remain LIBOR · Tranche 1 Exchange TL: 5.0% per annum · Tranche 1 Exchange TL: Previously agreed · Tranche 2 Exchange TL: None · Tranche 2 Exchange TL: Previously agreed Amortization · Stub TL: 1.0% per annum · Stub TL: Previously agreed · None for Term Loan and RCF· Previously agreed Amendment Fee 1 · Tranche 1 Exchange TL: NC1 / 103 / 102 / Par· Tranche 1 Exchange TL: Previously agreed Call · Tranche 2 Exchange TL: None · Tranche 2 Exchange TL: Previously agreed Premium · Exchange RCF: None · Exchange RCF: Previously agreed 1. Call premium is applicable only to optional prepayments. 4 Exchange RCF & Exchange TL Terms (cont’d)

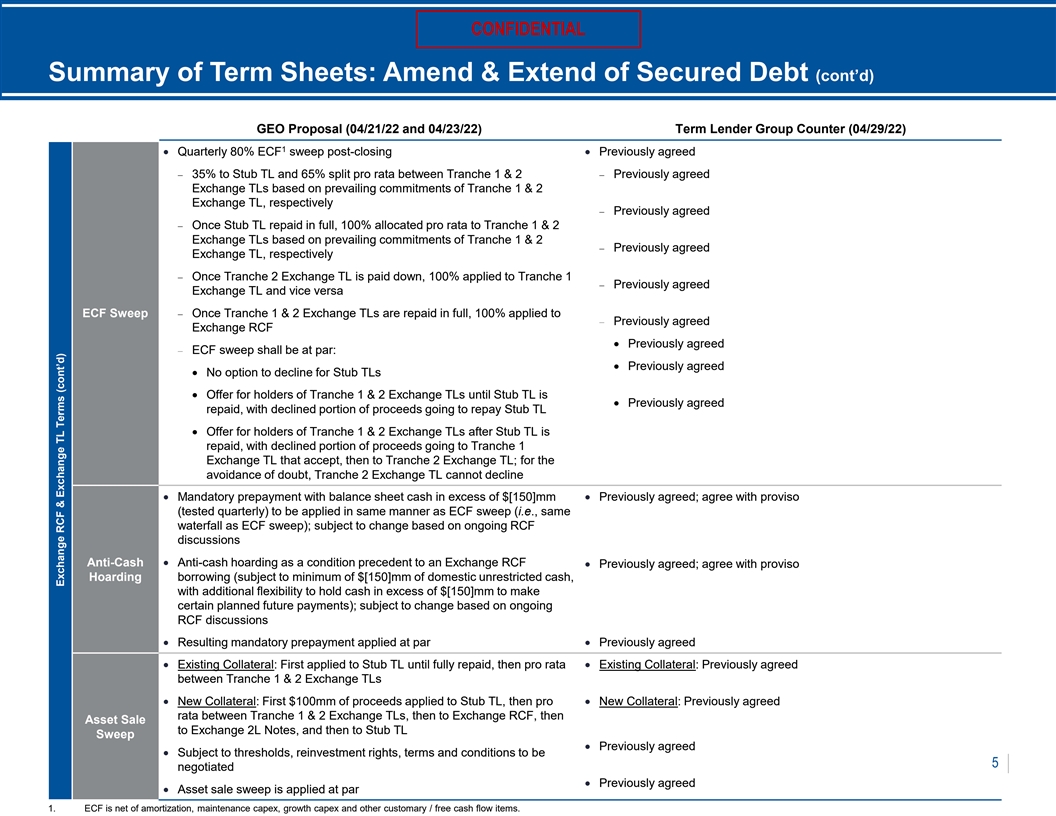

CONFIDENTIAL Summary of Term Sheets: Amend & Extend of Secured Debt (cont’d) GEO Proposal (04/21/22 and 04/23/22) Term Lender Group Counter (04/29/22) 1 · Quarterly 80% ECF sweep post-closing · Previously agreed - 35% to Stub TL and 65% split pro rata between Tranche 1 & 2 - Previously agreed Exchange TLs based on prevailing commitments of Tranche 1 & 2 Exchange TL, respectively - Previously agreed - Once Stub TL repaid in full, 100% allocated pro rata to Tranche 1 & 2 Exchange TLs based on prevailing commitments of Tranche 1 & 2 - Previously agreed Exchange TL, respectively - Once Tranche 2 Exchange TL is paid down, 100% applied to Tranche 1 - Previously agreed Exchange TL and vice versa ECF Sweep- Once Tranche 1 & 2 Exchange TLs are repaid in full, 100% applied to - Previously agreed Exchange RCF · Previously agreed - ECF sweep shall be at par: · Previously agreed · No option to decline for Stub TLs · Offer for holders of Tranche 1 & 2 Exchange TLs until Stub TL is · Previously agreed repaid, with declined portion of proceeds going to repay Stub TL · Offer for holders of Tranche 1 & 2 Exchange TLs after Stub TL is repaid, with declined portion of proceeds going to Tranche 1 Exchange TL that accept, then to Tranche 2 Exchange TL; for the avoidance of doubt, Tranche 2 Exchange TL cannot decline · Mandatory prepayment with balance sheet cash in excess of $[150]mm · Previously agreed; agree