Use these links to rapidly review the document

TABLE OF CONTENTS Prospectus Supplement

TABLE OF CONTENTS

Filed pursuant to Rule 424(b)(5)

Registration Statement No. 333-230106

P R O S P E C T U S S U P P L E M E N T

(to Prospectus dated March 18, 2019)

9,000,000 Shares

Danaos Corporation

Common Stock

We are offering 9,000,000 shares of common stock (our "common stock") pursuant to this prospectus supplement and the accompanying prospectus. Our common stock is listed on the New York Stock Exchange under the symbol "DAC." On November 21, 2019, the last reported sale price of our common stock on the New York Stock Exchange was $7.65 per share.

Certain of our significant stockholders, which are affiliates or family members of certain of our officers and directors, and executive officers have agreed to purchase approximately $27 million of common stock in the offering at the public offering price, including approximately $17 million by Danaos Investment Limited, which is our largest stockholder and beneficially owned by Dr. John Coustas, our Chief Executive Officer.

Investing in our common stock involves a high degree of risk. Please read "Risk Factors" beginning on page S-14 of this prospectus supplement, on page 4 of the accompanying prospectus and beginning on page 5 of our Annual Report on Form 20-F filed with the Securities and Exchange Commission on March 5, 2019 before you make an investment in our shares.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus supplement or the accompanying prospectus. Any representation to the contrary is a criminal offense.

| |

Per Share | Total(2) | ||

|---|---|---|---|---|

| Public offering price | $6.00 | $54,000,000 | ||

| Underwriting discounts and commissions(1) | $0.42 | $ 1,892,801 | ||

| Proceeds to us (before expenses and fees) | $5.58 | $52,107,199 |

We have granted the underwriters an option, exercisable in whole or from time to time in part, for a period of 30 days after the date of this prospectus supplement to purchase up to an additional 1,350,000 shares of our common stock directly from us at the public offering price per share shown above, less the underwriting discount per share shown above. If the underwriters exercise the option in full, the total underwriting discounts and commissions payable by us will be $2,459,801, and the total proceeds to us, before expenses and fees, will be $59,640,199.

Delivery of the shares of common stock is expected to be made on or about November 26, 2019.

| Citigroup | Jefferies |

The date of this prospectus supplement is November 21, 2019.

TABLE OF CONTENTS

Prospectus Supplement

S-i

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of this offering of our common stock and certain other matters. The second part, the prospectus, gives more general information about securities we may offer from time to time. Generally, when we refer to the "prospectus," we are referring to both parts of this document combined. You should read both this prospectus supplement and the accompanying prospectus, together with additional information described under the headings "Where You Can Find Additional Information" and "Incorporation by Reference." To the extent the description of our securities in this prospectus supplement differs from the description of our securities in the accompanying prospectus, you should rely on the information in this prospectus supplement.

You should rely only on the information contained or incorporated by reference into this prospectus supplement, the accompanying prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We have not, and the underwriters have not, authorized anyone to provide you with different information. Neither we nor the underwriters take any responsibility for, or provide any assurances as to the reliability of, any additional or different information that others may give you. The distribution of this prospectus supplement and sale of these securities in certain jurisdictions may be restricted by law. Persons in possession of this prospectus supplement or the accompanying prospectus are required to inform themselves about and observe any such restrictions. We are not making an offer to sell these securities, or seeking offers to buy our common stock, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus supplement, the accompanying prospectus and any related free writing prospectus is accurate as of the respective dates specified in such information, as applicable, and the information contained in documents incorporated by reference is accurate only as of the respective dates of those documents or as of the respective dates specified in such information, as applicable, in each case regardless of the time of delivery of this prospectus supplement, the accompanying prospectus, any such free writing prospectus or any sale of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

S-ii

WHERE YOU CAN FIND ADDITIONAL INFORMATION

We have filed with the Securities and Exchange Commission (the "SEC") a registration statement on Form F-3 under the Securities Act of 1933, as amended (the "Securities Act"), with respect to the offer and sale of securities pursuant to this prospectus supplement. This prospectus supplement, filed as a part of the registration statement, does not contain all of the information set forth in the registration statement. The registration statement includes and incorporates by reference additional information and exhibits. Statements made in this prospectus supplement concerning the contents of any contract, agreement or other document filed as an exhibit to the registration statement are summaries of all of the material terms of such contracts, agreements or documents, but do not repeat all of their terms. Reference is made to each such exhibit for a more complete description of the matters involved and such statements shall be deemed qualified in their entirety by such reference. The registration statement and the exhibits and schedules thereto filed with the SEC may be accessed, free of charge, on the SEC's website at http://www.sec.gov.

We are subject to the information and periodic reporting requirements of the Securities Exchange Act of 1934, as amended (the "Exchange Act") and we file periodic reports and other information with the SEC. These periodic reports and other information we file with the SEC are available to the public on the SEC's website at http://www.sec.gov. You may also inspect our SEC filings at the offices of the New York Stock Exchange (the "NYSE") at 20 Broad Street, New York, New York 10005. As a "foreign private issuer," we are exempt from the rules under the Exchange Act prescribing the furnishing and content of proxy statements to stockholders, but we are required to furnish certain proxy statements to stockholders under NYSE rules. Those proxy statements are not expected to conform to Schedule 14A of the proxy rules promulgated under the Exchange Act. In addition, as a "foreign private issuer," we are exempt from the rules under the Exchange Act relating to short swing profit reporting and liability.

S-iii

The SEC allows us to "incorporate by reference" the information we file with the SEC. This means that we can disclose important information to you by referring you to another document filed separately with the SEC. The information incorporated by reference is considered to be part of this prospectus supplement. Any information that we file later with the SEC and that is deemed incorporated by reference will also be considered to be part of this prospectus supplement and will automatically update and supersede the information in this prospectus supplement. In all cases, you should rely on the later information over different information included in this prospectus supplement.

This prospectus supplement incorporates by reference the following documents:

We are also incorporating by reference all subsequent annual reports on Form 20-F that we file with the SEC and certain reports on Form 6-K that we furnish to the SEC after the date of this prospectus supplement (in each case, if such Form 6-K states that it is incorporated by reference into this prospectus supplement) until we file a post-effective amendment indicating that the offering of the securities made by this prospectus supplement has been terminated. In all cases, you should rely on the later information over different information included in this prospectus supplement.

We will provide, free of charge upon written or oral request, to each person to whom this prospectus supplement is delivered, including any beneficial owner of the securities, a copy of any or all of the information that has been incorporated by reference into this prospectus supplement, but which has not been delivered with the prospectus. Copies of these documents also may be obtained on the "Investors" section of our website at http://www.danaos.com. The information contained on or linked to or from our website is not incorporated by reference into this prospectus supplement and should not be considered part of this prospectus supplement. Requests for such information should be made to us at the following address:

Danaos

Corporation

c/o Danaos Shipping Co. Ltd.

14 Akti Kondyli

185 45 Piraeus, Greece

Telephone No.: + 30 210 419 6401

Fax No.: + 30 210 419 6489

Attention: Chief Financial Officer

You should assume that the information appearing in this prospectus supplement and the accompanying prospectus, as well as the information we previously filed with the SEC and incorporated by reference, is accurate as of the dates on the front cover of those documents only. Our business, financial condition and results of operations and prospects may have changed since those dates.

S-iv

FORWARD-LOOKING STATEMENTS; CAUTIONARY INFORMATION

All statements in this prospectus supplement (and in the documents incorporated by reference herein) that are not statements of historical fact are "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995. The disclosure and analysis set forth in this prospectus supplement includes assumptions, expectations, projections, intentions and beliefs about future events in a number of places, particularly in relation to our operations, cash flows, financial position, including vessel and other asset values, plans, strategies, business prospects, changes and trends in our business and the markets in which we operate. These statements are intended as "forward-looking statements." In some cases, predictive, future-tense or forward-looking words such as "believe," "intend," "anticipate," "estimate," "project," "forecast," "plan," "potential," "may," "should," "could" and "expect" and similar expressions are intended to identify forward-looking statements, but are not the exclusive means of identifying such statements. In addition, we and our representatives may from time to time make other oral or written statements which are forward-looking statements, including in our periodic reports that we file with the SEC, other information sent to our security holders, and other written materials. We caution that these and other forward- looking statements included in this prospectus supplement (and in the documents incorporated by reference herein) represent our estimates and assumptions as of the date of this prospectus supplement or the accompanying prospectus, respectively (and as of the date of the documents incorporated by reference herein) or the date on which such oral or written statements are made, as applicable, about factors that are beyond our ability to control or predict, and are not intended to give any assurance as to future results.

Factors that might cause future results to differ include, but are not limited to, the following:

S-v

We undertake no obligation to update or revise any forward-looking statements contained in this prospectus supplement, whether as a result of new information, future events, a change in our views or expectations or otherwise. New factors emerge from time to time, and it is not possible for us to predict all of these factors. Further, we cannot assess the impact of each such factor on our business or the extent to which any factor, or combination of factors, may cause actual results to be materially different from those contained in any forward-looking statement.

