dated September 28, 2018 (the “Prospectus/Proxy Statement”) and the supplement thereto dated October 23, 2018 (the “Supplement”), as filed under the Registration Statement, contains additional information about the Merger and the Arrangement.

The New Alithya Subordinate Voting Shares have been approved for listing, on the Nasdaq Capital Market and the Toronto Stock Exchange under the symbol “ALYA”. The trading of the New Alithya Subordinate Voting Shares commenced on the Nasdaq Capital Market and the Toronto Stock Exchange on November 2, 2018.

In connection with the completion of the Arrangement, New Alithya received binding agreements from certain former Edgewater stockholders and Alithya shareholders not to sell their New Alithya Subordinate Voting Shares or New Alithya Multiple Voting Shares for a minimum period of 12 months following the Effective Date, without receiving New Alithya’s prior written consent. Those former Edgewater stockholders and Alithya shareholders included Ancora Advisors, LLC (which prior to the Effective Date owned approximately 10.2% of the total outstanding Edgewater Common Stock), the directors and officers of Alithya and Edgewater remaining with the post-closing operations of New Alithya, Alithya shareholders receiving more than 5% of all of the issued and outstanding New Alithya Shares taken as a whole, at closing, and certain other employees or other persons mutually agreed upon between Alithya and Edgewater.

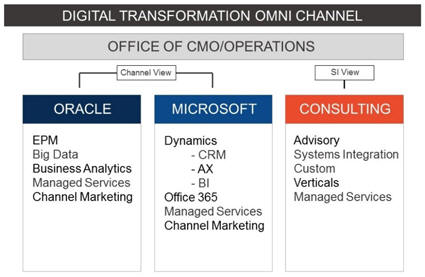

Our Services

Edgewater offers a full spectrum of services and expertise to ensure the success of our engagements. Our consulting services are categorized into two different components: (1) Channel View and (2) Systems Integration View.

The following diagram illustrates these offerings:

Edgewater has the proven expertise to plan, deliver and manage integration services that improve performance and maximize business results. We focus on deploying new systems and unlocking the value of the existing corporate assets. This proven expertise enables us to bring complex technologies and systems together while minimizing risk, leveraging our clients’ technology investments and delivering tailored solutions.

Factors Influencing Our Results of Operations

Revenue. The Company derives its service revenue from time and materials-based contracts, fixed-price contracts and retainer-based arrangements. Time and materials-based contracts represented 88.3% and 86.9% of service revenue for the three- and nine-month periods ended September 30, 2018, respectively. Time and materials-based contracts represented 82.9% and 83.9% of service revenue for the three- and nine-month periods ended September 30, 2017. Revenue under time and materials contracts is recognized as services are rendered and performed at contractually agreed upon rates. Fixed-price contracts represented 7.3% and 8.0% of service revenue for the three- and nine-month periods ended September 30, 2018. Fixed-price contracts represented 11.5% and 9.6% of service revenue for the three- and nine-month periods ended September 30, 2017. Revenue pursuant to fixed-price contracts is recognized over time based on the proportional performance (using a hours-based input method) related to individual performance

17