with proviso (tested quarterly) to be applied in same manner as ECF sweep (i.e., same waterfall as ECF sweep); subject to change based on ongoing RCF discussions Anti-Cash · Anti-cash hoarding as a condition precedent to an Exchange RCF · Previously agreed; agree with proviso Hoarding borrowing (subject to minimum of $[150]mm of domestic unrestricted cash, with additional flexibility to hold cash in excess of $[150]mm to make certain planned future payments); subject to change based on ongoing RCF discussions · Resulting mandatory prepayment applied at par· Previously agreed · Existing Collateral: First applied to Stub TL until fully repaid, then pro rata · Existing Collateral: Previously agreed between Tranche 1 & 2 Exchange TLs · New Collateral: First $100mm of proceeds applied to Stub TL, then pro · New Collateral: Previously agreed rata between Tranche 1 & 2 Exchange TLs, then to Exchange RCF, then Asset Sale to Exchange 2L Notes, and then to Stub TL Sweep · Previously agreed · Subject to thresholds, reinvestment rights, terms and conditions to be 5 negotiated · Previously agreed · Asset sale sweep is applied at par 1. ECF is net of amortization, maintenance capex, growth capex and other customary / free cash flow items. Exchange RCF & Exchange TL Terms (cont’d)

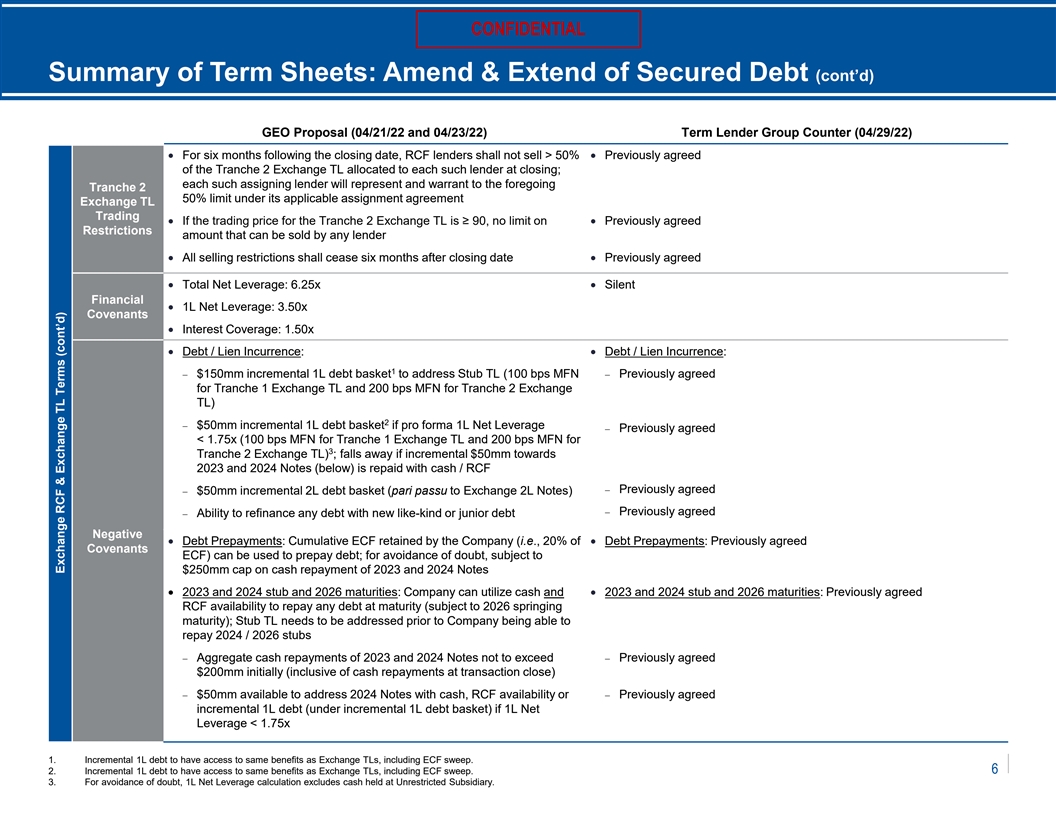

CONFIDENTIAL Summary of Term Sheets: Amend & Extend of Secured Debt (cont’d) GEO Proposal (04/21/22 and 04/23/22) Term Lender Group Counter (04/29/22) · For six months following the closing date, RCF lenders shall not sell > 50% · Previously agreed of the Tranche 2 Exchange TL allocated to each such lender at closing; each such assigning lender will represent and warrant to the foregoing Tranche 2 50% limit under its applicable assignment agreement Exchange TL Trading · If the trading price for the Tranche 2 Exchange TL is ≥ 90, no limit on · Previously agreed Restrictions amount that can be sold by any lender · All selling restrictions shall cease six months after closing date· Previously agreed · Total Net Leverage: 6.25x· Silent Financial · 1L Net Leverage: 3.50x Covenants · Interest Coverage: 1.50x · Debt / Lien Incurrence:· Debt / Lien Incurrence: 1 - $150mm incremental 1L debt basket to address Stub TL (100 bps MFN - Previously agreed for Tranche 1 Exchange TL and 200 bps MFN for Tranche 2 Exchange TL) 2 - $50mm incremental 1L debt basket if pro forma 1L Net Leverage - Previously agreed < 1.75x (100 bps MFN for Tranche 1 Exchange TL and 200 bps MFN for 3 Tranche 2 Exchange TL) ; falls away if incremental $50mm towards 2023 and 2024 Notes (below) is repaid with cash / RCF - Previously agreed - $50mm incremental 2L debt basket (pari passu to Exchange 2L Notes) - Previously agreed - Ability to refinance any debt with new like-kind or junior debt Negative · Debt Prepayments: Cumulative ECF retained by the Company (i.e., 20% of · Debt Prepayments: Previously agreed Covenants ECF) can be used to prepay debt; for avoidance of doubt, subject to $250mm cap on cash repayment of 2023 and 2024 Notes · 2023 and 2024 stub and 2026 maturities: Company can utilize cash and· 2023 and 2024 stub and 2026 maturities: Previously agreed RCF availability to repay any debt at maturity (subject to 2026 springing maturity); Stub TL needs to be addressed prior to Company being able to repay 2024 / 2026 stubs - Aggregate cash repayments of 2023 and 2024 Notes not to exceed - Previously agreed $200mm initially (inclusive of cash repayments at transaction close) - $50mm available to address 2024 Notes with cash, RCF availability or - Previously agreed incremental 1L debt (under incremental 1L debt basket) if 1L Net Leverage < 1.75x 1. Incremental 1L debt to have access to same benefits as Exchange TLs, including ECF sweep. 6 2. Incremental 1L debt to have access to same benefits as Exchange TLs, including ECF sweep. 3. For avoidance of doubt, 1L Net Leverage calculation excludes cash held at Unrestricted Subsidiary. Exchange RCF & Exchange TL Terms (cont’d)

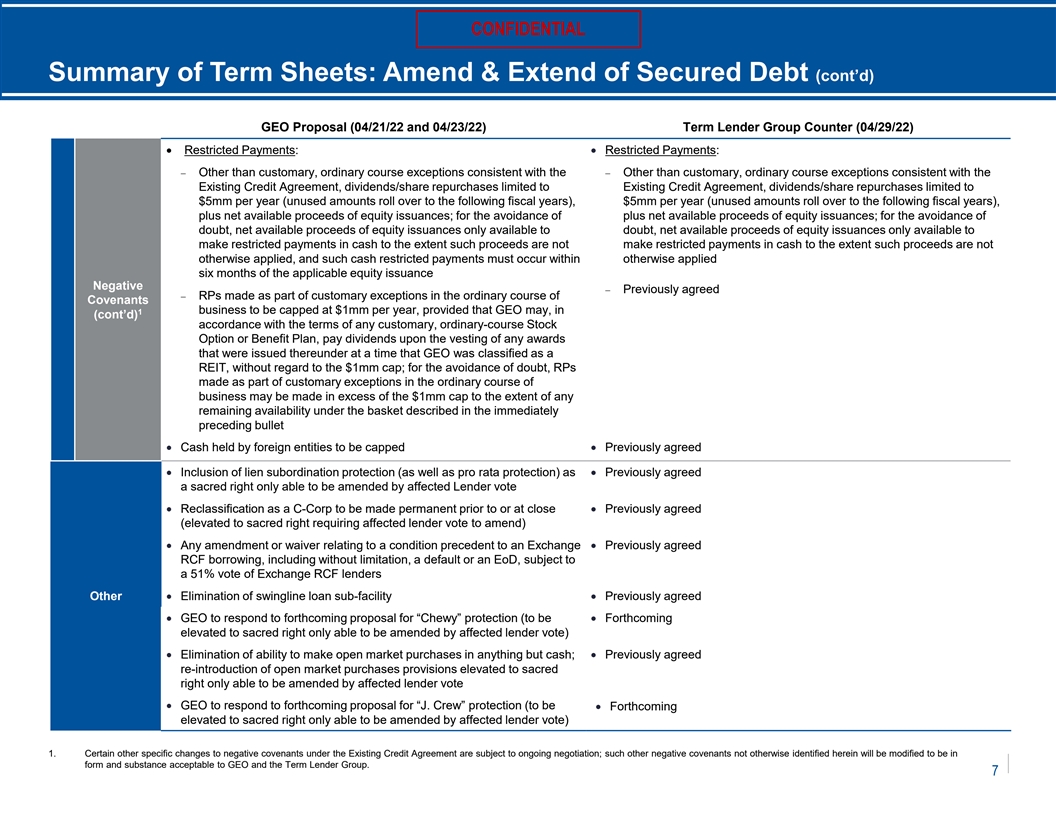