S-vi

This summary highlights information contained in other parts of and incorporated by reference into this prospectus supplement. Because it is only a summary, it does not contain all of the information that you should consider before investing in our common stock and it is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere in and incorporated by reference into this prospectus supplement. You should read the entire prospectus carefully, and all documents incorporated by reference into this prospectus supplement, including "Risk Factors" and our financial statements and the related notes, before deciding to buy our common stock.

We use the term "twenty foot equivalent unit," or "TEU," the international standard measure of containers, in describing the capacity of our containerships. Unless otherwise indicated, all references to currency amounts in this annual report are in U.S. dollars. Unless the context otherwise requires, references to the "Company," "we," "us," "our" or "Danaos" refer to Danaos Corporation, a Marshall Islands corporation, and references to "Gemini" are to Gemini Shipholdings Corporation, a Marshall Islands corporation incorporated in August 2015 and beneficially owned 49% by Danaos Corporation and 51% by Virage International Ltd., a company controlled by Danaos Corporation's largest stockholder. We do not consolidate Gemini's results of operations and account for our minority equity interest in Gemini under the equity method of accounting.

Our Company

We are an international owner of containerships with more than 40 years' experience owning, managing and chartering our vessels to many of the world's largest liner companies. As of September 30, 2019, we had a fleet of 60 containerships aggregating 360,147 TEUs, making us among the largest containership charter owners in the world, based on total TEU capacity. Our fleet of 60 containerships includes five containerships of 32,531 TEU aggregate capacity which are owned by Gemini Shipholdings Corporation ("Gemini"), in which we have a 49% minority equity interest. In October 2019, we entered into an agreement to acquire a 8,500 TEU containership built in 2005 for $25 million, with expected delivery to us by the end of May 2020.

Our strategy is to charter our containerships principally under favorable, multi-year, fixed-rate period charters, to a diverse group of major liner companies that operate regularly scheduled routes between large commercial ports. These customers currently include CMA-CGM, Hyundai Merchant Marine, MSC, Yang Ming, Hapag Lloyd, ZIM, OOCL, Maersk, COSCO, Evergreen, ONE and Samudera.

As of September 30, 2019, the average remaining duration of the charters for our 55 fully-owned containerships was 4.3 years (weighted by aggregate contracted charter hire). As of September 30, 2019, these contracts are expected to provide total contracted revenues of $1.4 billion during their initial terms, which expire between 2019 and 2028. Our charters have initial terms ranging up to 18 years, which provide us with stable cash flows and high utilization rates. Our fleet ranges in size from 2,200-13,100 TEU, providing us flexibility to serve the diverse needs of our customers.

Our Company's long history in the shipping industry dates back to the 1960s. Our largest stockholder is Danaos Investment Limited, an entity affiliated with our Chief Executive Officer, Dr. John Coustas. Dimitris Coustas, the father of our Chief Executive Officer, John Coustas, first invested in shipping in 1963 and founded Danaos Shipping Company Limited, which we refer to as Danaos Shipping or our manager, in 1972. After assuming management of our company in 1987, John Coustas has focused our strategy on building a large, modern containership fleet to serve the container shipping industry and grown our fleet from three multi-purpose vessels with a capacity of 2,395 TEUs to our current wholly-owned fleet of 55 containerships aggregating 327,616 TEUs.

S-1

As the Company has grown we have remained at the forefront of innovation and responsiveness to changes affecting our industry. We maintain an active dialogue with our customers around potential investment opportunities for newbuild vessels or technical innovations that can improve our operations and service to our customers. Further, our commitment to safe and environmentally sound operations is core to the Company. We have agreed to install scrubbers on nine of our vessels in collaboration with our customers, we have installed ballast water treatment systems to comply with regulations across our fleet, and we expect to be operationally compliant with new IMO 2020 low-sulfur fuel oil regulations when they go into effect next year.

Our strategic focus is enhancing shareholder value by continuing to reduce leverage and generating favorable returns through rational growth, including opportunistic acquisitions of new or secondhand vessels if there is a case for such investment. We believe that recent transactions we have undertaken, including significantly reducing our debt in 2018, continuing to manage our charter portfolio and acquiring two secondhand vessels in recent months, position us well with respect to executing on our objectives.

Our Fleet

The table below provides additional information, as of November 15, 2019, about our fleet of 55 cellular containerships and the five cellular containerships owned by Gemini, in which we have a 49% equity interest.

Vessel Name

|

| Year Built |

| Vessel Size (TEU) |

| Expiration of Charter(1) |

| Charterer | | Charter Type(2) |

| Through | | Charter Rate(3) |

| Extension Options(4) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

MSC Ambition |

| | 2012 | | | | 13,100 | | | June 2024 | | HMM | | T/C | | December 2019 | | $49,563 | | |||

|

| | | | | | | | | T/C | | April 2020(6) | | $59,418 | | |||||||

|

| | | | | | | | | T/C | | June 2024 | | $64,918 | | +3 years at $60,418 | ||||||

Maersk Exeter |

| | 2012 |

| | | 13,100 |

| | June 2024 |

| HMM |

| T/C |

| December 2019 |

| $49,563 |

| |||

|

| | | | | | | | | T/C | | May 2020(6) | | $59,418 | | |||||||

|

| | | | | | | | | T/C | | June 2024 | | $64,918 | | +3 years at $60,418 | ||||||

Maersk Enping |

| | 2012 |

| | | 13,100 |

| | May 2024 |

| HMM |

| T/C |

| December 2019 |

| $49,563 |

| |||

|

| | | | | | | | | T/C | | May 2020(6) | | $59,418 | | |||||||

|

| | | | | | | | | T/C | | May 2024 | | $64,918 | | +3 years at $60,418 | ||||||

Hyundai Respect(12) |

| | 2012 |

| | | 13,100 |

| | March 2024 |

| HMM |

| B/B |

| December 2019 |

| $42,594 |

| |||

|

| | | | | | | | | B/B | | March 2020(6) | | $52,449 | | |||||||

|

| | | | | | | | | B/B(5) | | May 2020 | | $57,949 | | |||||||

|

| | | | | | | | | T/C | | March 2024 | | $64,918 | | +3 years at $60,418 | ||||||

Hyundai Honour(12) |

| | 2012 |

| | | 13,100 |

| | February 2024 |

| HMM |

| B/B |

| December 2019 |

| $42,594 |

| |||

|

| | | | | | | | | B/B | | January 2020(6) | | $52,449 | | |||||||

|

| | | | | | | | | B/B(5) | | May 2020 | | $57,949 | | |||||||

|

| | | | | | | | | T/C | | February 2024 | | $64,918 | | +3 years at $60,418 | ||||||

Express Rome |

| | 2011 |

| | | 10,100 |

| | February 2022 |

| Hapag Lloyd |

| T/C |

| May 2021 |

| $27,000 |

| |||

|

| | | | | | | | | T/C | | February 2022 | | $28,000 | | +3 months at $28,000 | ||||||

|

| | | | | | | | | | | | +10 up to 14 months at $29,000 | |||||||||

Express Berlin |

| | 2011 | | | | 10,100 | | | April 2022 | | Yang Ming | | T/C | | December 2019 | | $25,000 | | |||

|

| | | | | | | | | T/C | | April 2022 | | $27,750 | | +4 months at $27,750 | ||||||

Express Athens |

| | 2011 |

| | | 10,100 |

| | February 2022 |

| Hapag Lloyd |

| T/C |

| May 2021 |

| $27,000 |

| |||

|

| | | | | | | | | T/C | | February 2022 | | $28,000 | | +3 months at $28,000 | ||||||

|

| | | | | | | | | | | | +10 up to 14 months at $29,000 | |||||||||

Le Havre |

| | 2006 |

| | | 9,580 |

| | February 2023 |

| MSC |

| T/C |

| February 2020(6) |

| $13,000 |

| |||

|

| | | | | | | | | T/C | | February 2023(8) | | $23,000 | | +4 months at $23,000 | ||||||

Pusan C |

| | 2006 |

| | | 9,580 |

| | February 2023 |

| MSC |

| T/C |

| February 2020(6) |

| $13,000 |

| |||

|

| | | | | | | | | T/C | | February 2023(8) | | $23,000 | | +4 months at $23,000 | ||||||

CMA CGM Melisande |

| | 2012 |

| | | 8,530 |

| | May 2024 |

| CMA CGM |

| T/C |

| November 2023 |

| $43,000 |

| |||

|

| | | | | | | | | T/C | | May 2024 | | at market(7) | | +6 months at market(7) | ||||||

S-2

Vessel Name

|

| Year Built |

| Vessel Size (TEU) |

| Expiration of Charter(1) |

| Charterer | | Charter Type(2) |

| Through | | Charter Rate(3) |

| Extension Options(4) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

CMA CGM Attila |

| | 2011 | | | | 8,530 | | | October 2023 |

| CMA CGM |

| T/C |

| April 2023 |

| $43,000 |

| |||

|

| | | | | | | | | T/C | | October 2023 | | at market(7) | | +6 months at market(7) | ||||||

CMA CGM Tancredi |

| | 2011 |

| | | 8,530 |

| | November 2023 |

| CMA CGM |

| T/C |

| May 2023 |

| $43,000 |

| |||

|

| | | | | | | | | T/C | | November 2023 | | at market(7) | | +6 months at market(7) | ||||||

CMA CGM Bianca |

| | 2011 |

| | | 8,530 |

| | January 2024 |

| CMA CGM |

| T/C |

| July 2023 |

| $43,000 |

| |||

|

| | | | | | | | | T/C | | January 2024 | | at market(7) | | +6 months at market(7) | ||||||

CMA CGM Samson |

| | 2011 |

| | | 8,530 |

| | March 2024 |

| CMA CGM |

| T/C |

| September 2023 |

| $43,000 |

| |||

|

| | | | | | | | | T/C | | March 2024 | | at market(7) | | +6 months at market(7) | ||||||

America |

| | 2004 |

| | | 8,468 |

| | January 2023 |

| MSC |

| T/C |

| January 2020(6) |

| $13,000 |

| |||

|

| | | | | | | | | T/C | | January 2023(8) | | $22,000 | | +4 months at $22,000 | ||||||

Europe |

| | 2004 |

| | | 8,468 |

| | March 2023 |

| MSC |

| T/C |

| March 2020(6) |

| $13,000 |

| |||

|

| | | | | | | | | T/C | | March 2023(8) | | $22,000 | | +4 months at $22,000 | ||||||

CMA CGM Moliere |

| | 2009 |

| | | 6,500 |

| | August 2021 |

| CMA CGM |

| T/C |

| August 2021 |

| $34,350 |

| +2 months at $34,350 |

||

CMA CGM Musset |

| | 2010 |

| | | 6,500 |

| | August 2022 |

| CMA CGM |

| T/C |

| February 2022 |

| $34,350 |

| |||

|

| | | | | | | | | T/C | | August 2022 | | at market(7) | | +6 months at market(7) | ||||||

CMA CGM Nerval |

| | 2010 |

| | | 6,500 |

| | October 2022 |

| CMA CGM |

| T/C |

| April 2022 |

| $34,350 |

| |||

|

| | | | | | | | | T/C | | October 2022 | | at market(7) | | +6 months at market(7) | ||||||

CMA CGM Rabelais |

| | 2010 |

| | | 6,500 |

| | December 2022 |

| CMA CGM |

| T/C |

| June 2022 |

| $34,350 |

| |||

|

| | | | | | | | | T/C | | December 2022 | | at market(7) | | +6 months at market(7) | ||||||

CMA CGM Racine |

| | 2010 |

| | | 6,500 |

| | January 2023 |

| CMA CGM |

| T/C |

| July 2022 |

| $34,350 |

| |||

|

| | | | | | | | | T/C | | January 2023 | | at market(7) | | +6 months at market(7) | ||||||

YM Mandate |

| | 2010 |

| | | 6,500 |

| | January 2028 |

| Yang Ming |

| B/B |

| January 2028 |

| $26,890 |

| +8 months at $26,890 |

||

YM Maturity |

| | 2010 |

| | | 6,500 |

| | April 2028 |

| Yang Ming |

| B/B |

| April 2028 |

| $26,890 |

| +8 months at $26,890 |

||

Dimitra C |

| | 2002 |

| | | 6,402 |

| | January 2020 |

| ONE |

| T/C |

| January 2020 |

| $18,000 |

| up to February 2020 at $18,000 |

||

Performance |

| | 2002 |

| | | 6,402 |

| | May 2020 |

| OOCL |

| T/C |

| May 2020 |

| $22,000 |

| up to July 2020 at $22,000 |

||

ZIM Rio Grande |

| | 2008 |

| | | 4,253 |

| | May 2020 |

| ZIM |

| T/C |

| May 2020 |

| $13,700 |

| +3 months at $13,700 |

||

ZIM Sao Paolo |

| | 2008 |

| | | 4,253 |

| | August 2020 |

| ZIM |

| T/C |

| August 2020 |

| $13,700 |

| +3 months at $13,700 |

||

ZIM Kingston |

| | 2008 |

| | | 4,253 |

| | September 2020 |

| ZIM |

| T/C |

| September 2020 |

| $13,700 |

| +3 months at $13,700 |

||

ZIM Monaco |

| | 2009 |

| | | 4,253 |

| | November 2020 |

| ZIM |

| T/C |

| November 2020 |

| $13,700 |

| +3 months at $13,700 |

||

ZIM Dalian |

| | 2009 |

| | | 4,253 |

| | February 2021 |

| ZIM |

| T/C |

| February 2021 |

| $13,700 |

| +3 months at $13,700 |

||

ZIM Luanda |

| | 2009 |

| | | 4,253 |

| | May 2021 |

| ZIM |

| T/C |

| May 2021 |

| $13,700 |

| +3 months at $13,700 |

||

YM Seattle |

| | 2007 |

| | | 4,253 |

| | November 2019 |

| Yang Ming |

| T/C |

| November 2019 |

| $9,000 |

| |||

YM Vancouver |

| | 2007 |

| | | 4,253 |

| | April 2020 |

| Yang Ming |

| T/C |

| April 2020 |

| $14,600 |

| +3 months at $14,600 |

||

Derby D |

| | 2004 |

| | | 4,253 |

| | May 2020 |

| CMA CGM |

| T/C |

| May 2020 |

| $9,200 |

| +2 months at $9,200 |

||

ANL Tongala |

| | 2004 |

| | | 4,253 |

| | May 2020 |

| CMA CGM |

| T/C |

| May 2020 |

| $9,200 |

| +2 months at $9,200 |

||

Dimitris C |

| | 2001 |

| | | 3,430 |

| | June 2020 |

| CMA CGM |

| T/C |

| June 2020 |

| $9,500 |

| +3 months at $9,500 |

||

|

| | | | | | | | | | | | +4.5 up to 6 months at $10,500 | |||||||||

Express Argentina |

| | 2010 |

| | | 3,400 |

| | May 2020 |

| Maersk |

| T/C |

| May 2020 |

| $9,000 |

| +4 months at $9,000 |

||

Express Brazil |

| | 2010 |

| | | 3,400 |

| | September 2020 |

| CMA CGM |

| T/C |

| September 2020 |

| $10,600 |

| +3 months at $10,600 |

||

Express France |

| | 2010 |

| | | 3,400 |

| | October 2020 |

| CMA CGM |

| T/C |

| November 2019 |

| $9,500 |

| +4 months at $9,000 |

||

|

| | | | | | | | | T/C | | October 2020 | | $10,600 | | +3 months at $10,600 | ||||||

Express Spain |

| | 2011 |

| | | 3,400 |

| | March 2020 |

| Cosco |

| T/C |

| March 2020 |

| $10,500 |

| +2 months at $10,500 |

||

Express Black Sea |

| | 2011 |

| | | 3,400 |

| | December 2019 |

| CMA CGM |

| T/C |

| December 2019 |

| $9,750 |

| up to February 2020 at $9,750 |

||

|

| | | | | | | | | | | | +10.5 up to 13.5 months at $11,000 | |||||||||

Singapore |

| | 2004 |

| | | 3,314 |

| | March 2020 |

| OOCL |

| T/C |

| March 2020 |

| $11,000 |

| +2 months at $11,000 |

||

S-3

Vessel Name

|

| Year Built |

| Vessel Size (TEU) |

| Expiration of Charter(1) |

| Charterer | | Charter Type(2) |

| Through | | Charter Rate(3) |

| Extension Options(4) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Colombo |

| | 2004 | | | | 3,314 | | | February 2020 |

| MSC |

| T/C |

| February 2020 |

| $8,250 |

| +2 months at $8,250 |

||

MSC Zebra |

| | 2001 |

| | | 2,602 |

| | September 2020 |

| MSC |

| T/C |

| September 2020 |

| $9,500 |

| |||

Danae C |

| | 2001 |

| | | 2,524 |

| | January 2020 |

| Hapag Lloyd |

| T/C |

| January 2020 |

| $9,000 |

| +13 months at $9,000 |

||

Amalia C |

| | 1998 |

| | | 2,452 |

| | March 2020 |

| Yang Ming |

| T/C |

| November 2019 |

| $8,750 |

| |||

|

| | | | | | | | | T/C | | March 2020 | | $10,100 | | +2 months at $10,100 | ||||||

Vladivostok |

| | 1997 |

| | | 2,200 |

| | November 2019 |

| Evergreen |

| T/C |

| November 2019 |

| $8,000 |

| up to February 2020 at $8,000 |

||

Stride |

| | 1997 |

| | | 2,200 |

| | April 2020 |

| Evergreen |

| T/C |

| April 2020 |

| $10,000 |

| +3 months at $10,000 |

||

Sprinter |

| | 1997 |

| | | 2,200 |

| | March 2020 |

| Evergreen |

| T/C |

| March 2020 |

| $9,100 |

| +3 months at $9,100 |

||

Future |

| | 1997 |

| | | 2,200 |

| | November 2019 |

| MCC |

| T/C |

| November 2019 |

| $7,650 |

| |||

Advance |

| | 1997 |

| | | 2,200 |

| | April 2020 |

| Evergreen |

| T/C |

| April 2020 |

| $10,000 |

| +3 months at $10,000 |

||

Bridge |

| | 1998 |

| | | 2,200 |

| | September 2020 |

| Samudera |

| T/C |

| November 2019 |

| $7,500 |

| |||

|

| | | | | | | | | T/C | | September 2020 | | $9,150 | | +2 months at $9,150 | ||||||