CONFIDENTIAL Summary of Term Sheets: Amend & Extend of Secured Debt (cont’d) GEO Proposal (04/21/22 and 04/23/22) Term Lender Group Counter (04/29/22) · Restricted Payments: · Restricted Payments: - Other than customary, ordinary course exceptions consistent with the - Other than customary, ordinary course exceptions consistent with the Existing Credit Agreement, dividends/share repurchases limited to Existing Credit Agreement, dividends/share repurchases limited to $5mm per year (unused amounts roll over to the following fiscal years), $5mm per year (unused amounts roll over to the following fiscal years), plus net available proceeds of equity issuances; for the avoidance of plus net available proceeds of equity issuances; for the avoidance of doubt, net available proceeds of equity issuances only available to doubt, net available proceeds of equity issuances only available to make restricted payments in cash to the extent such proceeds are not make restricted payments in cash to the extent such proceeds are not otherwise applied, and such cash restricted payments must occur within otherwise applied six months of the applicable equity issuance Negative - Previously agreed - RPs made as part of customary exceptions in the ordinary course of Covenants 1 business to be capped at $1mm per year, provided that GEO may, in (cont’d) accordance with the terms of any customary, ordinary-course Stock Option or Benefit Plan, pay dividends upon the vesting of any awards that were issued thereunder at a time that GEO was classified as a REIT, without regard to the $1mm cap; for the avoidance of doubt, RPs made as part of customary exceptions in the ordinary course of business may be made in excess of the $1mm cap to the extent of any remaining availability under the basket described in the immediately preceding bullet · Cash held by foreign entities to be capped· Previously agreed · Inclusion of lien subordination protection (as well as pro rata protection) as · Previously agreed a sacred right only able to be amended by affected Lender vote · Reclassification as a C-Corp to be made permanent prior to or at close · Previously agreed (elevated to sacred right requiring