Highway |

| | 1998 |

| | | 2,200 |

| | February 2020 |

| Cosco |

| T/C |

| November 2019 |

| $8,475 |

| |||

|

| | | | | | | | | T/C | | February 2020 | | $10,000 | | +2 months at $10,000 | ||||||

Progress C |

| | 1998 |

| | | 2,200 |

| | March 2020 |

| Evergreen |

| T/C |

| March 2020 |

| $9,100 |

| +3 months at $9,100 |

||

Contracted Vessel

|

| Year Built |

| Vessel Size (TEU) |

| Expiration of Charter(1) |

| Charterer | | Charter Type(2) |

| Through | | Charter Rate(3) |

| Extension Options(4) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Conti Champion(9) |

| | 2005 | | | | 8,500 | | | — | | — | | — | | — | | — | | — | ||

Gemini Vessels

|

| Year Built |

| Vessel Size (TEU) |

| Expiration of Charter(1) |

| Charterer | | Charter Type(2) |

| Through | | Charter Rate(3) |

| Extension Options(4) | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Belita(10) |

| | 2006 | | | | 8,533 | | | September 2021 | | ZIM | | T/C | | November 2019 | | $25,000 | | |||

|

| | | | | | | | CMA CGM | | T/C | | September 2021 | | $25,000 | | +4 months at $25,000 | |||||

Catherine C(10) |

| | 2001 |

| | | 6,422 |

| | February 2023 |

| MSC |

| T/C |

| February 2020(6) |

| $10,000 |

| |||

|

| | | | | | | | | | February 2023(8) | | $18,000 | | +4 months at $18,000 | |||||||

Leo C(10) |

| | 2002 |

| | | 6,422 |

| | September 2022 |

| MSC |

| T/C |

| September 2022 |

| $18,000 |

| +4 months at $18,000 |

||

Suez Canal(10)(11) |

| | 2002 |

| | | 5,610 |

| | April 2020 |

| TS Lines |

| T/C |

| April 2020 |

| $16,250 |

| up to August 2020 at $16,250 |

||

Genoa(10)(11) |

| | 2002 |

| | | 5,544 |

| | August 2020 |

| Hapag Lloyd |

| T/C |

| August 2020 |

| $17,000 |

| +3 months at $17,000 |

||

S-4

Our Competitive Strengths

We believe that our key competitive strengths are:

Longstanding Relationships with Leading Liner Companies. We have longstanding relationships, some spanning multiple decades, and have chartered vessels to all of the top-15 global liner companies. Our largest current customers include CMA-CGM, Yang Ming, COSCO, Maersk, Evergreen and MSC. Our fixed-rate contracted charter revenues from these customers provide visible forward earnings, and we believe we will benefit from the strength of our customer relationships as we seek to recharter our vessels and continue to grow our fleet as attractive opportunities arise. Additionally we have historically worked collaboratively with our customers to adapt to changing requirements. For example, we are currently partnering with Maersk on enhancing vessel performance evaluation and assessment through big data analytics.

High Level of Charter Coverage. We retain a high degree of flexibility in employing our fleet in order to provide charters to our clients while also aiming to optimize earnings. All of the 60 containerships in our and Gemini's combined fleet are currently chartered on time or bareboat charters, which expire between 2019 and 2028. As of September 30, 2019, the average remaining duration of the charters for our fully owned fleet of 55 vessels was 4.3 years (weighted by aggregate contracted charter hire), which charters are expected to provide total contracted revenues of $1.4 billion during their initial terms. As of September 30, 2019, over 95% of this contracted revenue relates to the charters for our 24 largest ships, which generally have higher daily rates and longer durations than our smaller vessels, with the smaller vessels in our fleet generally available for employment in the near term to generate potential additional revenue. We believe this substantial level of contracted revenue will enable us to generate a base of stable cash flows and limit our exposure to downside charter market risk.

Experienced Management Team, Aligned with Public Shareholders. Our executive management team has an average of over 25 years of experience in the container shipping industry and is strongly aligned with our stockholders through equity ownership. Our Chief Executive Officer, Dr. John Coustas, has over 30 years of experience in the shipping industry and through an affiliated entity, Danaos Investment Limited, is our largest stockholder, beneficially owning approximately 31.5% of our common stock prior to this offering. Our management team has been involved in the containership industry since the 1980s, developing long-standing relationships with leading participants in all aspects of the containership industry. We believe this experience and industry relationships, when combined with our overall platform, facilitate our ability to source attractive charters and growth opportunities, including opportunities that may not be widely available.

Established Platform with Reputation for Operational Excellence and Technological Leadership. We are the world's third-largest publicly listed containership owner by TEU capacity with a fleet of 60 vessels ranging from 2,200 to 13,100 TEU in size. Our technical and commercial manager, Danaos Shipping, has been operating containerships since 1984 and has been recognized for implementing advanced technology and innovative processes to provide reliable and efficient services. Our manager's and our operational excellence and reliability resulted in a 98.8% fleet utilization rate for our fleet during the first nine months of 2019, excluding scheduled drydockings and special surveys. This compares with 98.5% average utilization over the last twelve months and 97.9% average over the last five years. Our manager was awarded the Lloyd's List Intelligence Big Data Award in 2015 for their "Waves" fleet performance system, which provides advanced performance, emissions and safety monitoring, bunkers control, energy and risk management and advanced superintendence for the vessels. We believe that our and our manager's reputations for excellence and technological leadership will continue to assist us in securing employment for our vessels.

S-5

Strong Operational Focus on Environmental Regulations. We are well-prepared for new environmental regulations, namely IMO 2020, and have emphasized a strategic focus on adopting measures ahead of mandated deadlines. We have already agreed to install exhaust cleaning systems (scrubbers) on nine of our vessels and have an operational plan in place for compliance with low-sulfur fuel regulations around IMO 2020, which goes into effect January 1, 2020.

Well Positioned for Accretive Growth. We believe our track record, scale, and industry relationships provide us with vessel-acquisition and chartering opportunities not widely available. We believe we are one of a select group of containership charter-owners regularly invited by leading liner companies to bid for long-term charter opportunities linked to containership newbuilding projects. Following our 2018 refinancing, we believe we have a strong balance sheet to support future growth. We have reduced our total principal amount of debt outstanding by $680.5 million since June 30, 2018, the period before our 2018 refinancing. We have no "balloon" principal payments due prior to December 31, 2023 and no preferred or other non-amortizing debt securities outstanding, and we expect to continue to reduce our outstanding debt in the next several years. We believe our moderate leverage positions us well to capture accretive growth opportunities.

Our Business Strategies

Our primary objective is to maximize value to our stockholders by pursuing the following strategies:

Actively Manage Charter Portfolio with Substantial Charter Coverage. We will continue to charter our containerships to leading liner companies in a manner that maintains a significant amount of contracted revenue, taking advantage of rates that are attractive in relation to contract duration while limiting downside risk. We will also seek to maintain a portfolio of charters that is increasingly diverse from a customer and maturity perspective. Our multi-year charter agreements for our vessels have been contracted in varying rate environments and expire at different times, which should reduce our exposure to rechartering risk in any particular charter market environment. We have recently chartered many of our smaller and older vessels on shorter term charters so as to be available to take advantage of any increase in charter rates as the market improves.

Continue Partnership Approach with Customers. We believe that our focus on customer service, operational excellence, and our leadership in technology enhance our relationships with our charterers, many of which, we believe, consider us to be one of their preferred providers. We maintain a strategic focus on direct and regular engagement with our customers to adapt our platform and operations to align with new customer needs and technological advancements. We believe this focus enhances our rechartering alternatives for our existing fleet, as well as opportunities for growth.

Maintain High-Quality Cost-Effective Operations. We focus on providing high-quality, cost-effective operations and work with our manager to reduce cost while maintaining a high level of service. We believe the average daily operating cost per vessel to us, which was $5,605 for the nine months ended September 30, 2019, is among the lowest in the containership industry and supports the profitability of our operations.

Maintain Strong Balance Sheet with Financial Flexibility. We have significantly reduced our leverage through our refinancing in 2018 to a modest level, and we expect that our scheduled debt amortization will result in further significant debt reduction over the next few years. We believe that our planned reductions in leverage, combined with no "balloon" principal payments due until December 2023, will enable us to further enhance our financial flexibility, generate additional free cash flow through reduced financing costs and allow us to allocate capital in a manner that maximizes value to stockholders.

S-6

Pursue Disciplined Growth. We believe the containership industry is positioned for further growth given constantly evolving global trade dynamics and increasing demand for seaborne containerized trade. Given our broad customer relationships and financial flexibility, we believe we are well positioned to take advantage of future growth in the industry. We intend to grow our fleet opportunistically with investments in both secondhand and, in conjunction with obtaining long term charter agreements from leading liner companies, newbuilding containerships. Given the recurring trend of demand for larger vessels, we expect to continue to focus on investment in larger containerships. These vessels provide our customers with economies of scale, aligning with their preference to replace smaller vessels with larger vessels over time, as well as other market developments such as the widening of the Panama Canal and the enhanced ability of many ports to accommodate larger capacity vessels. Our customers also often prefer chartering these larger vessels for longer periods of time, which can make them particularly attractive investments for us due to the longer term stable cash flows and reduced residual vessel value exposure such charters provide. We will evaluate growth opportunities in conjunction with the asset price, quality / technical specifications, and expected cash flow profile to seek to allocate capital in a manner which is accretive to shareholder value.

We can provide no assurance, however, that we will be able to implement our business strategies described above. For further discussion of the risks that we face, see "Risk Factors" beginning on page S-14 of this prospectus supplement.

Our Manager

Our executive officers provide strategic management for our company while also supervising, in conjunction with our board of directors, the management of our operations by our manager. We believe our manager has built a strong reputation in the shipping community by providing customized, high-quality operational services in an efficient manner for both new and older vessels. We have a management agreement pursuant to which our manager and its affiliates provide us and our subsidiaries with technical, administrative and certain commercial services at rates fixed through the current term of the management agreement, expiring December 31, 2024. Danaos Shipping is ultimately owned by Danaos Investment Limited, which is also our largest stockholder.

2018 Debt Refinancing

We consummated a comprehensive debt refinancing, which we refer to as the "2018 Refinancing", with our lenders on August 10, 2018. The 2018 Refinancing involved our entry into modified or amended and restated credit facilities (the "2018 Credit Facilities"), reflecting a $551 million reduction in our debt, reset financial and other covenants, modified interest rates and amortization profiles and extended final debt maturities by approximately five years to December 31, 2023 (or, in some cases, June 30, 2024). In the 2018 Refinancing, we issued to certain of our lenders an aggregate of 7,095,877 shares (99,342,271 shares before the 1-for-14 reverse stock split effected on May 2, 2019) of our common stock, representing 47.5% of our issued and outstanding common stock immediately after giving effect to such issuance. For additional information about our 2018 Refinancing, see "Item 5. Operating and Financial Review and Prospects—2018 Refinancing" in our Annual Report on Form 20-F for the year ended December 31, 2018 filed with the SEC on March 5, 2019 and incorporated by reference in this prospectus supplement.

Container Shipping Industry

For information regarding the containership industry, please see the section of this prospectus supplement titled "The International Container Shipping and Containership Leasing Industry" on page S-18.

S-7

Recent Developments

On August 26, 2019, Gemini acquired a 8,533 TEU container vessel built in 2006 for a gross purchase price of $25.3 million, and in October 2019, we entered into an agreement to acquire a 8,500 TEU containership built in 2005 for $25 million, with expected delivery to us by the end of May 2020, increasing our fleet capacity by 17,033 TEU, or by 5%.

Our Corporate Information

Danaos Corporation, formerly Danaos Holdings Limited, was formed on December 7, 1998 under the laws of Liberia. Danaos Holdings Limited was redomiciled in the Marshall Islands on October 7, 2005. In connection with the redomiciliation, the Company changed its name to Danaos Corporation. We operate through a number of wholly-owned subsidiaries which own the vessels in our fleet.

Our principal executive offices are c/o Danaos Shipping Co. Ltd., Athens Branch, 14 Akti Kondyli, 185 45 Piraeus, Greece. Our telephone number at that address is +30 210 419 6480. Our website is http://www.danaos.com. Information contained on, or that can be accessed through, our website does not constitute a part of this prospectus supplement and is not incorporated by reference herein. We have included our website address in this prospectus supplement solely as an inactive textual reference.

S-8

The following summary contains basic information about this offering and may not contain all of the information that may be important to you. You should read this entire prospectus supplement, the accompanying prospectus, any free writing prospectus we may provide to you in connection with this offering and the documents incorporated by reference herein and therein before making an investment decision.

Issuer |

Danaos Corporation, a Marshall Islands corporation. | |

Shares of common stock offered |

9,000,000 shares of common stock. |

|

Underwriters' option |

We have granted the underwriters the option, exercisable in whole or from time to time in part, to purchase up to 1,350,000 additional shares of our common stock directly from us, exercisable for 30 days after the date of this prospectus supplement. |

|

Shares of common stock to be outstanding immediately after this offering(1) |

24,371,470 shares of common stock, assuming the underwriters do not exercise their option to purchase additional shares. |

|

|

Certain of our significant stockholders, which are affiliates or family members of certain of our officers and directors, and executive officers have agreed to purchase approximately $27 million of common stock in the offering at the public offering price, including approximately $17 million by Danaos Investment Limited, which is our largest stockholder and beneficially owned by Dr. John Coustas, our Chief Executive Officer. |

|

Use of proceeds |

We estimate that the net proceeds from this offering, after deducting underwriting discounts and estimated expenses payable by us, will be approximately $51.4 million (or approximately $58.9 million if the underwriters exercise their option to purchase additional shares of our common stock in full). We plan to use the net proceeds of this offering for capital expenditures, including vessel acquisitions, and for other general corporate purposes. See "Use of Proceeds." |

|

Taxation |

You should carefully read the discussion of the principal United States federal, Marshall Islands and Liberian tax considerations associated with our operations and the acquisition, ownership and disposition of our common stock set forth in the section of our Annual Report on Form 20-F entitled "Item 10. Additional Information—Tax Considerations." |

|

NYSE listing |

Our common stock is listed on the New York Stock Exchange under the symbol "DAC." |

S-9

Risk factors |

Investing in our common stock involves a high degree of risk. See "Risk Factors" on page S-14 of this prospectus supplement, on page 4 of the accompanying prospectus and beginning on page 5 of our Annual Report on Form 20-F filed with the SEC on March 5, 2019 for a discussion of factors you should carefully consider before deciding to invest in shares of our common stock. |

S-10

Summary Historical Financial and Operating Data

The following table presents summary consolidated financial and other data of Danaos Corporation as of and for each of the years in the three year period ended December 31, 2018 and as of September 30, 2019 and each of the three and nine months ended September 30, 2019 and 2018. The summary consolidated financial data of Danaos Corporation is a summary of, is derived from and is qualified by reference to, our consolidated financial statements and notes thereto, which have been prepared in accordance with U.S. generally accepted accounting principles ("U.S. GAAP").

Our audited consolidated statements of operations, comprehensive income, stockholders' equity and cash flows for the years ended December 31, 2018, 2017 and 2016 and our consolidated balance sheets at December 31, 2018 and 2017, together with the notes thereto, are included in our Annual Report on Form 20-F filed with the SEC on March 5, 2019 incorporated herein by reference and should be read in their entirety. Our unaudited consolidated statements of operations, comprehensive income, stockholders' equity and cash flows for the three and nine months ended September 30, 2019 and 2018, and our consolidated balance sheet as of September 30, 2019, together with the notes thereto, are included in our Report on Form 6-K filed with the SEC on November 6, 2019 incorporated by reference herein and should be read in their entirety. The unaudited interim financial statements reflect all adjustment which are, in the opinion of management, necessary to a fair statement of the results for the interim periods presented. The results of operations for the three and nine months ended September 30, 2019 may not be indicative of the results that may be expected for the entire year ending December 31, 2019.

| |

Three Months Ended September 30, |

Nine Months Ended September 30, |

Year Ended December 31, | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2019 | 2018 | 2019 | 2018 | 2018 | 2017 | 2016 | |||||||||||||||

| |

In thousands, except per share amounts |

|||||||||||||||||||||

STATEMENTS OF OPERATIONS |

||||||||||||||||||||||

Operating revenues |

$ | 111,830 | $ | 117,781 | $ | 337,040 | $ | 343,101 | $ | 458,732 | $ | 451,731 | $ | 498,332 | ||||||||

Voyage expenses |

(2,792 | ) | (2,883 | ) | (8,794 | ) | (9,230 | ) | (12,207 | ) | (12,587 | ) | (13,925 | ) | ||||||||

Vessel operating expenses |

(24,858 | ) | (25,461 | ) | (78,035 | ) | (79,052 | ) | (104,604 | ) | (106,999 | ) | (109,384 | ) | ||||||||

Depreciation |

(24,336 | ) | (26,995 | ) | (72,141 | ) | (80,752 | ) | (107,757 | ) | (115,228 | ) | (129,045 | ) | ||||||||

Amortization of deferred drydocking and special survey costs |

(2,271 | ) | (2,636 | ) | (6,525 | ) | (6,888 | ) | (9,237 | ) | (6,748 | ) | (5,528 | ) | ||||||||

Impairment loss |

— | — | — | — | (210,715 | ) | — | (415,118 | ) | |||||||||||||

Bad debt expense |

— | — | — | — | — | — | (15,834 | ) | ||||||||||||||

General and administrative expenses |

(6,422 | ) | (7,431 | ) | (19,783 | ) | (18,390 | ) | (26,334 | ) | (22,672 | ) | (22,105 | ) | ||||||||

Gain/(loss) on sale of vessels |

— | — | — | — | — | — | (36 | ) | ||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Income/(loss) from operations |

51,151 | 52,375 | 151,762 | 148,789 | (12,122 | ) | 187,497 | (212,643 | ) | |||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Interest income |

1,586 | 1,505 | 4,751 | 4,298 | 5,781 | 5,576 | 4,682 | |||||||||||||||

Interest expense |

(18,216 | ) | (20,509 | ) | (54,903 | ) | (66,378 | ) | (85,706 | ) | (86,556 | ) | (82,966 | ) | ||||||||