affected lender vote to amend) · Any amendment or waiver relating to a condition precedent to an Exchange · Previously agreed RCF borrowing, including without limitation, a default or an EoD, subject to a 51% vote of Exchange RCF lenders Other· Elimination of swingline loan sub-facility · Previously agreed · GEO to respond to forthcoming proposal for “Chewy” protection (to be · Forthcoming elevated to sacred right only able to be amended by affected lender vote) · Elimination of ability to make open market purchases in anything but cash; · Previously agreed re-introduction of open market purchases provisions elevated to sacred right only able to be amended by affected lender vote · GEO to respond to forthcoming proposal for “J. Crew” protection (to be · Forthcoming elevated to sacred right only able to be amended by affected lender vote) 1. Certain other specific changes to negative covenants under the Existing Credit Agreement are subject to ongoing negotiation; such other negative covenants not otherwise identified herein will be modified to be in form and substance acceptable to GEO and the Term Lender Group. 7

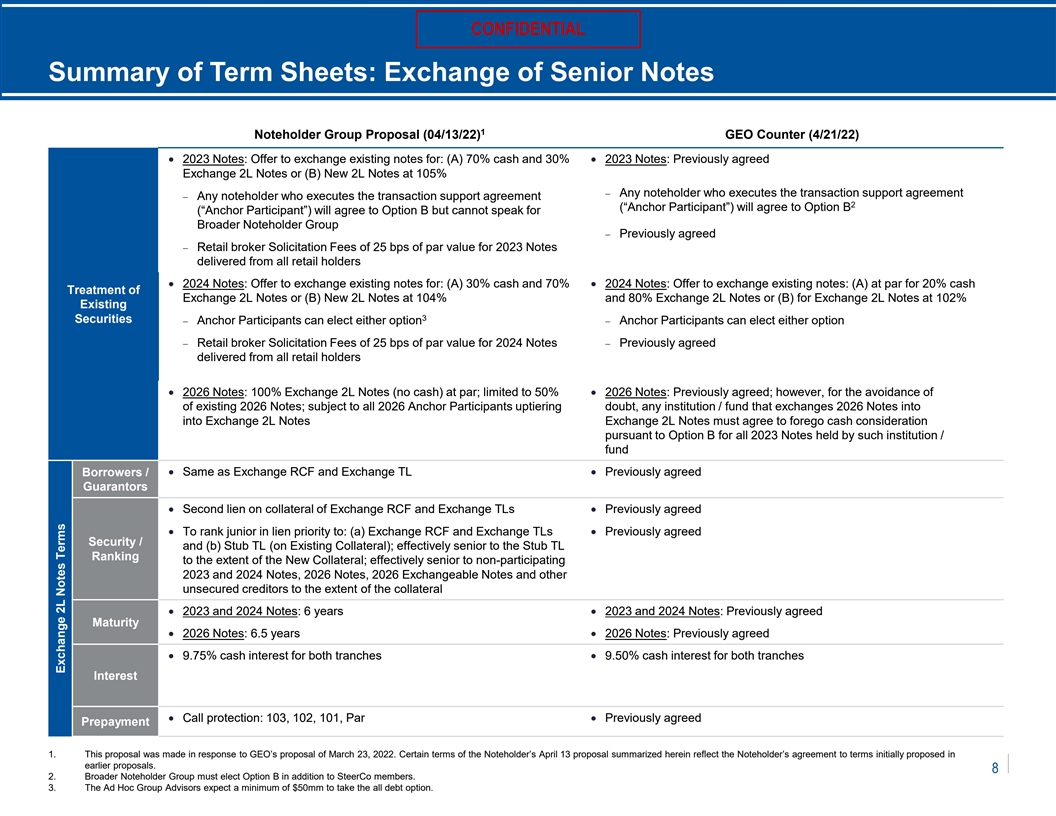

CONFIDENTIAL Summary of Term Sheets: Exchange of Senior Notes 1 Noteholder Group Proposal (04/13/22) GEO Counter (4/21/22) · 2023 Notes: Offer to exchange existing notes for: (A) 70% cash and 30% · 2023 Notes: Previously agreed Exchange 2L Notes or (B) New 2L Notes at 105% - Any noteholder who executes the transaction support agreement - Any noteholder who executes the transaction support agreement 2 (“Anchor Participant”) will agree to Option B (“Anchor Participant”) will agree to Option B but cannot speak for Broader Noteholder Group - Previously agreed - Retail broker Solicitation Fees of 25 bps of par value for 2023 Notes delivered from all retail holders · 2024 Notes: Offer to exchange existing notes for: (A) 30% cash and 70% · 2024 Notes: Offer to exchange existing notes: (A) at par for 20% cash Treatment of Exchange 2L Notes or (B) New 2L Notes at 104% and 80% Exchange 2L Notes or (B) for Exchange 