Other finance expenses |

(308 | ) | (679 | ) | (2,402 | ) | (2,611 | ) | (3,026 | ) | (4,126 | ) | (4,932 | ) | ||||||||

Equity income/(loss) on investments |

560 | 728 | 508 | 912 | 1,365 | 965 | (16,252 | ) | ||||||||||||||

Gain on debt extinguishment |

— | 116,365 | — | 116,365 | 116,365 | — | — | |||||||||||||||

Other income/(expenses), net |

(5 | ) | (21,637 | ) | 429 | (50,565 | ) | (50,456 | ) | (15,757 | ) | (41,602 | ) | |||||||||

Unrealized and realized losses on derivatives |

(913 | ) | (931 | ) | (2,709 | ) | (2,763 | ) | (5,137 | ) | (3,694 | ) | (12,482 | ) | ||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Total other income/(expenses), net |

(17,296 | ) | 74,842 | (54,326 | ) | (742 | ) | (20,814 | ) | (103,592 | ) | (153,552 | ) | |||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Net income/(loss) |

$ | 33,855 | $ | 127,217 | $ | 97,436 | $ | 148,047 | $ | (32,936 | ) | $ | 83,905 | $ | (366,195 | ) | ||||||

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

PER SHARE DATA(1) |

||||||||||||||||||||||

Basic earnings/(loss) per share of common stock |

$ | 2.27 | $ | 10.80 | $ | 6.52 | $ | 16.15 | $ | (3.10 | ) | $ | 10.70 | $ | (46.69 | ) | ||||||

Diluted earnings/(loss) per share of common stock |

$ | 2.20 | $ | 10.76 | $ | 6.36 | $ | 16.12 | $ | (3.10 | ) | $ | 10.70 | $ | (46.69 | ) | ||||||

Basic weighted average number of shares (in thousands) |

14,939 | 11,766 | 14,939 | 9,168 | 10,623 | 7,845 | 7,843 | |||||||||||||||

Diluted weighted average number of shares (in thousands) |

15,373 | 11,828 | 15,309 | 9,186 | 10,623 | 7,845 | 7,843 | |||||||||||||||

S-11

| |

Three Months Ended September 30, |

Nine Months Ended September 30, |

Year Ended December 31, | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2019 | 2018 | 2019 | 2018 | 2018 | 2017 | 2016 | |||||||||||||||

| |

In thousands, except other data |

|||||||||||||||||||||

CASH FLOW DATA |

||||||||||||||||||||||

Net cash provided by operating activities |

$ | 56,189 | $ | 55,308 | $ | 167,645 | $ | 110,900 | $ | 164,686 | $ | 181,073 | $ | 261,967 | ||||||||

Net cash provided by/(used in) investing activities |

(4,124 | ) | (400 | ) | (14,762 | ) | (2,083 | ) | (8,250 | ) | 1,758 | (9,379 | ) | |||||||||

Net cash used in financing activities |

(48,045 | ) | (50,010 | ) | (147,335 | ) | (98,391 | ) | (148,868 | ) | (189,653 | ) | (251,130 | ) | ||||||||

BALANCE SHEET DATA (at period end) |

||||||||||||||||||||||

Total current assets |

$ | 127,588 | $ | 119,680 | $ | 127,588 | $ | 119,680 | $ | 119,750 | $ | 125,999 | $ | 135,954 | ||||||||

Total assets |

2,637,684 | 2,921,347 | 2,637,684 | 2,921,347 | 2,679,842 | 2,986,396 | 3,127,064 | |||||||||||||||

Total current liabilities, including current portion of long-term debt |

222,203 | 239,424 | 222,203 | 239,424 | 222,701 | 2,379,839 | 2,566,281 | |||||||||||||||

Current portion of long-term debt, net |

115,551 | 118,517 | 115,551 | 118,517 | 113,777 | 2,329,601 | 2,504,932 | |||||||||||||||

Long-term debt, net |

1,298,371 | 1,527,390 | 1,298,371 | 1,527,390 | 1,508,108 | — | — | |||||||||||||||

Total stockholders' equity |

$ | 791,756 | $ | 881,845 | $ | 791,756 | $ | 881,845 | $ | 690,853 | $ | 548,705 | $ | 487,713 | ||||||||

EBITDA/ADJUSTED EBITDA |

||||||||||||||||||||||

EBITDA(2) |

$ | 78,133 | $ | 177,187 | $ | 229,387 | $ | 302,418 | $ | 169,736 | $ | 293,724 | $ | (145,863 | ) | |||||||

Adjusted EBITDA(2) |

79,328 | 82,745 | 232,447 | 237,677 | 317,848 | 310,378 | 350,587 | |||||||||||||||

OTHER DATA |

||||||||||||||||||||||

Number of vessels at period end |

55 | 55 | 55 | 55 | 55 | 55 | 55 | |||||||||||||||

TEU capacity at period end |

327,616 | 327,616 | 327,616 | 327,616 | 327,616 | 327,616 | 329,588 | |||||||||||||||

Ownership days |

5,060 | 5,060 | 15,015 | 15,015 | 20,075 | 20,075 | 20,138 | |||||||||||||||

Operating days |

4,995 | 4,927 | 14,828 | 14,471 | 19,424 | 19,345 | 19,057 | |||||||||||||||

Average Gross Daily Charter Rate |

$ | 22,388 | $ | 23,905 | $ | 22,730 | $ | 23,710 | $ | 23,617 | $ | 23,351 | $ | 26,150 | ||||||||

Utilization(3) |

98.7 | % | 97.4 | % | 98.8 | % | 96.4 | % | 96.8 | % | 96.4 | % | 94.6 | % | ||||||||

EBITDA and Adjusted EBITDA have limitations as analytical tools, and should not be considered in isolation or as a substitute for analysis of our results as reported under U.S. GAAP. Some of these limitations are: (i) EBITDA/Adjusted EBITDA does not reflect changes in, or cash requirements for, working capital needs; and (ii) although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future, and EBITDA/Adjusted EBITDA do not reflect any cash requirements for such capital expenditures. In evaluating Adjusted EBITDA, you should be aware that, in the future, we may incur expenses that are the same as or similar to some of the adjustments in this presentation. Our presentation of Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Because of these limitations, EBITDA/Adjusted EBITDA should not be considered as principal indicators of our performance.

S-12

Net income/(loss) Reconciliation to EBITDA and Adjusted EBITDA

| |

Three Months Ended September 30, |

Nine Months Ended September 30, |

Year Ended December 31, | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2019 | 2018 | 2019 | 2018 | 2018 | 2017 | 2016 | |||||||||||||||

| |

(In thousands) |

|||||||||||||||||||||

Net income/(loss) |

$ | 33,855 | $ | 127,217 | $ | 97,436 | $ | 148,047 | $ | (32,936 | ) | $ | 83,905 | $ | (366,195 | ) | ||||||

Depreciation |

24,336 | 26,995 | 72,141 | 80,752 | 107,757 | 115,228 | 129,045 | |||||||||||||||

Amortization of deferred drydocking & special survey costs |

2,271 | 2,636 | 6,525 | 6,888 | 9,237 | 6,748 | 5,528 | |||||||||||||||

Amortization of deferred realized losses of cash flow interest rate swaps |

913 | 931 | 2,709 | 2,763 | 3,694 | 3,694 | 4,028 | |||||||||||||||

Amortization of finance costs and debt discount |

3,898 | 4,430 | 12,846 | 9,544 | 14,957 | 11,153 | 12,652 | |||||||||||||||

Finance costs accrued (Exit Fees under our Bank Agreements) |

129 | 404 | 424 | 1,888 | 2,059 | 3,169 | 3,447 | |||||||||||||||

Interest income |

(1,586 | ) | (1,505 | ) | (4,751 | ) | (4,298 | ) | (5,781 | ) | (5,576 | ) | (4,682 | ) | ||||||||

Interest expense |

14,317 | 16,079 | 42,057 | 56,834 | 70,749 | 75,403 | 70,314 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

EBITDA |

78,133 | 177,187 | 229,387 | 302,418 | 169,736 | 293,724 | (145,863 | ) | ||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Gain on debt extinguishment |

— | (116,365 | ) | — | (116,365 | ) | (116,365 | ) | — | — | ||||||||||||

Refinancing professional fees |

— | 21,766 | — | 51,467 | 51,313 | 14,297 | — | |||||||||||||||

Loss on sale of securities |

— | — | — | — | — | 2,357 | 12,906 | |||||||||||||||

Impairment loss |

— | — | — | — | 210,715 | — | 415,118 | |||||||||||||||

Impairment loss on securities |

— | — | — | — | — | — | 29,384 | |||||||||||||||

Impairment loss component of equity loss on investments |

— | — | — | — | — | — | 14,642 | |||||||||||||||

Bad debt expense |

— | — | — | — | — | — | 15,834 | |||||||||||||||

Accelerated amortization of accumulated other comprehensive loss |

— | — | — | — | 1,443 | — | 7,706 | |||||||||||||||

Stock based compensation |

1,195 | 157 | 3,060 | 157 | 1,006 | — | 76 | |||||||||||||||

Loss on sale of vessels |

— | — | — | — | — | — | 36 | |||||||||||||||

Realized loss on derivatives |

— | — | — | — | — | — | 5,397 | |||||||||||||||

Unrealized gain on derivatives |

— | — | — | — | — | — | (4,649 | ) | ||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Adjusted EBITDA |

$ | 79,328 | $ | 82,745 | $ | 232,447 | $ | 237,677 | $ | 317,848 | $ | 310,378 | $ | 350,587 | ||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

S-13

Investing in our common stock involves certain risks. You are urged to read and consider the risk factors described in our reports filed with the SEC under the Exchange Act, which are incorporated by reference into this prospectus supplement and the accompanying prospectus, including our Annual Report on Form 20-F for the year ended December 31, 2018 filed with the SEC on March 5, 2019. Before making an investment decision, you should carefully consider these risks as well as other information we include or incorporate by reference in this prospectus supplement and the accompanying prospectus. You should also be aware that new risks may emerge in the future at any time, and we cannot predict such risks or estimate the extent to which they may affect our financial condition or performance.