2L Notes at 102% Existing 3 Securities - Anchor Participants can elect either option- Anchor Participants can elect either option - Retail broker Solicitation Fees of 25 bps of par value for 2024 Notes - Previously agreed delivered from all retail holders · 2026 Notes: 100% Exchange 2L Notes (no cash) at par; limited to 50% · 2026 Notes: Previously agreed; however, for the avoidance of of existing 2026 Notes; subject to all 2026 Anchor Participants uptiering doubt, any institution / fund that exchanges 2026 Notes into into Exchange 2L Notes Exchange 2L Notes must agree to forego cash consideration pursuant to Option B for all 2023 Notes held by such institution / fund Borrowers / · Same as Exchange RCF and Exchange TL · Previously agreed Guarantors · Second lien on collateral of Exchange RCF and Exchange TLs · Previously agreed · To rank junior in lien priority to: (a) Exchange RCF and Exchange TLs · Previously agreed Security / and (b) Stub TL (on Existing Collateral); effectively senior to the Stub TL Ranking to the extent of the New Collateral; effectively senior to non-participating 2023 and 2024 Notes, 2026 Notes, 2026 Exchangeable Notes and other unsecured creditors to the extent of the collateral · 2023 and 2024 Notes: 6 years · 2023 and 2024 Notes: Previously agreed Maturity · 2026 Notes: 6.5 years· 2026 Notes: Previously agreed · 9.75% cash interest for both tranches· 9.50% cash interest for both tranches Interest · Call protection: 103, 102, 101, Par· Previously agreed Prepayment 1. This proposal was made in response to GEO’s proposal of March 23, 2022. Certain terms of the Noteholder’s April 13 proposal summarized herein reflect the Noteholder’s agreement to terms initially proposed in earlier proposals. 8 2. Broader Noteholder Group must elect Option B in addition to SteerCo members. 3. The Ad Hoc Group Advisors expect a minimum of $50mm to take the all debt option. Exchange 2L Notes Terms

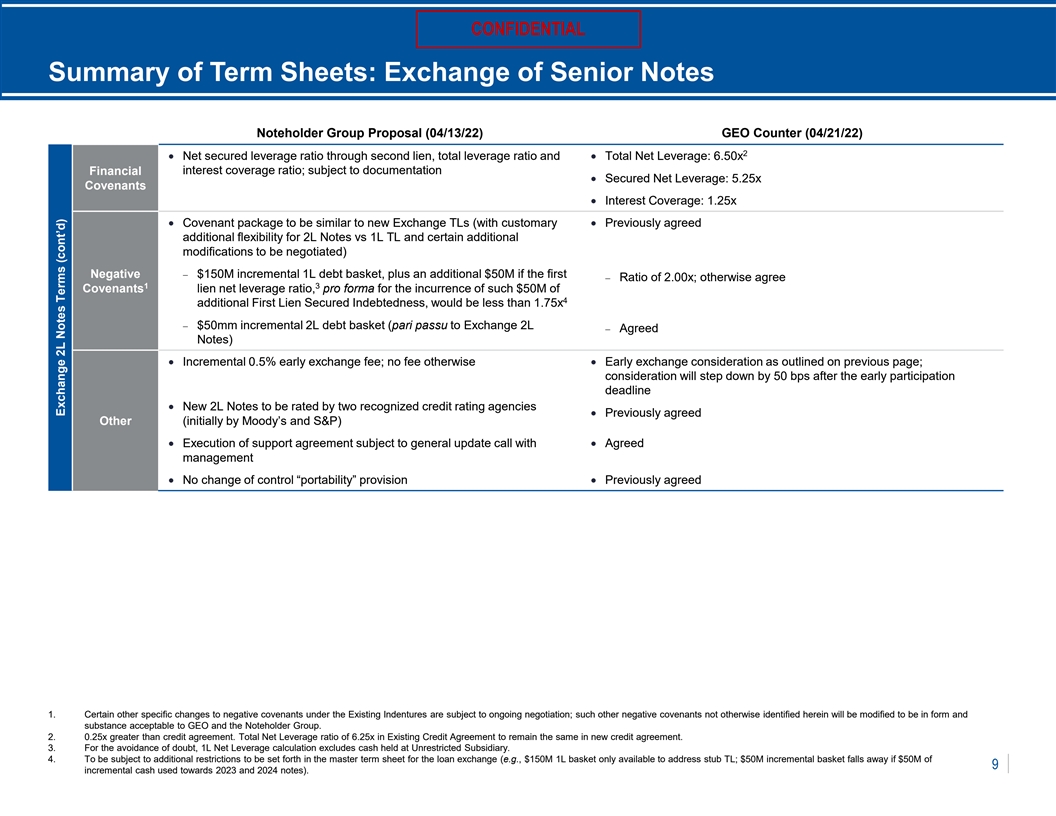

CONFIDENTIAL Summary of Term Sheets: Exchange of Senior Notes Noteholder Group Proposal (04/13/22) GEO Counter (04/21/22) 2 · Net secured leverage ratio through second lien, total leverage ratio and · Total Net Leverage: 6.50x interest coverage ratio; subject to documentation Financial · Secured Net Leverage: 5.25x Covenants · Interest Coverage: 1.25x · Covenant package to be similar to new Exchange TLs (with customary · Previously agreed additional flexibility for 2L Notes vs 1L TL and certain additional modifications to be negotiated) Negative - $150M incremental 1L debt basket, plus an additional $50M if the first - Ratio of 2.00x; otherwise agree 1 3 Covenants lien net leverage ratio, pro forma for the incurrence of such $50M of 4 additional First Lien Secured Indebtedness, would be less than 1.75x - $50mm incremental 2L debt basket (pari passu to Exchange 2L - Agreed Notes) · Incremental 0.5% early exchange fee; no fee otherwise· Early exchange consideration as outlined on previous page; consideration will step down by 50 bps after the early participation deadline · New 2L Notes to be rated by two recognized credit rating agencies · Previously agreed Other (initially by Moody’s and S&P) · Execution of support agreement subject to general update call with · Agreed management · No change of control “portability” provision· Previously agreed 1. Certain other specific changes to negative covenants under the Existing Indentures are subject to ongoing negotiation; such other negative covenants not otherwise identified herein will be modified to be in form and substance acceptable to GEO and the Noteholder Group. 2. 0.25x greater than credit agreement. Total Net Leverage ratio of 6.25x in Existing Credit Agreement to remain the same in new credit agreement. 3. For the avoidance of doubt, 1L Net Leverage calculation excludes cash held at Unrestricted Subsidiary. 4. To be subject to additional restrictions to be set forth in the master term sheet for the loan exchange (e.g., $150M 1L basket only available to address stub TL; $50M incremental basket falls away if $50M of 9 incremental cash used towards 2023 and 2024 notes). Exchange 2L Notes Terms (cont’d)