S-14

We estimate that the net proceeds from this offering, after deducting the underwriting discount and estimated expenses relating to this offering payable by us, will be approximately $51.4 million (or approximately $58.9 million if the underwriters exercise their option to purchase additional shares of our common stock in full). We plan to use the net proceeds of this offering for capital expenditures, including vessel acquisitions, and for other general corporate purposes.

S-15

The table below sets forth our consolidated cash and cash equivalents and capitalization as of September 30, 2019:

Other than these adjustments, there has been no material change in our capitalization from debt or equity issuances, re-capitalization or special dividends between September 30, 2019 and November 18, 2019.

The following data are qualified in their entirety by our financial statements and related notes and other information incorporated by reference in this prospectus supplement and the accompanying prospectus. This table should be read in conjunction with our consolidated financial statements for the nine months ended September 30, 2019 and "Operating and Financial Review and Prospects" included in our Report on Form 6-K filed with the SEC on November 6, 2019, incorporated by reference herein.

| |

As of September 30, 2019 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

Actual | As adjusted | As further adjusted |

|||||||

| |

(In thousands) |

|||||||||

Cash |

||||||||||

Cash and cash equivalents |

$ | 82,823 | $ | 52,946 | $ | 104,353 | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Capitalization |

||||||||||

Debt: |

||||||||||

Total debt(1)(2) |

$ | 1,612,786 | $ | 1,582,909 | $ | 1,582,909 | ||||

| | | | | | | | | | | |

Stockholders' equity: |

||||||||||

Preferred stock, par value $0.01 per share; 100,000,000 preferred shares authorized and none issued; actual, as adjusted and as further adjusted |

— | — | — | |||||||

Common stock, par value $0.01 per share; 750,000,000 shares authorized; 15,371,470 shares issued and outstanding actual and as adjusted and 24,371,470 shares issued and outstanding as further adjusted(3) |

154 | 154 | 244 | |||||||

Additional paid-in capital |

730,620 | 730,620 | 781,937 | |||||||

Accumulated other comprehensive loss |

(118,303 | ) | (118,303 | ) | (118,303 | ) | ||||

Retained earnings |

179,285 | 179,285 | 179,285 | |||||||

| | | | | | | | | | | |

Total stockholders' equity |

791,756 | 791,756 | 843,163 | |||||||

| | | | | | | | | | | |

Total capitalization |

$ | 2,404,542 | $ | 2,374,665 | $ | 2,426,072 | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

S-16

in our Annual Report on Form 20-F filed with the SEC on March 5, 2019 and incorporated herein by reference.

We expect to be permitted, under the terms of our credit facilities, to pay dividends after the completion of this offering. We have not yet adopted a dividend policy with respect to future dividends.

We have not paid a dividend since 2008, when our board of directors determined to suspend the payment of cash dividends as a result of market conditions in the international shipping industry. We are not permitted to pay dividends under our credit facilities until (1) we receive in excess of $50 million in net cash proceeds from offerings of common stock which are consummated after the 2018 Refinancing, and (2) the payment in full of the first installment of amortization payable following the consummation of the 2018 Refinancing under each new credit facility, which installment payments have been made and, accordingly, this condition has been satisfied. After these conditions are satisfied under our loan agreements, we will be permitted to pay dividends if, among other things, a default has not occurred and is continuing or would occur as a result of the payment of such dividend and we remain in compliance with the financial and other covenants thereunder. To the extent our credit facilities permit us to pay dividends, any dividend payments will be subject to us having sufficient available excess cash and distributable reserves, and declaration and payment of any dividends will be at the discretion of our board of directors.

The timing and amount of dividend payments will be dependent upon our earnings, financial condition, cash requirements and availability, fleet renewal and expansion, restrictions in our credit facilities, the provisions of Marshall Islands law affecting the payment of distributions to stockholders and other factors. Declaration and payment of any future dividend is subject to the discretion of our board of directors. We are a holding company, and we depend on the ability of our subsidiaries to distribute funds to us in order to satisfy our financial obligations and to make any dividend payments.

S-17

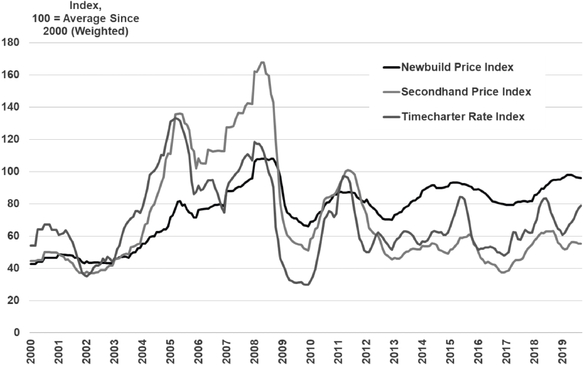

THE INTERNATIONAL CONTAINER SHIPPING AND CONTAINERSHIP LEASING INDUSTRY

Maritime Strategies International Ltd. ("MSI") has provided certain statistical and graphical information contained in this prospectus under the caption "The International Container Shipping and Containership Leasing Industry." MSI has advised that (i) some information in MSI's database is derived from estimates derived from industry sources or subjective judgments, (ii) the information in the databases of other maritime data collection agencies may differ from the information in MSI's database, (iii) whilst MSI has taken reasonable care in the compilation of the statistical and graphical information and believes it to be accurate and correct, data compilation is subject to limited audit and validation procedures and may accordingly contain errors, (iv) MSI, its agents, officers and employees cannot accept liability for any loss suffered in consequence of reliance on such information or in any other manner, and (v) the provision of such information does not obviate any need to make appropriate further enquiries.

Industry Overview

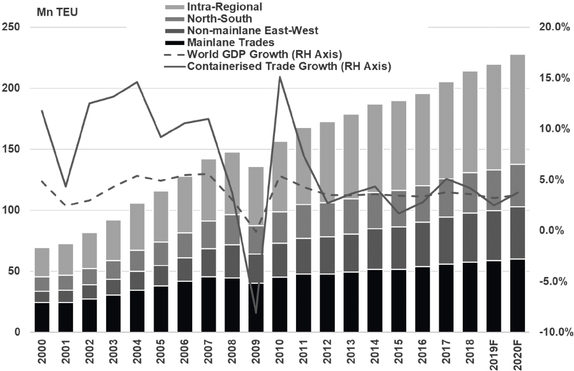

The container shipping industry is one of the younger shipping sectors, with the first containerized cargoes shipped in the mid-1950s. Containerization is the most convenient and cost-effective way to transport a wide range of cargoes, predominantly a diverse selection of consumer, manufactured, and semi-manufactured goods. Global containerized trade volumes for 2018 are estimated to be 208 million TEU.

The containerized supply chain extends throughout the world. The Mainlane trades are those linking the major manufacturing economies in Asia with the major consumer economies in North America and Europe and the trans-Atlantic trade. However, over 70% of global containerized trade volumes are in the non-Mainlane trades, with intra-regional trades alone representing almost 39%. Indeed, the largest trade grouping comprises the intra-Asian trades connecting that region's rapidly growing markets.

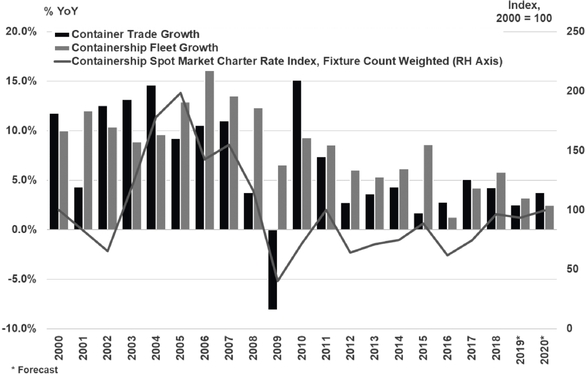

Since the 1980s, growth in container trade be grouped into three different phases, each with its own characteristics. The first phase was a period of rapid expansion. From 1993 to 2008, containerized trade grew at a compound annual rate of over 9.0%. This was driven both by the ongoing 'containerization' of cargoes previously transported by other types of vessel, as well structural changes in the world economy, including China's infrastructural investment growth and integration into the global trade system, the off-shoring of production, and the expansion of global supply chains.

The second phase encompassed the 2008-09 global financial crisis and its aftermath. 2009, due to the global financial crisis and recession, was the only year of negative growth in the industry's history, with volumes shrinking 8.0%. Volumes subsequently rebounded in 2010 and 2011, with growth of 15.0% and 7.0% respectively.

The third phase has been characterized by growth in container trade of closer to, but still faster than, growth in global GDP. Between 2011 and 2018 average compound annual growth of containerized trade was 3.5%. More recently, over the first nine months of 2019 estimated growth in primary container trade was just over 3.0%. Full year growth in 2019 is expected to be 2.5%, while growth is forecast to accelerate in 2020 to 3.7%.

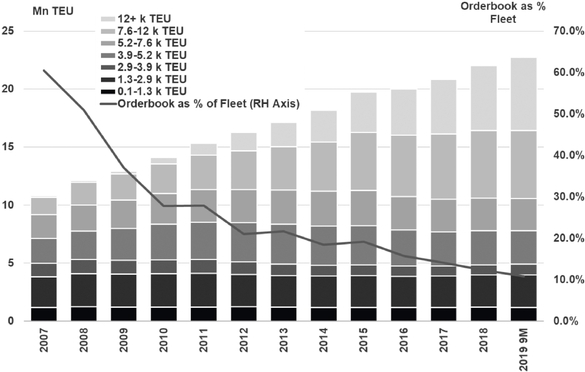

The rapid expansion in containerized trade has also led to a rapid expansion in the global liner fleet, of which the vast majority of vessels are fully cellular containerships: vessels specialized for the transport of containers and fitted with cell guides throughout the ship to optimize container stowage and significantly enhance the efficiency of load and discharge operations. Between 1995 and 2008, the nominal carrying capacity of the industry-wide fully cellular fleet grew by a compound annual rate of 11.4%; and from 2009 through 2018 at 6.1%. As at September 30, 2019, industry-wide fleet capacity stood at 22.7 million TEU, aboard a total of 5,212 vessels.

S-18

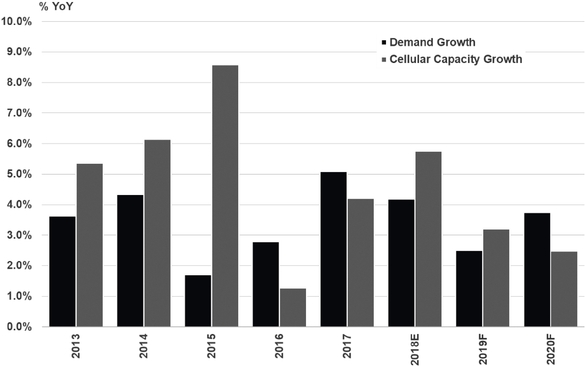

Demand Growth v. Supply Growth, Including 2019 and 2020 Forecasts

Containerships have been upsized over time to carry increasing cargo volumes and reduce unit costs. Whereas in 1995 the largest vessel in the industry-wide fleet had a nominal capacity of 5,344 TEU, as at September 30, 2019, the largest vessel had a nominal capacity of 23,756 TEU. Over the same period, average containership nominal capacity across the industry increased from 1,020 TEU to 4,360 TEU.

Within the container shipping industry, key participants include shippers, liner companies and charter-owners. Shippers are the senders and receivers of containerized cargo (Walmart is a typical example). Liner companies (also referred to as lines or operators) are logistics service providers responsible for the seaborne, and often also inland, transportation of containerized goods; they negotiate freight rates with shippers themselves, or with third parties such as freight forwarders/consolidators. Liner companies either operate vessels that they themselves own, or lease vessels from charter-owners. Charter-owners (also referred to as containership owners and containership lessors) provide the function of owning containerships and leasing, or chartering, them out to liner companies

In the containership charter market, leases are most often structured as time charters. Under a time charter, with the exception of fuel (which is paid for by the lessee), the operating costs of the vessel are borne by the lessor. Charter periods can vary in length: the spot market generally refers to charter fixtures of 12 months or less, while term charters cover longer fixtures, with periods of five years or more not uncommon. The containership lessor assumes no freight risk under a time charter.

Demand

Global container trade predominantly involves the movement of manufactured and semi-manufactured goods. Growth drivers include the increasing consumption of manufactured goods, the containerization of goods formerly transported by other vessel types (above all refrigerated cargoes), and the offshoring of manufacturing and extension of global supply chains. Consequently, historically containerized trade has tended to expand at a multiple of both global Gross Domestic Product ("GDP") growth and total seaborne trade growth.

S-19

The container trade growth-multiplier effect was disrupted in 2015 and 2016, when both seaborne and container trade grew slower than world GDP. In 2015 container trade grew by 1.7%, compared against world GDP growth of 3.4%, and in 2016 container trade grew by around 2.8% and world GDP by around 3.4%. In 2017 the container trade growth multiplier strengthened notably and remained in positive territory in 2018. World GDP growth and container trade growth have faced headwinds in 2019, with container trade forecast to grow by 2.5% and world GDP growth by 3.2%. However, container trade growth is forecast to accelerate in 2020 to 3.7%.

Growth of Containerized Trade, Including 2019 and 2020 Forecasts

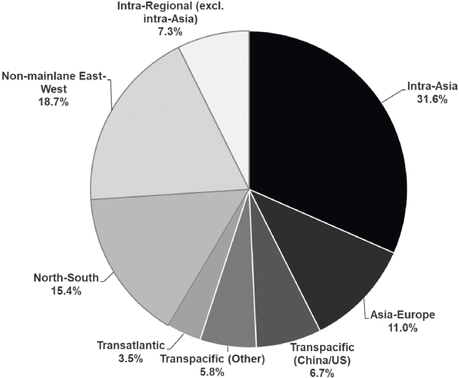

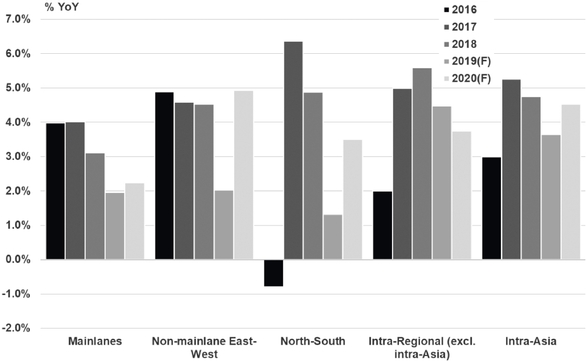

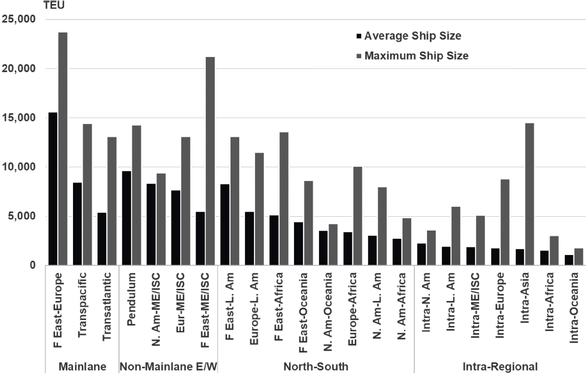

Traditionally, global container trade has been separated into four different trade groupings: the arterial East-West Trades ("mainlanes"), the non-mainlane East-West trades, North-South trades and intra-regional trades.

The mainlane trades are the major East-West routes connecting Asia, North America and Europe: the Asia-Europe, Transpacific and Transatlantic trades. Of these, the Transpacific (commonly taken to refer to all cargoes moved between Asia and North America, regardless of whether they cross the Pacific or go via the Suez Canal) and Asia-Europe are the largest.

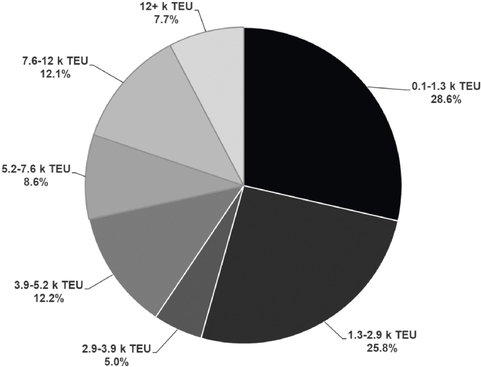

Due to the length and high cargo volumes of these trades, in combination with well-developed port infrastructure, cargoes on the Transpacific and, above all, Asia-Europe trades are normally carried on the largest vessels in the fleet. Higher cargo volumes and longer sailing distances allow vessels to maximize their economies of scale. Asia-Europe services across the industry deploy the fleet's largest vessels, trending towards 18,000 TEU or larger, with an average ship size of 15,604 TEU. Vessels deployed on the Transpacific are somewhat smaller, with a maximum ship size as of September 30, 2019, of 14,424 TEU and an average size of 8,402 TEU.

The non-mainlane East-West trades are those which link the Middle East and Indian Subcontinent to Asia, Europe and North America. Of these, the most significant is the Westbound Asia-Middle East/Indian Subcontinent trade, which in 2018 represented nearly 5.5% of global volumes. While historically these trades have been served by smaller vessels than those deployed on the mainlane trades, the

S-20

combination of relatively high cargo volumes and port infrastructure development has resulted in the deployment of vessels of 10,000 TEU or larger on some service loops (with vessels on one current service reaching 21,000 TEU). The average vessel size on non-mainlane East-West trades is 6,215 TEU.